Some investors like to run concentrated portfolios.

Think just 10 or 20 stocks.

It’s hard for me to imagine taking on that kind of single-stock risk.

Moreover, one is assuming a lot of possible opportunity cost with that kind of approach.

After all, there are hundreds, if not thousands, of truly terrific businesses out there.

Want to see what I mean?

Take a look at the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

These are dividend growth stocks.

Let’s break it down quickly.

It takes a special kind of business to be able to routinely grow its dividend.

That’s because it takes a special kind of business to be able to routinely grow its profit, which is what’s necessary to fund a dividend that’s routinely growing.

Okay.

Guess what?

There are over 700 stocks on that list!

I’m not saying that every stock on the list is buyable today… or even investable, in general.

That’s up to you to decide.

But to artificially and unnecessarily limit oneself to 10 or 20 from over 700 seems awfully bullheaded to me.

I’ve been buying a broad range of high-quality dividend growth stocks for years now.

I’ve been buying a broad range of high-quality dividend growth stocks for years now.

In doing so, I built out FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

And since I do live off of dividends, I like having that portfolio broadly diversified and protected against possible issues with any one single business.

I’d argue it’s partly because of broad diversification that I’ve been able to live off of dividends for years now.

I actually retired in my early 30s.

I actually retired in my early 30s.

And my Early Retirement Blueprint shares how I did that.

Suffice it to say, owning a broad basket of high-quality dividend growth stocks has been crucial to my financial success.

But that’s not all.

Buying specific stocks at specific valuations has been a huge part of it.

Price relates to what you pay, but value relates to what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Building a diversified portfolio of high-quality dividend growth stocks, and doing the stock buying when undervaluation is present, can allow you to achieve, and maintain, financial freedom over the long haul.

Admittedly, that endeavor requires one to first understand the basics of valuation.

Fortunately, it’s not all that hard.

My colleague Dave Van Knapp made it even easier after introducing his Lesson 11: Valuation.

Part of a more comprehensive series of “lessons” on dividend growth investing, it provides a valuation template that can be applied toward almost any dividend growth stock you’ll run into.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Air Products & Chemicals, Inc. (APD)

Air Products & Chemicals, Inc. (APD)

Air Products & Chemicals, Inc. (APD) is a major global producer and supplier of industrial gases. They’re the largest supplier of hydrogen and helium in the world.

Founded in 1940, Air Products & Chemicals is now a $64 billion (by market cap) industrial gases giant that employs more than 20,000 people.

The company’s FY 2022 sales were reported through four Industrial Gases business segments organized by geography: Americas, 42%; Asia, 25%; Europe, 24%; and Middle East and India, 1%. Corporate and other accounted for the remainder.

This business model is super appealing.

I’ll give you four reasons why.

First, industrial gases are critical input for the manufacturing processes of many different end products, and constant, reliable access to various gases is often a requirement for a manufacturer.

Second, because of the critical nature of these industrial gases, a manufacturer is keen to set up a long-term contract with a dependable provider of these gases.

Third, part and parcel of reliably providing gases, complex infrastructure often has to be installed at a manufacturing site in order to ensure constant supply, which makes it costly and difficult to switch providers later.

Fourth, Air Products & Chemicals is part of a global oligopoly – only three major companies command the majority of worldwide market share.

Those four aspects can be summed up like this: Air Products & Chemicals combines necessary input with long-term contracts fortified by complex infrastructure within the advantageous envelope of a global oligopoly.

Put simply, Air Products & Chemicals operates a business model that is about as bulletproof as it gets.

And what that means is, shareholders are set up to experience fantastic results over the decades to come, which should include plenty of safe, growing dividend income.

Dividend Growth, Growth Rate, Payout Ratio and Yield

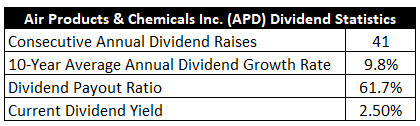

Already, the company has increased its dividend for 41 consecutive years.

That easily qualifies the company for its status as a respected Dividend Aristocrat.

The 10-year dividend growth rate is 9.8%, which is pretty strong.

The 10-year dividend growth rate is 9.8%, which is pretty strong.

Better yet, there’s been a lot of consistency here with little signs of a slowdown.

And you get to layer that growth on top of the stock’s market-beating yield of 2.5%.

By the way, that yield is 30 basis points higher than its own five-year average.

A payout ratio of 61.7%, based on midpoint adjusted EPS guidance for FY 2023, indicates a well-covered dividend.

I like dividend growth stocks in what I call the “sweet spot” – that’s a yield of between 2.5% and 3.5%, paired with a high-single-digit (or higher) dividend growth rate.

We’re clearly in the sweet spot here.

Revenue and Earnings Growth

As sweet as the dividend metrics may be, we’re also looking mostly backward.

However, investors must look forward and risk today’s capital for the rewards of tomorrow.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be very important when it comes time to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Fusing the proven past with a future forecast in this manner should give us the ability to roughly compute where the business may be going from here.

Air Products & Chemicals moved its revenue up from $10.2 billion in FY 2013 to $12.7 billion in FY 2022.

That’s a compound annual growth rate of 2.5%.

I usually like to see mid-single-digit top-line growth from a mature business like this.

But, in this case, I’m not disappointed.

Management made a decision to purposely make the business smaller and more efficient through what was called the “Five-Point Plan”, which was introduced in 2014.

This plan focused operations on industrial gases by jettisoning non-core businesses.

Executing this plan led to spinning off the electronics material division in 2016, and the performance materials division was then sold in 2017 for $3.8 billion in cash.

We can see how well the plan has worked out.

Earnings per share grew from $4.68 to $10.14 over this period, which is a CAGR of 9%.

Significant, steady margin expansion can explain a lot of this excess bottom-line growth, vindicating management’s choices.

We can also see h0w well dividend growth lines up with EPS growth over the last decade, showing more great command by management.

Looking forward, CFRA forecasts that Air Products & Chemicals will compound its EPS at an annual rate of 12% over the next three years.

This is measurably higher than the growth rate that the company produced over the last decade.

But I don’t think it’s an unreasonable expectation.

And I say that because it’s more of a continuation of the bottom-line growth acceleration that’s been playing out over the last few years.

Said another way, it’s more status quo than one might initially be led to believe.

The company is highly exposed to secular growth tailwinds that cannot be underestimated.

CFRA puts it like this: “We think [Air Products & Chemicals] has a solid backlog of growth projects, with a focus on expanding the scope of syngas supply agreements, acquiring air separation units, and winning agreements in large industrial gas projects.”

Speaking on that backlog, it’s currently over $15 billion.

In addition, new growth avenues that didn’t even exist 10 years ago are now opening up for the company, which further supports the growth acceleration thesis.

CFRA speaks on this: “[Air Products & Chemicals] is well positioned to capitalize on [gasification] related to carbon capture and hydrogen mobility, which are long-term secular tailwinds.”

The green hydrogen story is huge.

The company’s multibillion JV with Saudi Arabia’s ACWA Power and NEOM on the world’s largest green hydrogen plant in Saudi Arabia is a prime example of this.

There’s also the new $4 billion JV green hydrogen production facility in Texas.

This was already a very good business 10 years ago, but it’s improving it through renewed focus on its core strengths, and then it’s adding on new growth vectors.

I see extremely favorable conditions here for Air Products & Chemicals.

If the company is able to grow its EPS at a low-double-digit rate over the foreseeable future, that easily sets up the dividend to continue growing at the high-single-digit rate shareholders have been accustomed to.

When starting off with a 2.5% yield, you can get to a double-digit annualized total return pretty quickly.

Hard to dislike any of this.

Financial Position

Moving over to the balance sheet, the company has a great financial position.

The long-term debt/equity ratio is 0.5, while the interest coverage ratio is over 21.

Profitability is robust, and it’s only been getting better.

Over the last five years, the firm has averaged annual net margin of 19.3% and annual return on equity of 15.9%.

I want to quickly point out that net margin was closer to 10% a decade ago.

This speaks on just how successful management has been with its margin expansion efforts.

In almost every single way, this is a terrific business.

And with global economies of scale, large barriers to entry, high switching costs, a global oligopoly, and long-term contracts with fixed infrastructure, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

A recession, which some believe is coming soon, would impact the business, as demand for industrial gases is correlated with manufacturing activity.

Since the company is heavily involved in a variety of major energy projects around the world, ongoing changes in the global energy complex adds uncertainty.

Input costs can be volatile.

More than half of the company’s sales come from outside the Americas, which exposes the company to currency moves and geopolitical risks.

Joint ventures are employed in order to help fund growth projects, but the financial health/commitment of partners may vary over time.

Overall, I see the risks here as quite acceptable when weighed up against the attractive growth and quality offered by the business.

And with the stock down almost 15% from its 52-week high, the valuation being offered up also looks attractive…

Stock Price Valuation

The forward P/E ratio is 25, based on FY 2023 adjusted EPS guidance at the midpoint.

The five-year average P/E ratio for the stock is 28.7.

We can also see a favorable P/S ratio of 4.9 relative to its own five-year average of 5.5.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

This 8% mark is as high as I’ll go, but I believe this is a business that deserves the designation.

The demonstrated dividend and EPS growth over the last decade are both higher than this level.

And we’re seeing an acceleration in EPS growth playing out, as CFRA notes with its near-term EPS growth projection.

If the next decade ends up simply being like the the last decade, I’d say my model is realistic.

But the next decade could actually be much better than the last decade, which starts to make my model look fairly conservative.

I will note that the most recent dividend raise was 8% on the dot.

Balancing things out, I think this kind of expectation is very reasonable.

The DDM analysis gives me a fair value of $378.00.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I put together a pretty sensible valuation, yet the stock’s valuation still comes out looking low.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates APD as a 4-star stock, with a fair value estimate of $319.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates APD as a 5-star “STRONG BUY”, with a 12-month target price of $347.00.

I was high this time around, which surprises me a bit, but we all agree that the stock should have a 3-handle on it. Averaging the three numbers out gives us a final valuation of $348.00, which would indicate the stock is possibly 18% undervalued.

Bottom line: Air Products & Chemicals, Inc. (APD) is a terrific business benefiting from powerful economics and secular tailwinds within a global oligopoly. With a market-beating yield, a near-double-digit dividend growth rate, a moderate payout ratio, more than 40 consecutive years of dividend increases, and the potential that shares are 18% undervalued, this Dividend Aristocrat is a compelling idea for long-term dividend growth investors.

Bottom line: Air Products & Chemicals, Inc. (APD) is a terrific business benefiting from powerful economics and secular tailwinds within a global oligopoly. With a market-beating yield, a near-double-digit dividend growth rate, a moderate payout ratio, more than 40 consecutive years of dividend increases, and the potential that shares are 18% undervalued, this Dividend Aristocrat is a compelling idea for long-term dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is APD’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 95. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, APD’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income