Time flies, doesn’t it?

We’re now into May, almost halfway done with 2023. Compared to the last few years, 2023 has been pretty tame. The S&P 500 is up decently YTD. But there have been some ups and downs along the way, and those downs are especially nice.

Price and yield are inversely correlated. All else equal, lower prices result in higher yields.

This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach. I always see short-term volatility as a long-term opportunity.

That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint. If you’re interested, you can download a free copy of my Early Retirement Blueprint.

All that said, it’s a big market, and some ideas are better than others.

Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for May 2023.

Ready? Let’s dig in.

My first dividend growth stock for May 2023 is Air Products & Chemicals (APD).

Air Products & Chemicals is a major global producer and supplier of industrial gases.

Industrial gases. Doesn’t sound like a great place to make money, does it? Except it is. That’s because industrial gases are critical input for the manufacturing processes of many different end products, and constant, reliable access to various gases is often a requirement for a manufacturer. Being critical, low-cost input practically ensures steady business.

But wait. There’s more.

This company operates within the favorable framework of a global oligopoly, as there are only a few major global providers of industrial gases. This advantageous positioning is a key part of why Air Products & Chemicals has compounded its revenue at an annual rate of 2.5% and its EPS at an annual rate of 9% over the last decade.

It’s also a key part of why this is a vaunted Dividend Aristocrat.

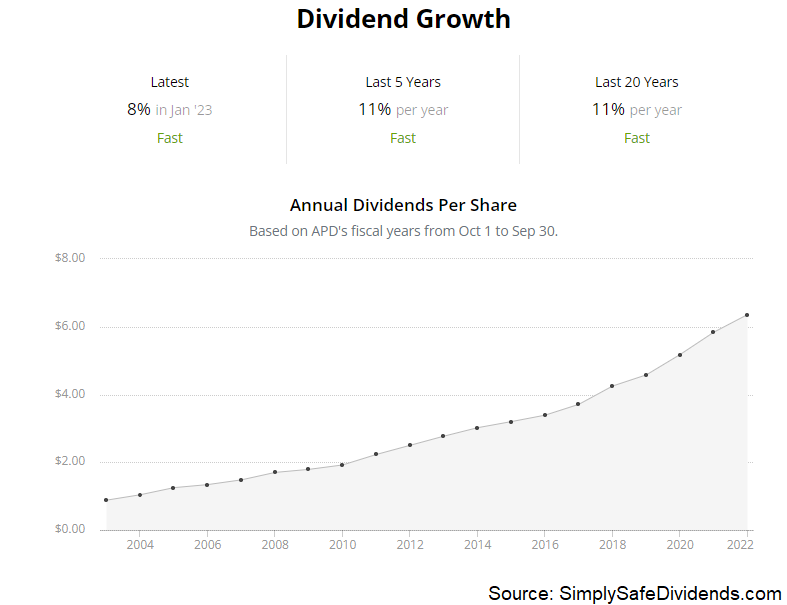

Yes, Air Products & Chemicals is a Dividend Aristocrat, with 41 consecutive years of dividend increases. The 10-year DGR is 9.8%, which is obviously very nice. Better yet, you get to pair that high-single-digit dividend growth with the stock’s starting yield of 2.4%. That’s a great combination of yield and growth. And the payout ratio of 61.7%, based on midpoint adjusted EPS guidance for FY 2023, shows us a healthy dividend.

I think this high-quality dividend growth stock is meaningfully undervalued.

I think this high-quality dividend growth stock is meaningfully undervalued.

We already put together a full analysis and valuation on the business. If the video on that isn’t already live, it should be very soon. In that video, you’ll see why the estimate for intrinsic value comes out to nearly $350/share. This stock is currently selling for about $290.

So it looks about 17% undervalued right now. If you can get shares in this kind of business for almost 20% less than they’re probably worth, you’re almost guaranteed to do very well over the long run. If you don’t already own a slice of Air Products & Chemicals, now would be a great time to consider changing that.

My second dividend growth stock for May 2023 is Broadridge Financial Solutions (BR). Broadridge is a global fintech company.

A lot of investors might not be super familiar with this company’s name, even though they’re almost certainly familiar with its services. Why might they be so familiar? Well, the company’s largest segment mostly includes the processing and distribution of proxy materials to investors that hold positions in equity securities and mutual funds, which is a service that Broadridge dominates.

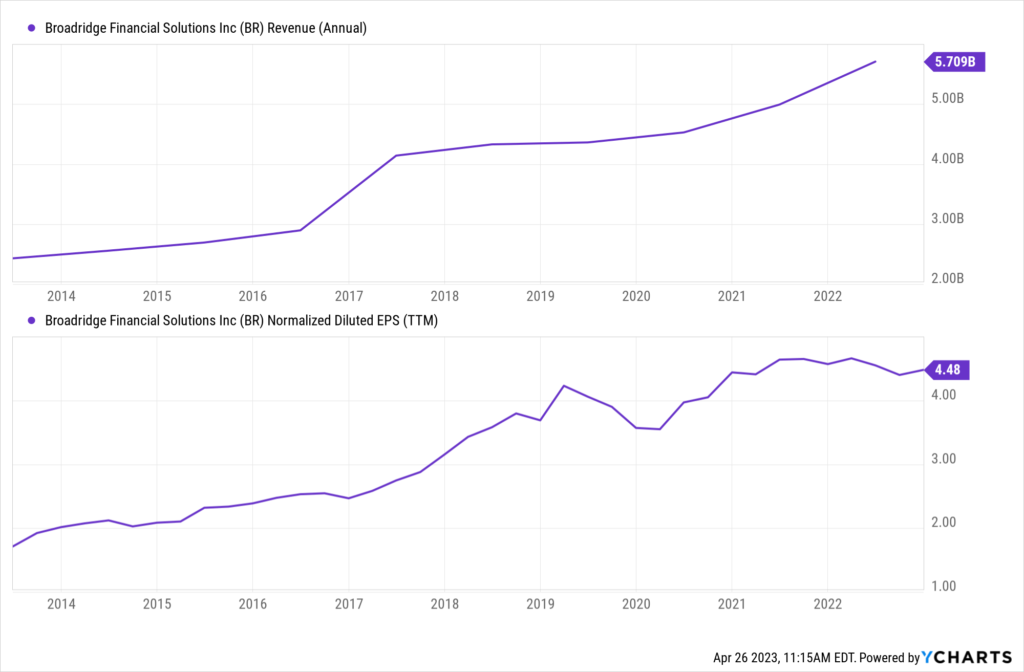

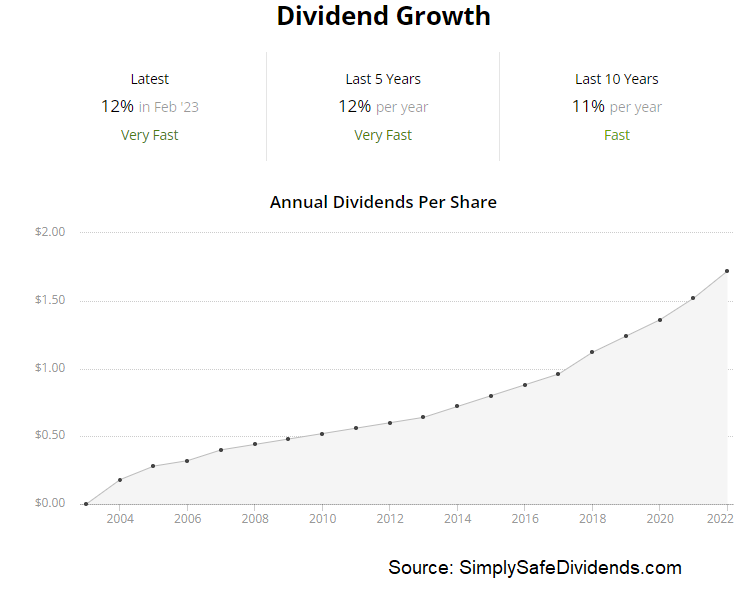

Those communications you get as a shareholder? Broadridge most likely handled them for you. Indeed, Broadridge recently processed more than 80% of domestic shares outstanding through its ProxyEdge platform (the company’s crown jewel). This dominance bleeds through to excellent growth – a 10.1% CAGR for revenue and 11.6% CAGR for EPS over the last decade.

If you think that’s impressive, check out this dividend growth.

If you think that’s impressive, check out this dividend growth.

The 10-year DGR is 14.9%. And there’s no major sign of slowdown here, either, as the most recent dividend raise was 13.3%. At that kind of compounding rate, you’re doubling the dividend roughly every five years. It’s incredible.

Broadridge has increased its dividend for 16 consecutive years, which dates back to its initial 2007 spin-off. This is a consistent compounding machine, which is not easy to find in this world. Now, the payout ratio has become slightly elevated.

At 64.6%, I’d expect future dividend growth to pretty much match EPS growth – no slouch in and of itself. And the 2% yield isn’t super high, but that’s what you give up in order to access the compounding power.

This stock isn’t a steal. It’s not super cheap. But the valuation is more reasonable than it usually is.

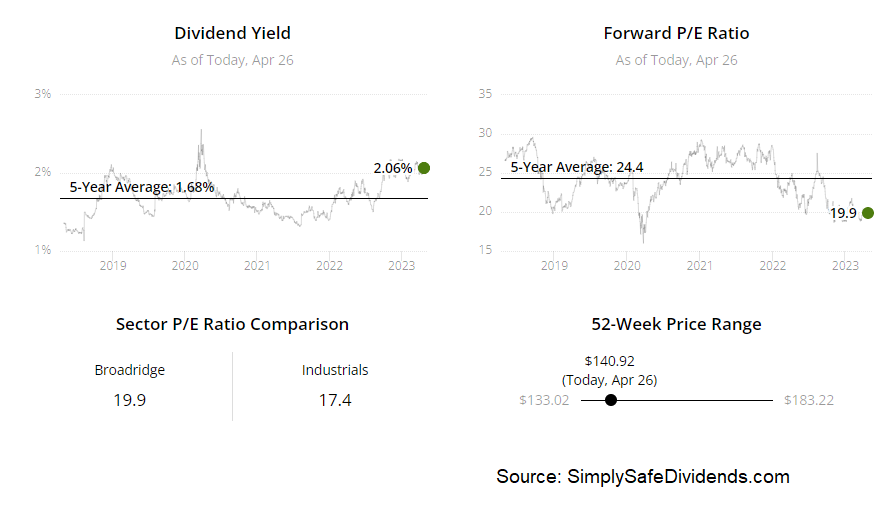

The stock’s P/E ratio right now is 32. Isn’t that way too high? No. Not really. Its own five-year average is even higher – at 33.2. Broadridge has been defying gravity for years. Why? The market sniffed out the market dominance, high returns on capital, and strong growth potential years ago.

While so-called “cheap” stocks flounder because the underlying businesses aren’t doing much, Broadridge continues to put up impressive numbers. We recently analyzed and valued Broadridge, and the video should go live soon. The fair value estimate came out to almost $175/share. The stock is currently priced at around $144. Again, not a steal. But this is a terrific business. And it’s cheaper than it usually is. Take a look.

While so-called “cheap” stocks flounder because the underlying businesses aren’t doing much, Broadridge continues to put up impressive numbers. We recently analyzed and valued Broadridge, and the video should go live soon. The fair value estimate came out to almost $175/share. The stock is currently priced at around $144. Again, not a steal. But this is a terrific business. And it’s cheaper than it usually is. Take a look.

My third dividend growth stock for May 2023 is Crown Castle (CCI).

Crown Castle is an infrastructure real estate investment trust. This is a US-based tower, small cell, and fiber REIT. We’ve been covering American Tower a lot recently on the channel. Crown Castle is like a smaller, domestically-focused version of American Tower.

What’s great about this business model is the way in which income can scale against fixed costs. It comes down to the way in which its real estate can be easily leveraged. Once a tower is built, there is a lot of available scalability in terms of bringing on additional tenants.

Adding tenants, equipment, and upgrades results in much higher returns per tower, as revenue is added with minimal incremental cost. This has helped Crown Castle put up very respectable growth over the last decade – a 10.3% CAGR for revenue, and a 6.3% CAGR for AFFO/share.

The dividend growth is also respectable, but wait until you see the yield.

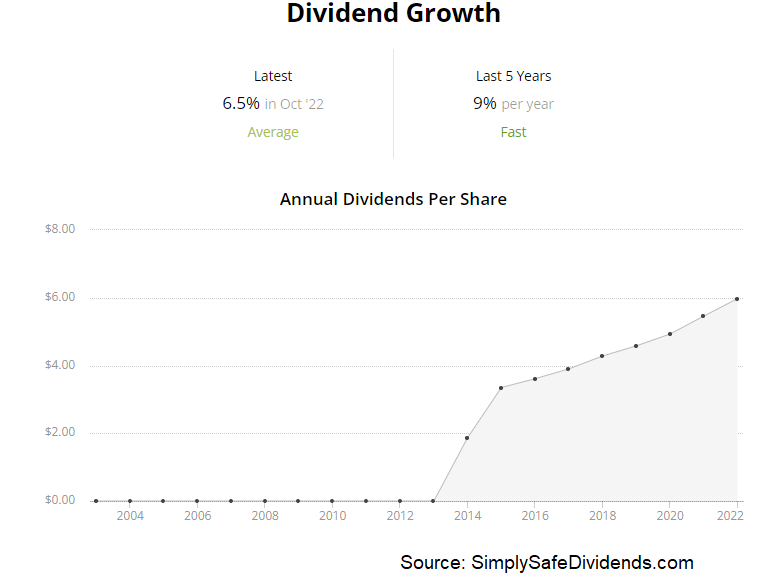

Crown Castle has increased its dividend for nine consecutive years. And the five-year DGR is 8.9%, although we can see the excess there relative to underlying profit growth. As such, it’s not surprising to see a slowdown.

The most recent boost to the dividend came in at 6.5%, which is really what you’d expect to see. That’s good. But it’s the yield that’s really special.

The most recent boost to the dividend came in at 6.5%, which is really what you’d expect to see. That’s good. But it’s the yield that’s really special.

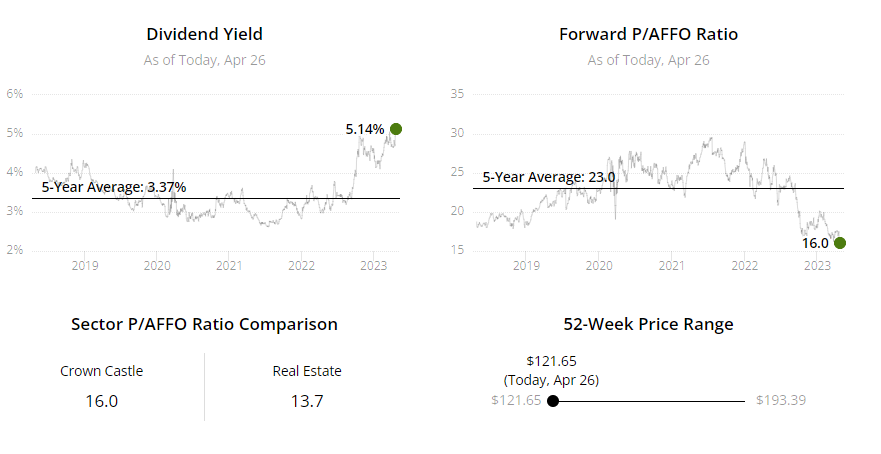

The stock’s 5% yield isn’t high in just absolute terms but also relative terms – this is 170 basis points higher than its own five-year average yield. And based on the AFFO/share outlook for this fiscal year, the payout ratio is 82%. A bit high, but not at all unheard of for a REIT.

This stock is as cheap as I’ve ever seen it. Outside of full-on market crashes, I’ve never seen Crown Castle valued this lowly. The P/CF ratio of 18.7 is well off of its own five-year average of 23.5. Based on that aforementioned outlook, the forward-price-to-adjusted-funds-from-operations ratio is 16.5.

That’s somewhat analogous to a P/E ratio on a normal stock, and it goes to show just how far we’ve sunk with Crown Castle. This has historically been a fast-growing REIT with a premium valuation attached to it.

That’s somewhat analogous to a P/E ratio on a normal stock, and it goes to show just how far we’ve sunk with Crown Castle. This has historically been a fast-growing REIT with a premium valuation attached to it.

Growth has recently been challenged with telecom consolidation. And interest rates have risen. Sure. But the stock has dropped nearly 40% from its 52-week high. If you’ve ever wanted to get into Crown Castle, now might be the best time ever to do just that.

My fourth dividend growth stock for May 2023 is Robert Half International (RHI). Robert Half is a global staffing and consulting company.

Some of my best investments over the last decade have been in companies that really fly way under the radar. To the contrary, a lot of the companies that are constantly in the headlines are often in the news for the wrong reason – because they’re terrible performers.

Well, to this point, Robert Half definitely flies under the radar. And that has a lot to do with its business model of providing talent and consulting solutions. Yawn, right? Well, this business model is an effective, high-margin method for making a lot of money. Indeed, Robert Half has compounded its revenue at an annual rate of 6.2% over the last decade, while its EPS has compounded at an annual rate of 14.2% over that time frame.

The dividend metrics here are stellar. Robert Half has increased its dividend for 20 consecutive years, with a 10-year DGR of 11.1%. Usually, when you see a double-digit dividend growth rate, you also see a low yield. But not in this case. The stock yields 2.6%.

That easily beats the market. It’s also 70 basis points higher than its own five-year average. Want more? Okay. The payout ratio is only 31.8%. Like I said, stellar dividend metrics. I see nothing to nitpick.

That easily beats the market. It’s also 70 basis points higher than its own five-year average. Want more? Okay. The payout ratio is only 31.8%. Like I said, stellar dividend metrics. I see nothing to nitpick.

I think this under-the-radar name is highly undervalued.

Robert Half should almost be renamed “cut in half”, because the stock is 35% off of its 52-week high. But what this has done is, it’s created what appears to be a very favorable valuation. We’ll have a full analysis and valuation video coming out soon on Robert Half, it’s not out already, and this video will go through the whole business and show why the estimate for fair value shakes out to just under $100/share.

The stock is currently priced at about $73. Big upside potential. This company has no long-term debt on the balance sheet. And management announced a massive buyback program in February. Buying the shares alongside the company itself might not be a bad idea at all right now.

My fifth dividend growth stock for May 2023 is Toronto-Dominion (TD). Toronto-Dominion is a Canada-based multinational banking and financial services corporation.

I mean, I had to put at least one bank on today’s list. Banks have been absolutely hammered over the last few weeks following some idiosyncratic bank failures that were more indicative of local mismanagement than widespread banking issues.

Nonetheless, banks large and small got caught up in the misplaced hysteria, and that’s where long-term opportunities can be found. Regarding TD specifically, this is one of the largest Canadian banks. And what a great spot to be in, as Canada basically has a banking oligopoly going on – there are five major banks that absolutely dominate the market up there.

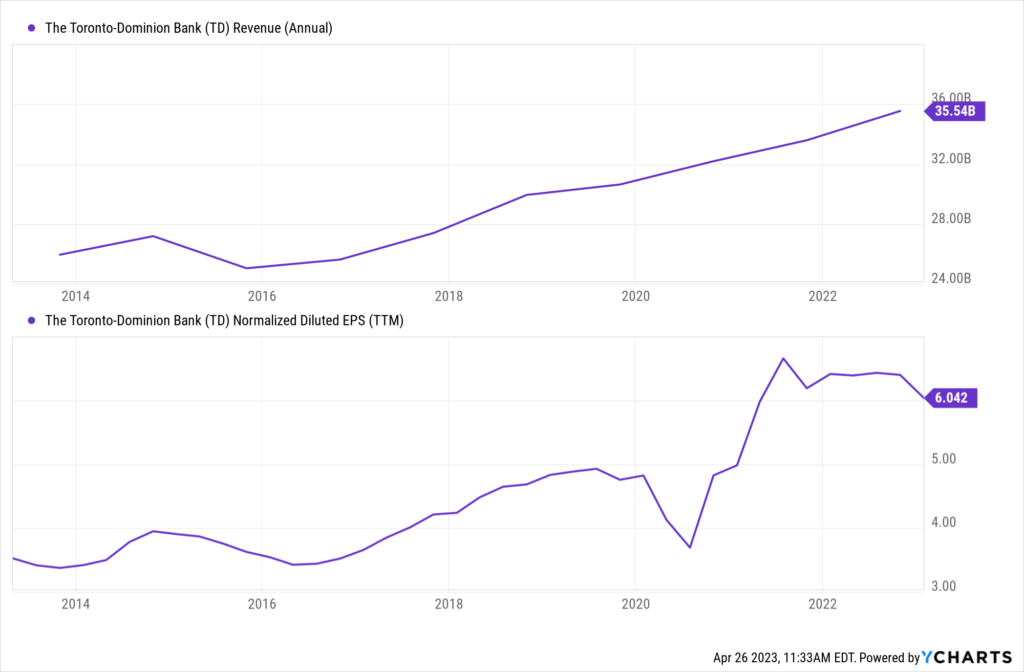

That’s why, despite a really challenging decade for banks, TD put up a 6.7% CAGR for revenue and 11.8% CAGR for EPS over the last 10 years.

TD has a rich dividend history. TD has increased its dividend for nine consecutive years. This short track record doesn’t do the bank’s rich dividend history proper justice.

TD has a rich dividend history. TD has increased its dividend for nine consecutive years. This short track record doesn’t do the bank’s rich dividend history proper justice.

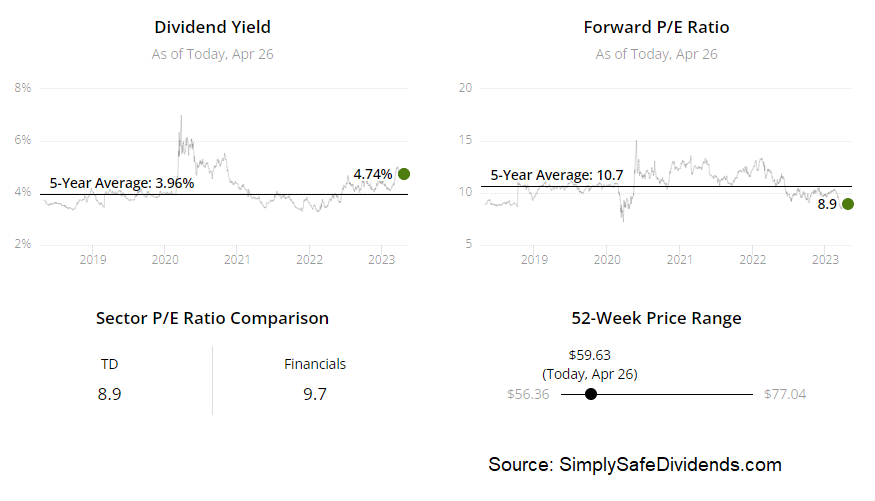

TD, as it exists today, has been formed through a series of mergers, which clouds things, but we can trace a steady dividend payment for more than 160 years. The five-year DGR of 8.7% is solid. But what makes that growth rate especially compelling is the fact that it’s paired with the stock’s market-smashing 4.6% yield. Great combination. And the 46.4% payout ratio gives me no qualms about the sustainability of the dividend.

I view this stock’s unfair punishment as a chance to be opportunistic.

TD had nothing to do with the bank failures that occurred.

Nonetheless, the stock dropped by about 20% in a hurry. We went from a valuation that looked pretty fair to one that looks downright compelling in a matter of only weeks. We already put together the basic content for an upcoming analysis and valuation video on TD, and this video will lay out the case for the bank being worth $75.24/share.

Nonetheless, the stock dropped by about 20% in a hurry. We went from a valuation that looked pretty fair to one that looks downright compelling in a matter of only weeks. We already put together the basic content for an upcoming analysis and valuation video on TD, and this video will lay out the case for the bank being worth $75.24/share.

It was close to that price back in February, but the stock is now priced at around $61. If there were ever a textbook “buy-the-dip” opportunity, this might be it.

— Jason Fieber

Imagine having 12 new monthly income checks, carrying the potential of up to 21% yields.This is possible because of a tested strategy to get paid out regularly, like a paycheck. For over a decade, I have helped more than 26,000 investors secure 12 new monthly payouts. Meaning, you know exactly how much you'll make every month... Because of some stocks that pay us 8%,13.4%, and even 21.6% yields. See it for yourself here.

Source: Dividends & Income