We contrarians, we’re not ashamed to admit, make our big money dumpster diving for discarded dividends.

When vanilla investors toss trash, it is often our treasure!

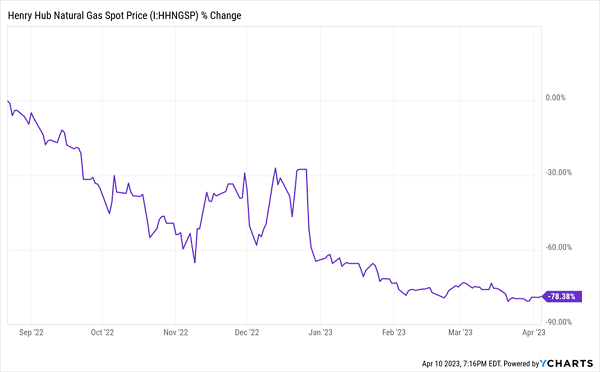

I have a hunch this is unfolding in the natural gas market. Prices literally can’t go much lower, which means that eventually they must go higher. Check out this chart—prices are down by 80% in one year!

Nat Gas is Dirt Cheap

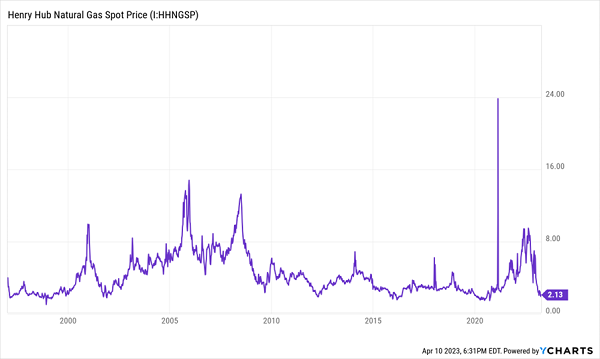

“Natty” prices have fallen from roughly $9 per million British thermal units (MMBtus) to a little more than $2, flattened by unseasonably warm weather and months of dogged supply surplus. Reuters reported in February that “depletion so far this heating season has been around half the seasonal average for the last 10 years.”

“Natty” prices have fallen from roughly $9 per million British thermal units (MMBtus) to a little more than $2, flattened by unseasonably warm weather and months of dogged supply surplus. Reuters reported in February that “depletion so far this heating season has been around half the seasonal average for the last 10 years.”

And current prices aren’t just low—they’re sitting just above a multi-decade floor for natural gas.

It Rarely Gets Much Lower Than This

The cure for these low prices? These low prices.

The cure for these low prices? These low prices.

Producers are slamming on the brakes. Energy equipment firms Liberty Energy (LBRT) and Helmerich & Payne (HP) have already warned about the possibility of lower activity levels this summer. Oil and gas analytics firm Enverus says nat-gas production will grow by 1.7 billion cubic feet per day (bcf/d), down sharply from last year’s 3 billion bcf/d.

Other drivers, both short-term and long, are creeping up too.

Demand in China, the world’s largest importer of nat-gas, could expand once more now that its COVID restrictions have been lifted and travel activity is on the rebound.

Then there’s the changing global picture. Wells Fargo notes that in 2021, before going to war with Ukraine, that Russia accounted for a little more than 41% of the European Union’s natural gas imports. By November 2022, it was down to 12.9%.

A prime beneficiary: The U.S., whose liquefied natural gas (LNG) exports to the EU jumped 61% in that time. And the European Union continues to build up its infrastructure; the U.S. Energy Information Administration expects that the EU’s LNG import capacity will swell by 34% between 2021 and 2024.

All of the above represents a potential spark in numerous natty names—some more smudged than others during this natural gas crash, but all of which are throwing off great to downright garish yields right now:

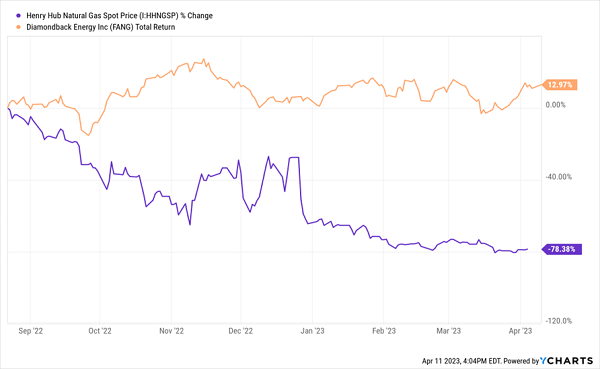

Diamondback Energy (FANG, 7.8% yield), for instance, is a Permian Basin exploration-and-production firm that works primarily in the Wolfcamp, Spraberry and Bone Spring formations, and its low production costs make it attractive in low-price environments … but downright mouthwatering should nat-gas prices bounce back. I’ll note that Diamondback isn’t a pure-play natural-gas play—a slight majority (53%) of its proved reserves is oil, but the remainder is basically split between natural gas and natural gas liquids (NGLs).

Diamondback Energy (FANG, 7.8% yield), for instance, is a Permian Basin exploration-and-production firm that works primarily in the Wolfcamp, Spraberry and Bone Spring formations, and its low production costs make it attractive in low-price environments … but downright mouthwatering should nat-gas prices bounce back. I’ll note that Diamondback isn’t a pure-play natural-gas play—a slight majority (53%) of its proved reserves is oil, but the remainder is basically split between natural gas and natural gas liquids (NGLs).

FANG’s low costs and diversified products has helped it stay afloat despite natty’s plunge.

Diamondback Slithers to Safety

Diamondback is one of several energy stocks that have transitioned to a fixed-plus-variable dividend—a more prudent and responsible model for an industry that’s heavily reliant on whipsaw commodity prices. Its 75-cent regular dividend comes out to a 2.1% yield; the past 12 months’ worth of variable payouts bump that yield up to nearly 8%. This makes for a much more financially sound firm, though it’s unfortunate you can only truly count on about a quarter of its yield.

Diamondback is one of several energy stocks that have transitioned to a fixed-plus-variable dividend—a more prudent and responsible model for an industry that’s heavily reliant on whipsaw commodity prices. Its 75-cent regular dividend comes out to a 2.1% yield; the past 12 months’ worth of variable payouts bump that yield up to nearly 8%. This makes for a much more financially sound firm, though it’s unfortunate you can only truly count on about a quarter of its yield.

More common among high-yield natural gas plays are the “energy toll bridges”—midstream companies. They don’t make the stuff, nor do they sell the stuff. They simply get the natural gas from Point A to Point B, maybe help store it, and take a fee for their troubles.

Western Midstream Partners LP (WES, 7.4%), for instance, manages 23 gathering systems, 72 processing and treating facilities, and 15,389 miles of pipeline spread across six natural gas pipelines and 15 crude oil and NGL pipelines. This infrastructure is largely spread across the southwestern and western U.S., as well as Pennsylvania. While WES did deliver slightly disappointing 2023 guidance, it did cheer investors by announcing it expected to pay a 36-cent “enhanced distribution” for 2022 that would be paid out alongside WES’s 50-cent regular distribution, tacking on another 1.3 percentage points’ worth of yield.

The downside? Western is a master limited partnership (MLP) that comes with the added complication of a K-1 tax form, which I try to avoid.

Plenty of nat-gas players allow you to avoid the K-1, however.

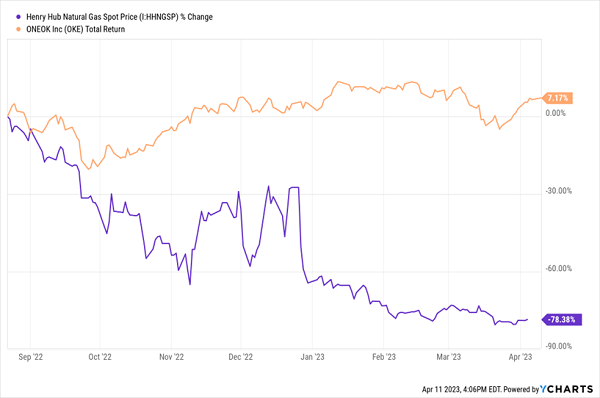

One of them is ONEOK (OKE, 5.8% yield), which boasts a roughly 40,000-mile network of natural gas and NGL pipelines and says more than 10% of U.S. nat-gas production is reliant on ONEOK’s infrastructure.

ONEOK is a favorite of mine. We added OKE to our Contrarian Income Portfolio in April 2020, and we’re sitting on 175%+ total returns since then. I’m also happy to report that it has held its own during the natural-gas price crash, sitting in the black since the August 2022 Henry Hub highs. Also, OKE’s payout isn’t just plump—it has grown by 12% annually since 2000, and it hasn’t suffered a cut in more than 25 years.

ONEOK Is Treading Water—But Watch Out When Natural Gas Prices Pop!

Kinder Morgan (KMI, 6.2% yield) is another venerable pipeline name. It’s an energy infrastructure titan, with 82,000 miles of pipelines, 140 terminals, and 700 billion cubic feet of working nat-gas storage capacity. While natural gas is its primary business, KMI also transports and/or stores crude oil, LNG, NGLs, renewable fuels, refined petroleum products, and more.

Kinder Morgan (KMI, 6.2% yield) is another venerable pipeline name. It’s an energy infrastructure titan, with 82,000 miles of pipelines, 140 terminals, and 700 billion cubic feet of working nat-gas storage capacity. While natural gas is its primary business, KMI also transports and/or stores crude oil, LNG, NGLs, renewable fuels, refined petroleum products, and more.

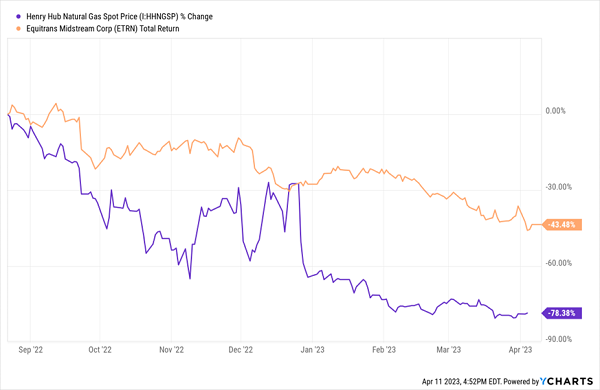

Less well-known than Kinder is Equitrans Midstream (ETRN, 11.8% yield), which is one of the continent’s largest natural gas gatherers, and also has a number of transmission and storage assets in Ohio, West Virginia and Pennsylvania.

Equitrans offers a wild double-digit yield at current prices. That’s largely an effect of the massive hit ETRN shares have taken—the stock has been cut nearly in half amid the slump in natural gas.

Equitrans Hasn’t Been Able to Outrun the Nat-Gas Bear

ETRN has been weighed down by more than just nat-gas prices, of course. The company’s Mountain Valley Pipeline (MVP) project, which was expected to be finished in 2018, has been delayed numerous times by legal challenges and has gone billions of dollars over budget.

ETRN has been weighed down by more than just nat-gas prices, of course. The company’s Mountain Valley Pipeline (MVP) project, which was expected to be finished in 2018, has been delayed numerous times by legal challenges and has gone billions of dollars over budget.

The potential snap-back is high, especially if Equitrans can finally see its MVP to completion. But it’s simultaneously a very high-risk way to bet on an eventual comeback in natural gas.

Yours in a dividend-powered retirement,

Brett Owens

This Instantly Gets You an “All-Weather” 9.5% Dividend (Paid Monthly!) [sponsor]

As I mentioned above, a mess like the one we’re seeing at SIVB demonstrates the power of safe—and monthly!—CEF dividends.

That, plus a high 9.5% current yield, is exactly what you get in the 4-CEF “mini-portfolio” I’ve constructed. With just shy of 10% of your investment boomeranging back to you in the form of a monthly dividend every year, you can relax and collect your checks—and tune out the market noise!

I’d love to show you these 4 funds right here, right now. But they’re all recommendations of my CEF Insider service, and that wouldn’t be fair to my paying members. So I’m going to do the next best thing:

Simply click here and I’ll take you to a page that gives you a guided tour of this portfolio and reveals my full CEF-investing strategy. Then I’ll show you how to download your own copy of an exclusive Special Report revealing these 4 CEFs’ names, tickers, best-buy prices and all of my research.

Don’t miss your chance to buy these four 9.5%-paying CEFs while the SIVB crisis has made them ridiculously cheap.

Source: Contrarian Outlook