The S&P 500 dropped into a bear market more than a year ago, and the broad-based index is still down 14% from all-time highs. History says the drawdown is temporary. Every bear market ushers in a new bull market, and the S&P 500 has never failed to recoup its losses.

That’s why investors should treat the current situation as a buying opportunity for great stocks, especially the handful of artificial intelligence (AI) growth stocks currently trading at attractive prices.

Here’s why The Trade Desk (TTD) and Arista Networks (ANET) are two AI stocks worth buying today and holding long-term.

1. The Trade Desk

1. The Trade Desk

The Trade Desk runs the largest independent demand-side platform (DSP). Its software leans on AI to help advertisers plan, measure, and optimize data-driven campaigns across digital channels like desktop, mobile, and connected TV (CTV). The Trade Desk competes with much larger tech giants like Alphabet and Meta Platforms, but the company is gaining market share due to its more transparent business model and arguably superior technology.

Alphabet and Meta Platforms provide adtech solutions to ad buyers and ad sellers, which is tantamount to working for two rival companies. But the conflict of interest runs even deeper. Alphabet and Meta Platforms also sell their own ad inventory (e.g., Google Search, Instagram) alongside inventory from third-party publishers. That means they also compete against their customers. But The Trade Desk works only with ad buyers and it does not own ad inventory.

That ad agnosticism allows The Trade Desk to build the most advanced data marketplace in the industry, according to management. Its platform sources shopper data from 80% of the largest retailers in the U.S., but those brands are usually unwilling to share data with rivals like Alphabet and Meta. Additionally, The Trade Desk was recently recognized as an adtech leader by consultancy Quadrant Knowledge Solutions. The report cited The Trade Desk’s advanced AI and data management platform as key differentiators. Those advantages ultimately allow brands to target campaigns and measure performance more effectively.

The Trade Desk reported solid financial results in the fourth quarter. Revenue rose 24% to $491 million and cash from operations jumped 6% to $173 million. For context, Alphabet and Meta both reported a 4% decline in ad revenue in the fourth quarter, meaning they ceded market share to The Trade Desk.

The Trade Desk has a long runway for growth. Grand View Research estimates the adtech market will increase at 14% annually to reach $2.4 trillion by 2030. Shares currently trade at 19.9 times sales, a discount to the five-year average of 24.8 times sales. That valuation is not cheap, but investors can still buy a small position in this AI growth stock now, then dollar-cost average their way into a bigger position over time.

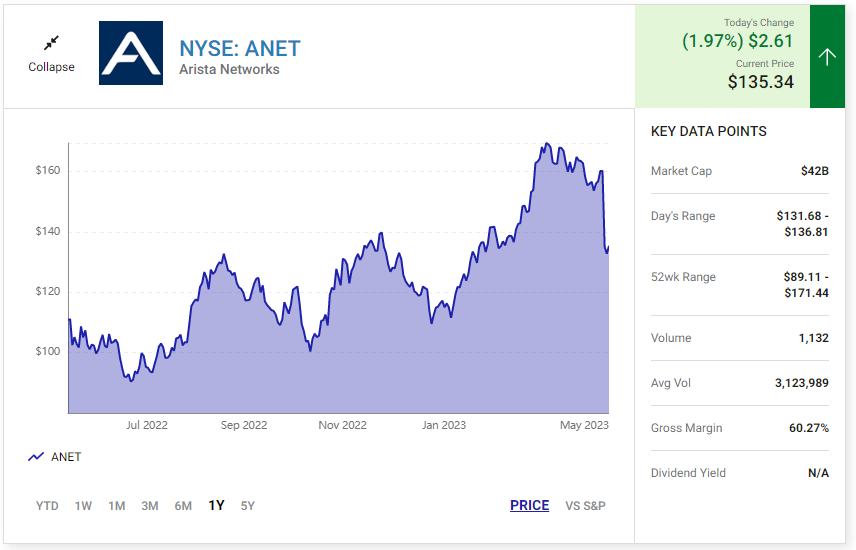

2. Arista Networks

2. Arista Networks

Arista provides networking solutions for cloud and enterprise data centers. Its portfolio includes switches and routers that offer industry-leading speed, capacity, and power efficiency; it also includes adjacent software for network automation, monitoring, and security.

But its greatest innovation is the Extensible Operating System (EOS), the software that runs across every Arista hardware product. Legacy vendors generally rely on multiple operating systems, but Arista simplifies network management by implementing just one. In short, EOS lowers the total cost of network ownership for clients by reducing complexity.

Arista delivered solid financial results in the first quarter. Revenue jumped 54% to $1.4 billion and earnings under generally accepted accounting principles (GAAP) soared 62% to $1.38 per diluted share. Management expects growth to decelerate significantly in the coming quarters as large cloud customers pull back on spending, but that has to do with the challenging economic environment and the cyclicality of the data center switching industry. Investors have good reason to believe growth will reaccelerate in the future.

Specifically, Arista should benefit from several tailwinds in the coming years, including cloud migration and the proliferation of connected devices, both of which will create a need for more performant data center networks. But the company should also benefit from the growing demand for AI software.

AI is a compute-intensive technology that demands high-speed networking solutions, and Arista is the market leader. The company captured 42% market share in high-speed data center switches (i.e., 100G, 200G, and 400G) last year, up from 36% in the prior year. For context, the runner-up, Cisco Systems, captured 21% market share last year, down from 23% in the prior year. In other words, Arista is not only the market leader, but it’s also taking share.

With that in mind, management believes its market opportunity will expand at 13% annually from $31 billion in 2023 to $51 billion by 2027, and the company should have no trouble growing faster than the industry average given its strong competitive position. Currently, shares trade at 9.7 times sales, roughly even with the five-year average of 9.9 times sales. That creates a reasonable buying opportunity for investors, though it would be prudent to start with a small position. Any future share price declines would likely present opportunities to buy more.

— Trevor Jennewine

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: The Motley Fool