Warren Buffett started his career off by chasing “cigar butts”.

These were junk stocks that were so cheap, they were akin to finding discarded cigar butts when one free puff left in them.

Over time, though, he learned from his ways and reformed.

Later, he began to invest in great businesses.

That transition is exemplified by this Buffett quote: “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

But what if you could buy a wonderful company at a wonderful price?

That would be the best of both worlds.

First, how do we find wonderful companies to invest in?

Well, I’d argue the Dividend Champions, Contenders, and Challengers list is a great place to begin that search.

This list contains invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

These are all dividend growth stocks.

These are all dividend growth stocks.

The logic behind these stocks is simple: A growing dividend requires growing profit to support it, and only a great company can routinely grow its profit.

I’ve taken that logic to heart over the years, using it to build my FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure dividend income for me to live off of.

Indeed, I’ve been living off of dividends for a number of years now.

In fact, I quit my job and retired in my early 30s.

How?

My Early Retirement Blueprint explains.

Investing in wonderful companies has been key to my success.

But, as I alluded to earlier, getting good deals has also been key to my success.

But, as I alluded to earlier, getting good deals has also been key to my success.

While price is what you pay, it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Investing in a wonderful company when the valuation is also wonderful is a simple action that can lead to tremendous wealth and passive income over the years to come.

Of course, this simple action first requires one to have a basic understanding of valuation already in place.

Fear not.

For anyone looking for help on the valuation process, my colleague Dave Van Knapp put together Lesson 11: Valuation.

It’s part of an overarching series of “lessons” on dividend growth investing, and it lays out a valuation template that can be easily applied toward almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Accenture PLC (ACN)

Accenture PLC (ACN)

Accenture PLC (ACN) is a professional services company specializing in information technology services and consulting.

Founded in 1951, Accenture is now a $183 billion (by market cap) consulting behemoth that employs 738,000 people.

The company reports results across five operating groups: Products, 30% of FY 2022 revenue; Communications, Media & Technology, 20%; Financial Services, 19%; Health & Public Service, 18%; and Resources, 13%.

Accenture is one of the largest IT-services companies in the world, providing a range of consulting, strategy, technology,

operational, and outsourcing services.

Simply put, Accenture helps to solve problems for enterprises.

Properly navigating the digital transformation would be one example.

Formulating a strategy for entering new markets might be another example.

The combinations of enterprises, problems, and solutions are nearly endless.

And that’s what’s so exciting for Accenture and its shareholders.

Enterprises aren’t going away, and neither are problems which need solutions.

In fact, doing business today is more complex and technology-driven than ever before.

This is part of why Accenture has such a rich legacy for revenue, profit, and dividend growth, which looks set to continue for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

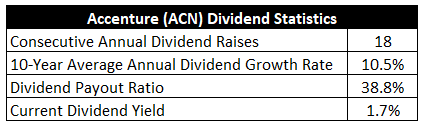

To date, Accenture has increased its dividend for 18 consecutive years.

Will Accenture be a Dividend Aristocrat in seven years?

I believe so.

The 10-year dividend growth rate of 10.5% is impressive.

The 10-year dividend growth rate of 10.5% is impressive.

What’s even more impressive is the acceleration in dividend growth.

The most recent dividend raise of 15.5% is a perfect example of that.

Now, you do have to sacrifice some yield in order to access that high dividend growth rate.

The stock’s yield is only 1.7%.

That said, this is 30 basis points higher than its own five-year average.

And what’s really great about the dividend is the safety of it.

The payout ratio is just 38.8%.

That gives the dividend plenty of room to head higher over the coming years.

For younger dividend growth investors who are interested in compounding their money at a high rate over a long period of time, these dividend metrics perfectly fit the bill.

Revenue and Earnings Growth

As perfect as the metrics may be for some investors, these numbers are also mostly looking backward.

The issue is, investors must look forward and realize that today’s capital is being risked for tomorrow’s rewards.

That’s precisely why I’ll now build out a forward-looking growth trajectory for the business, which will be of great aid when the time comes to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this fashion should allow us to approximate where the business could be going from here.

Accenture moved its revenue from $30.4 billion in FY 2013 to $61.6 billion in FY 2022.

That’s a compound annual growth rate of 8.2%.

Strong top-line growth.

I usually look for a mid-single-digit top-line growth rate from a large, mature business like this.

Accenture shines.

Meanwhile, earnings per share grew from $4.93 to $10.71, which is a CAGR of 9%.

More good stuff from Accenture.

What’s especially remarkable is the way in which that 9% EPS CAGR was achieved – it was almost completely secular, with a steady march upward from year to year.

It’s clockwork-like growth.

We can also see a tight growth correlation between EPS and the dividend over the last decade, which shows excellent control from management.

Looking forward, CFRA believes that Accenture will grow its EPS at a compound annual rate of 9% over the next three years.

Clearly, CFRA is not stepping out on a limb here.

But I actually like that.

Accenture is a model of consistency, as I just alluded to.

CFRA sums up the investment thesis well with this passage: “Accenture is operating at a high level, as it takes share and outgrows operating markets by ~2x. More recently, [Accenture] has been able to buck industry trends around more protracted sales cycles, posting bookings of ~$22B (+13% Y/Y) in [Q2], highlighting its unmatched scale across consulting, integration, and managed services, coupled with its enduring client relationships ([Q2]: 35 with $100M in bookings).”

I mean, I’m not sure what more you can say.

If that doesn’t give you an idea of Accenture’s quality, I’m not sure what will.

However, just in case you need more, CFRA then follows that up with this: “We regard [Accenture] as a high-quality name that holds up well in a slowing macro, due to its diverse industry reach and client relationships, sound financial positioning, and proven track record of compounding earnings at an above-average rate.”

I’ll take CFRA’s projection as the base case.

That sets up Accenture for at least high-single-digit dividend growth over the foreseeable future.

And with the payout ratio being as low as it is, I actually think it’s quite possible – even likely – that we see low-double-digit divided raises over the next few years or so, which would be right in line with Accenture’s recent history.

The dividend growth could then settle into a high-single-digit range thereafter.

Essentially, we’re looking at a compounding machine that’s still full of fuel.

Financial Position

Moving over to the balance sheet, Accenture has an extremely strong financial position.

The long-term debt is negligible, and the interest coverage ratio is almost 170.

Furthermore, Accenture has more than $6 billion in cash and cash equivalents.

This is a pristine balance sheet.

Profitability is magnificent.

Over the last five years, the firm has averaged annual net margin of 11.1% and annual return on equity of 35.1%.

The ROE looks even better when you see that it was achieved without a lot of debt.

Accenture is a terrific business with high returns on capital.

Simply put, the fundamentals here are among the best I’ve ever seen.

And with scale, brand/reputation power, switching costs, industry know-how, entrenched relationships, and IP, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

The company is sensitive to the overall economy, as less businesses and less spending will reduce demand for Accenture’s services.

Consulting firms are uniquely reliant on their employee base, and talent retention is important.

Technology continues to evolve at a rapid pace, which means Accenture must continue to stay ahead of the curve and maintain its edge.

The company’s large scale is an advantage, but it also may start to work against the firm by introducing the law of large numbers.

The work-from-home trend could lead to more decentralized, cloud-based workloads and less growth for Accenture.

Accenture’s reputation carries great value, and the company must guard against anything that would damage this.

A global footprint leads to geopolitical risks and currency exposure.

Overall, in light of the very high quality of the business, I see these risks as manageable.

And with the stock down about 1/3 from its all-time high, the valuation now looks about as attractive as it gets for this name…

Stock Price Valuation

The P/E ratio is sitting at 25.

For this kind of quality and growth, I find that to be quite reasonable.

For perspective, its own five-year average P/E ratio is 28.8.

We can also see a disconnect on the cash flow multiple.

The current P/CF ratio of 7.2 is well off of its own five-year average of 9.1.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 12% dividend growth rate for the next ten years, and a long-term dividend growth rate of 8%.

That strikes me as a reasonable view on Accenture’s near-term and long-term dividend growth potential.

The payout ratio is low, the earnings power is high, and the most recent dividend raise was over 15%.

It’s impossible to say exactly how things will balance out from year to year, but this seems like a realistic expectation over the next decade and beyond.

I wouldn’t be surprised to see Accenture do a bit better than this.

But I would be very surprised to see them do much worse.

The DDM analysis gives me a fair value of $339.22.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I don’t see my valuation model as imprudent, yet the stock still comes out looking pretty cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates ACN as a 3-star stock, with a fair value estimate of $258.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates ACN as a 5-star “STRONG BUY”, with a 12-month target price of $333.00.

I came out very close to where CFRA is at, and I think Morningstar is too conservative on this one. Averaging the three numbers out gives us a final valuation of $310.07, which would indicate the stock is possibly 13% undervalued.

Bottom line: Accenture PLC (ACN) is an ultra high-quality business that has some of the best fundamentals I’ve ever come across. With a market-like yield, a double-digit long-term dividend growth rate, a low payout ratio, almost 20 consecutive years of dividend increases, and the potential that shares are 13% undervalued, this could be a rare window of opportunity to invest in a world-class compounder.

Bottom line: Accenture PLC (ACN) is an ultra high-quality business that has some of the best fundamentals I’ve ever come across. With a market-like yield, a double-digit long-term dividend growth rate, a low payout ratio, almost 20 consecutive years of dividend increases, and the potential that shares are 13% undervalued, this could be a rare window of opportunity to invest in a world-class compounder.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is ACN’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 92. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, ACN’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income