Look, I like being productive as much as anyone else. A life of pure leisure is a pretty boring and unfulfilling life, in my opinion. But getting paid for doing nothing at all?

It’s hard to complain about that. Getting paid ever-more money for doing nothing?

Now we’re really talking.

Well, that’s the life of a dividend growth investor. When you own shares in world-class businesses paying safe, growing dividends, you’re getting paid ever-more money for doing nothing other than not selling those shares.

That’s so easy, even I can do it. When you collect enough safe, growing dividend income to cover your bills, you’re financially free. And financial freedom is worth more than any luxury product or service you could possibly think of.

Today, I want to tell you about 6 dividend growth stocks that just increased their dividends.

Ready? Let’s dig in.

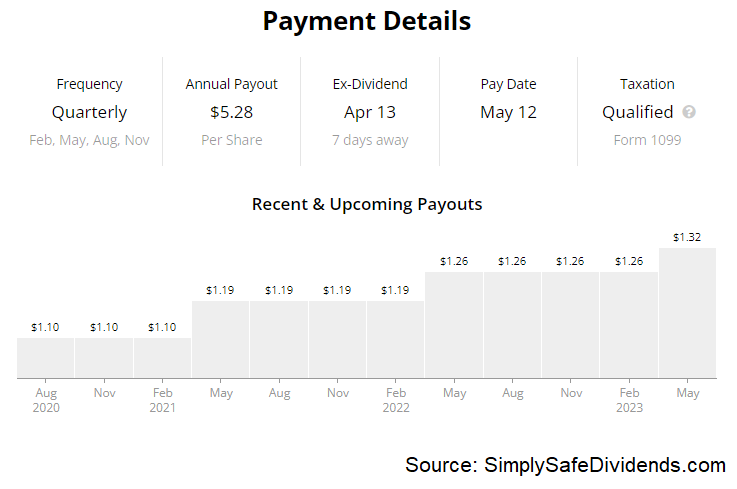

The first dividend increase we have to talk about is the one that was announced by General Dynamics (GD).

General Dynamics increased its dividend by 4.8%. A bit smaller than I was expecting from General Dynamics, which used to be known as “generous dynamics” way back in the day, but let’s keep things in perspective – this was still a “pay raise” for doing nothing other than holding shares in a great business.

This marks the 32nd consecutive year of dividend increases for the aerospace and defense corporation.

Yep. This is a Dividend Aristocrat. Been one since 2017. And I think it’ll remain one for a long time to come. The 10-year DGR is 9.5%, which is obviously really solid, but recent dividend raises have been in this mid-single-digit range.

Yep. This is a Dividend Aristocrat. Been one since 2017. And I think it’ll remain one for a long time to come. The 10-year DGR is 9.5%, which is obviously really solid, but recent dividend raises have been in this mid-single-digit range.

That largely comes down to the fact that the aerospace side of the business – i.e., Gulfstream – was severely impacted by the pandemic. But defense is strong, contracts keep rolling in, the backlog is over $90 billion, and aerospace is rebounding. Meantime, the stock offers a 2.3% yield that’s protected by a healthy 43.3% payout ratio.

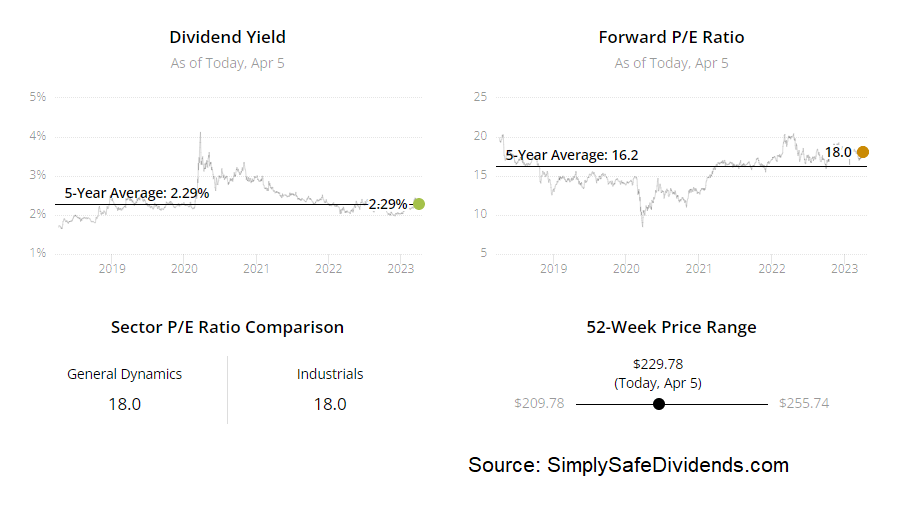

This stock is down nearly 10% YTD, and the valuation looks pretty reasonable here. I see no expensiveness. The P/E ratio of 18.7 is certainly not egregious, although it does trail its own five-year average of 16.8. Then again, this stock spent a good period of time in the penalty box as a result of the aforementioned troubles around aerospace, and that drags down the average valuation.

We can see a sales multiple of 1.6, which is just slightly ahead of its own five-year average of 1.5. Overall, this Dividend Aristocrat strikes me as a good long-term investment candidate for dividend growth investors. You’ve got a huge backlog and a rebound in aerospace. And it’s not terribly expensive.

We can see a sales multiple of 1.6, which is just slightly ahead of its own five-year average of 1.5. Overall, this Dividend Aristocrat strikes me as a good long-term investment candidate for dividend growth investors. You’ve got a huge backlog and a rebound in aerospace. And it’s not terribly expensive.

The second dividend increase we have to cover is the one that came in from Linde PLC (LIN).

Linde just increased its dividend by 9%. This company is just so, so consistent. It’s a beautiful thing. If you’re a long-term dividend growth investor, Linde is exactly the kind of business you want working for you so you don’t have to.

The global industrial gases company has increased its dividend for 30 consecutive years.

Yet another Dividend Aristocrat doing what Dividend Aristocrats do best – relentlessly increase the dividend. The 10-year DGR is 7.8%. Nice to see a dividend raise that’s even higher than that already-acceptable level.

The one thing you do have to sacrifice here, though, is yield – the 1.4%. yield might leave something to be desired. But this isn’t some high-yield junk stock. It’s a high-quality compounder that continues to make investors wealthy. With the payout ratio sitting at 38.2%, based on midpoint guidance for FY 2023 adjusted EPS, I foresee many more years of compounding that dividend.

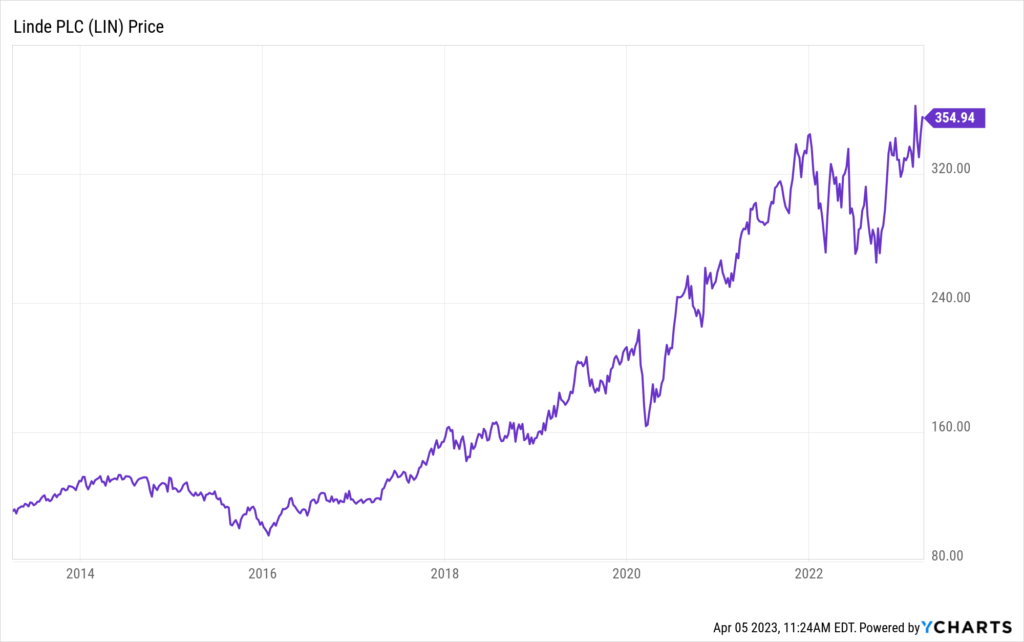

This stock isn’t cheap. But why should it be?

This stock isn’t cheap. But why should it be?

I’ve said it before, and I’ll say it again: You tend to get what you pay for. We recently analyzed and valued this business, estimating fair value at slightly over $351/share. That video highlighted Linde when its shares were trading hands for about $329/each. So I saw a favorable gap between price and value. But a lot of the comments kept going on about how expensive the stock was.

Yet here we are, and the stock has run even higher – now sitting at $355. What else has happened since that video went out? A solid Q4 report with impressive FY 2023 guidance. And this 9% dividend raise, of course, which makes the stock that much more appealing than it was when the video came out. This stock is up 150% over the last five years alone. If you’ve been sleeping on Linde, now might be a good time to consider waking up.

The third dividend growth stock to have a quick discussion about is the one that came courtesy of Realty Income (O).

Realty Income just increased its dividend by 0.2%.

0.2%? What gives? I’ll tell you what gives. Realty Income tends to increase its dividend multiple times per year. And they add up, as I’m about to show you.

This is the 30th consecutive year in which the real estate investment trust has increased its dividend.

Here we go again. Another Dividend Aristocrat. Notice a trend yet? Okay. So let’s break it down. The 10-year DGR is 5.3%. Like I said, those small dividend raises, when they’re coming in many times per year, can really add up. Indeed, the dividend is already up 2.6% on a YOY basis YTD.

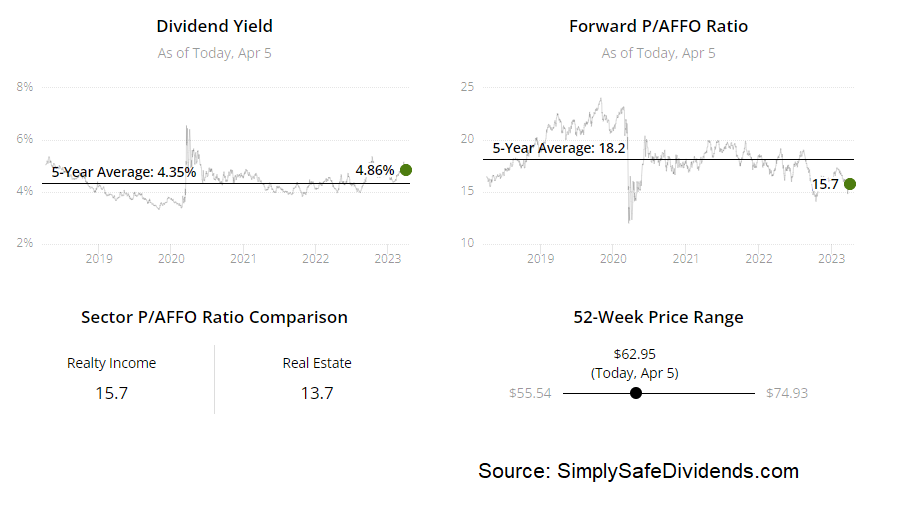

We’re about halfway there to the 10-year DGR. Ahead of schedule. You know what else comes in many times per year? The dividend itself. That’s because Realty Income pays its dividend monthly. So that’s a monthly dividend being raised multiple times per year. If that isn’t awesome, I don’t know what is. Oh, and the stock yields 4.8%. Very decent income here. Based on midpoint guidance for FY 2023 FFO/share, the payout ratio is 75.2%. That’s right about what I’d expect for a REIT.

This stock is priced quite a bit lower than it was before the pandemic hit.

And that’s despite the business and dividend advancing. This was an $80 stock in early 2020. It’s currently a $63 stock. Interest rates are quite a bit higher now, I get it. But this stock was in the doldrums even before the rate-hiking cycle took off. I’m really not sure why the market continues to punish this name. However, that could be just the opportunity long-term dividend growth investors are looking for.

And that’s despite the business and dividend advancing. This was an $80 stock in early 2020. It’s currently a $63 stock. Interest rates are quite a bit higher now, I get it. But this stock was in the doldrums even before the rate-hiking cycle took off. I’m really not sure why the market continues to punish this name. However, that could be just the opportunity long-term dividend growth investors are looking for.

Based on that aforementioned guidance, the forward price-to-funds-from-operations ratio is only 15.6. That’s somewhat analogous to a P/E ratio on a normal stock. We can also see that the P/CF ratio is 15.1, which is close to what I just mentioned. This stock’s five-year average P/CF ratio is 19.6. We are way off of that. In my view, Realty Income is very attractive right now, especially for income-oriented dividend growth investors.

The fourth dividend increase I have to bring up today is the one that came in from Oracle Corporation (ORCL).

Oracle just increased its dividend by 25%.

Boom. Old tech dropping the hammer. While a lot of flashy new tech businesses get headlines, in spite of not making any money, stodgy tech companies like Oracle continue to make a lot of money and reward their shareholders with generous dividend raises.

This is the 15th consecutive year of dividend increases for the multinational database management company.

With a 10-year DGR of 18.2%, you can see that huge dividend raises are nothing new for Oracle. However, oftentimes, you’ll see a deceleration in dividend growth from such a high starting rate. Not in this case, obviously, as this 25% dividend raise was actually an outsized one. Now, you do have to give up some yield in order to access that dividend growth – the stock yields only 1.7%. But Oracle has been an underrated compounder. And with a balanced payout ratio of 52.8%, the dividend is positioned to continue compounding away.

With a 10-year DGR of 18.2%, you can see that huge dividend raises are nothing new for Oracle. However, oftentimes, you’ll see a deceleration in dividend growth from such a high starting rate. Not in this case, obviously, as this 25% dividend raise was actually an outsized one. Now, you do have to give up some yield in order to access that dividend growth – the stock yields only 1.7%. But Oracle has been an underrated compounder. And with a balanced payout ratio of 52.8%, the dividend is positioned to continue compounding away.

This stock has gone on a huge run, and I’d like to see a pullback before buying shares.

The stock is up by more than 40% over just the last six months alone. As a result, it may have gotten ahead of itself. The P/E ratio of 30.9 is looking rich to me, even by Oracle’s standards. The five-year average P/E ratio is 27.1. And it’s not just an earnings thing. Every other multiple that I see is running ahead of its respective recent historical average. Great business. Not-so-great valuation. I’d wait for a better price.

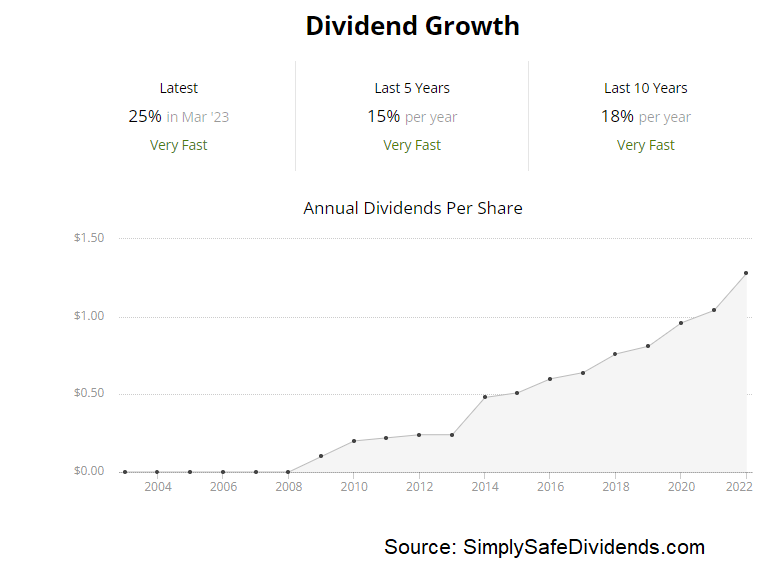

The fifth dividend increase I have to bring to your attention is the one that was announced by Qualcomm (QCOM).

Qualcomm just increased its dividend by 6.7%.

That’s right about where inflation is running at in the US on a YOY basis. And so what that means is, Qualcomm shareholders are seeing their purchasing power remain intact. Sure, something closer to 10% would be better. But let’s keep some perspective. It’s a near-7% bump in pay for sitting on your hands. And the dividends are paid while you sit on your hands. Tough to complain about any of that.

The global technology company has now increased its dividend for 21 consecutive years.

Qualcomm has been such a reliable dividend raiser. I remember back when I first started investing in 2010, many investors thought tech was a risky place for capital allocation. But that’s been proven to be the wrong way to look at it.

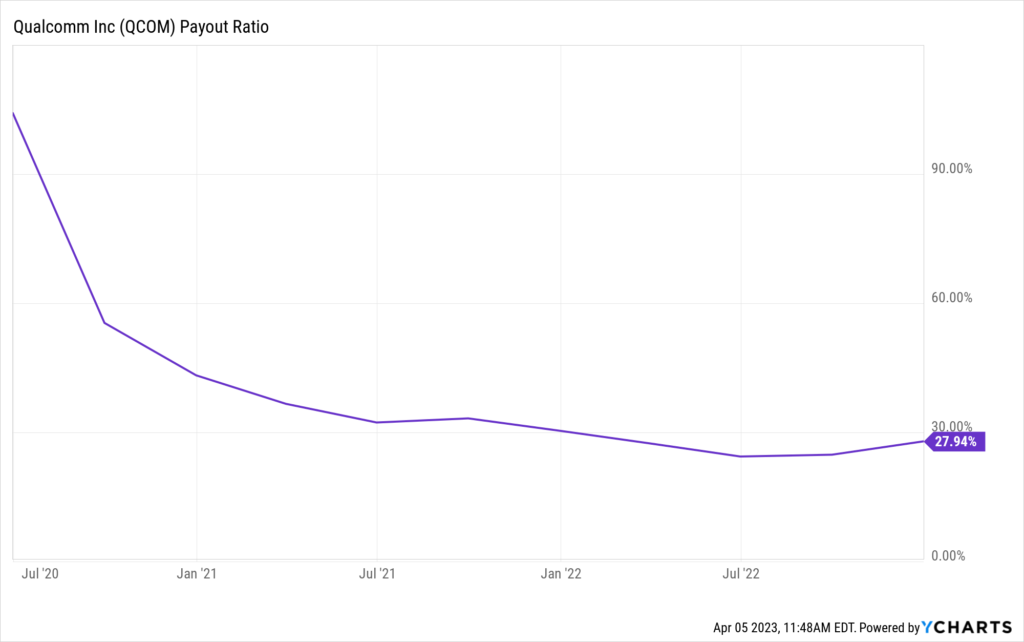

With a 10-year DGR of 11.7%, this most recent dividend increase was a bit smaller than one might expect. Still, you’re pairing that high-single-digit raise with the stock’s yield of 2.4%. Not a bad combination at all. And the payout ratio is only 30.9%, even after this dividend raise, which gives the company plenty of room for more large dividend increases in the years ahead.

In my view, Qualcomm is extremely attractive for long-term dividend growth investors. You don’t often see quality and cheapness paired together. But that’s what you’ve got here with Qualcomm. The company has nearly doubled its revenue over the last decade. EPS has nearly tripled over that period. The healthy dividend continues to move up like clockwork.

In my view, Qualcomm is extremely attractive for long-term dividend growth investors. You don’t often see quality and cheapness paired together. But that’s what you’ve got here with Qualcomm. The company has nearly doubled its revenue over the last decade. EPS has nearly tripled over that period. The healthy dividend continues to move up like clockwork.

And yet the business is slapped with an earnings multiple of 12. I think that’s vastly underestimating and undervaluing this business. For perspective, its five-year average P/E ratio is 24.4. So it’s half of where it usually is. This premier tech company is not commanding the valuation it should or usually does. This one is worth a very close look.

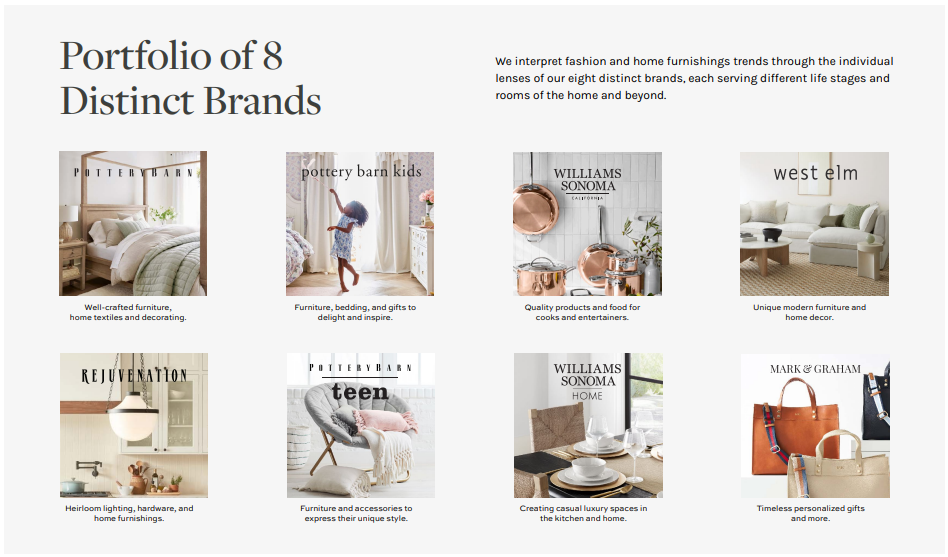

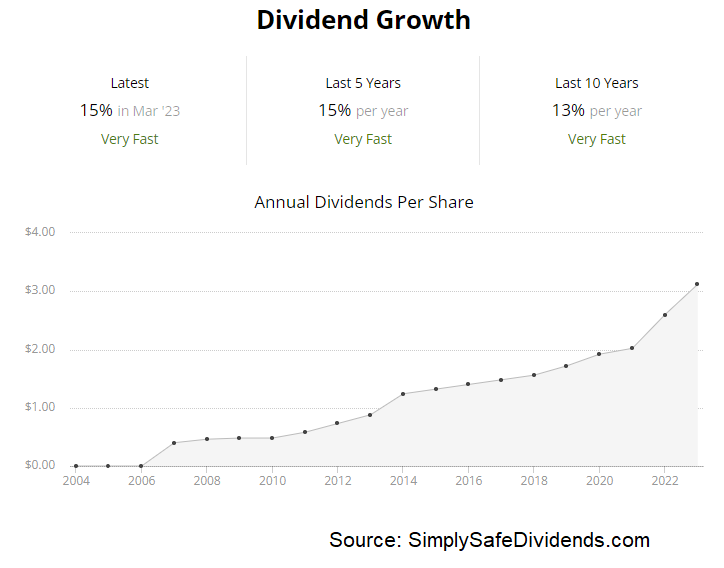

The sixth dividend increase I want to highlight is the one that came from Williams-Sonoma (WSM).

Williams-Sonoma just increased its dividend by 15%. Bam. Williams-Sonoma coming through yet again. This is one of the best niche retailers in all of America. All it does is sell more products, make more money, buy back shares, and increase its dividend. Love it.

This is the 18th consecutive year in which the home furnishings retailer has increased its dividend.

This is the 18th consecutive year in which the home furnishings retailer has increased its dividend.

The 10-year DGR is 13.2%, so we can see that consistent double-digit dividend growth at play here once again. And the stock also offers a pretty compelling yield of 3%. Boy, if every stock I ever bought gave me a 3% yield and a double-digit dividend growth rate, I’d be totally delighted. If that’s not good enough already, you also get a super low payout ratio of 22.1%. It’s practically “nirvana” here for long-term dividend growth investors.

But wait. There’s more. How about an attractive valuation?

But wait. There’s more. How about an attractive valuation?

We analyzed and valued this terrific business back in early October, estimating fair value for Williams-Sonoma at almost $178/share. The stock is currently priced at about $121. Could the analysis and valuation be off a bit? Absolutely. Is it likely that it’s completely wrong from start to finish? The odds of that are low.

That said, there’s a huge margin of safety here between price and estimated fair value. Williams-Sonoma announced a $1 billion buyback program along with that 15% dividend increase. That’s 12.5% of the company! The company is buying back its own stock hand over fist while the P/E ratio is below 8. I’d be inclined to join management on this one.

— Jason Fieber

The company manufacturing Nvidia's AI servers trades under a secret name. AI revenue: $30B this year. Stock price: $8. Click for the hidden identity →

Source: Dividends & Income