Wow. Been a wild time, hasn’t it?

A few idiosyncratic bank failures have created ripples across the market. It’s been about as volatile as it gets. But this volatility is a gift, especially for younger investors still accumulating assets.

Price and yield are inversely correlated. All else equal, lower prices result in higher yields.

This means more dividend income on the same invested dollar, creating a faster path to financial independence.

I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

All that said, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this piece is all about.

Today, I want to tell you my top 5 dividend growth stocks for April 2023.

Ready? Let’s dig in.

My first dividend growth stock for April 2023 is American Tower (AMT).

American Tower is a real estate investment trust that owns, operates, and develops broadcast communications infrastructure.

Real estate isn’t limited to apartments or shopping centers. No. Real estate can actually delve into infrastructure. And that’s precisely what leads you to the likes of American Tower, which is a premier infrastructure REIT that owns and operates – you guessed it – towers. These towers have various broadcast equipment installed onto them, and that equipment is necessary for a variety of technologies to work.

Mobile data would be an example. Without these towers, smartphones are practically unusable. And with the rise of self-driving cars, towers will become even more critical. This is why you see double-digit top-line and bottom-line growth over the last decade for American Tower – a 13.6% CAGR for revenue, and an 11.9% CAGR for AFFO/share.

What else has been growing at a double-digit rate? The dividend.

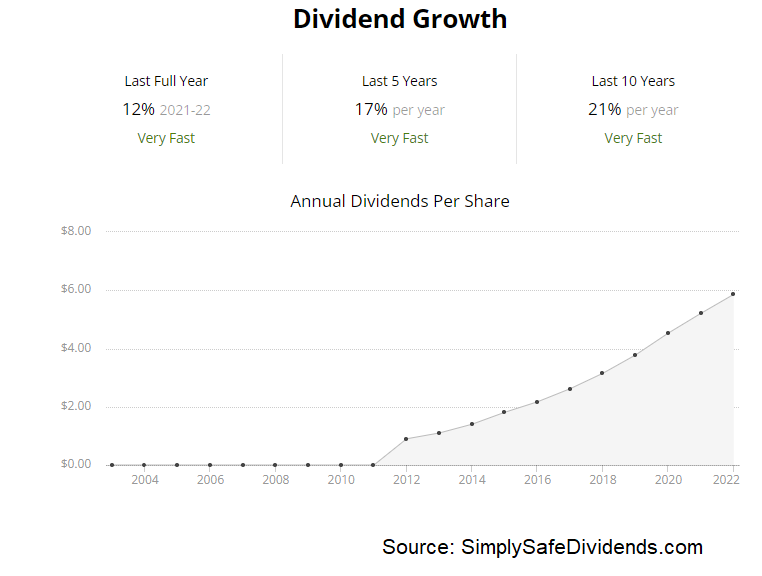

Yep. American Tower, which has increased its dividend for 13 consecutive years, sports a 10-year DGR of 20.3%. That is unusually high for a REIT, as most REITs are slower-growth income vehicles. Well, American Tower has been more of a true compounder, which is rare among REITs.

Yep. American Tower, which has increased its dividend for 13 consecutive years, sports a 10-year DGR of 20.3%. That is unusually high for a REIT, as most REITs are slower-growth income vehicles. Well, American Tower has been more of a true compounder, which is rare among REITs.

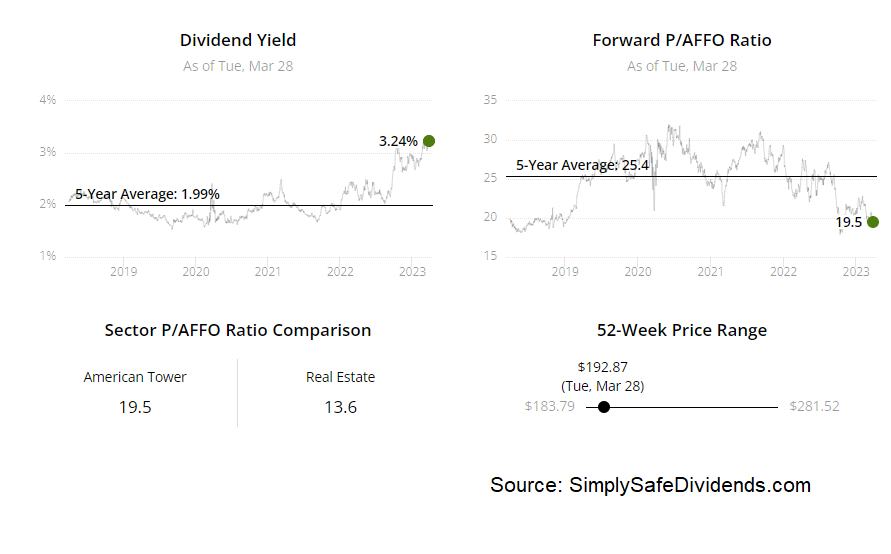

On the other hand, it doesn’t offer the kind of high yield that is typical across REITdom. The stock’s yield is just 3.1%. Respectable for sure. Just not the 5%+ yield that you might get elsewhere. However, it is 120 basis points higher than its own five-year average, speaking on the price-yield relationship I touched on earlier. The payout ratio is 64.9%, based on midpoint guidance for FY 2023 AFFO/share, which indicates a healthy dividend poised for more growth ahead.

This is a stock that has often looked expensive. But it doesn’t right now.

The forward price-to-adjusted-funds-from-operations ratio is right about 20. That’s somewhat analogous to a P/E ratio on a normal stock. For a business that has been able to grow the top line, the bottom line, and the dividend at a double-digit rate? I don’t think that’s an unreasonable multiple at all.

The forward price-to-adjusted-funds-from-operations ratio is right about 20. That’s somewhat analogous to a P/E ratio on a normal stock. For a business that has been able to grow the top line, the bottom line, and the dividend at a double-digit rate? I don’t think that’s an unreasonable multiple at all.

We recently analyzed and valued American Tower, estimating fair value for the business at just over $224/share. The stock is currently priced at around $192. Big gap between price and potential value here. Consider jumping on this great infrastructure REIT after the 30% decline from its 52-week high.

My second dividend growth stock for April 2023 is Lowe’s Companies (LOW).

Lowe’s is a large home improvement retailer based in the United States.

What can we say? Americans love their houses. Homeownership, and the sense of independence as you forge your own path, is part and parcel of the American Dream. Well, that plays right into the hands of major home improvement retailers like Lowe’s, as the likes of Lowe’s caters to homeownership. Houses are physical structures that are decaying.

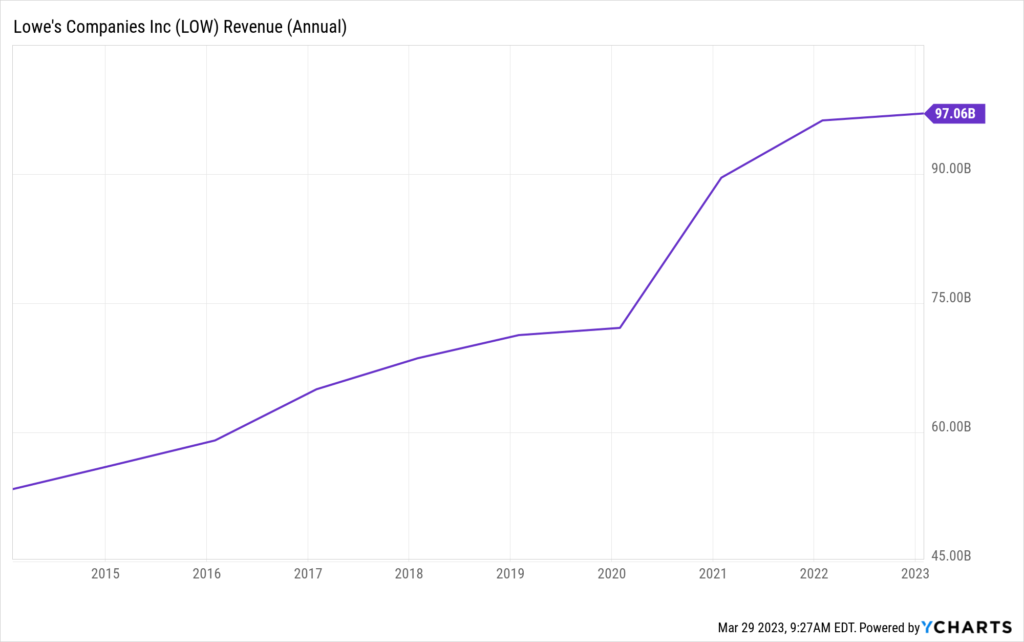

As such, houses need constant upkeep and repairs. And that’s not even to speak of modifications, upgrades, personalization, etc. All of that explains why Lowe’s has been putting up amazing numbers. Lowe’s has compounded its revenue at a 6.9% annualized rate and its EPS at an 18.9% annualized rate over the last decade.

This amazingness also translates over to the dividend.

This amazingness also translates over to the dividend.

Lowe’s has increased its dividend for 60 consecutive years. Yes. 60 straight years of ever-higher dividends. It’s a Dividend Aristocrat, a Dividend King, and pretty much every other title you could possibly confer. The 10-year DGR is 20%.

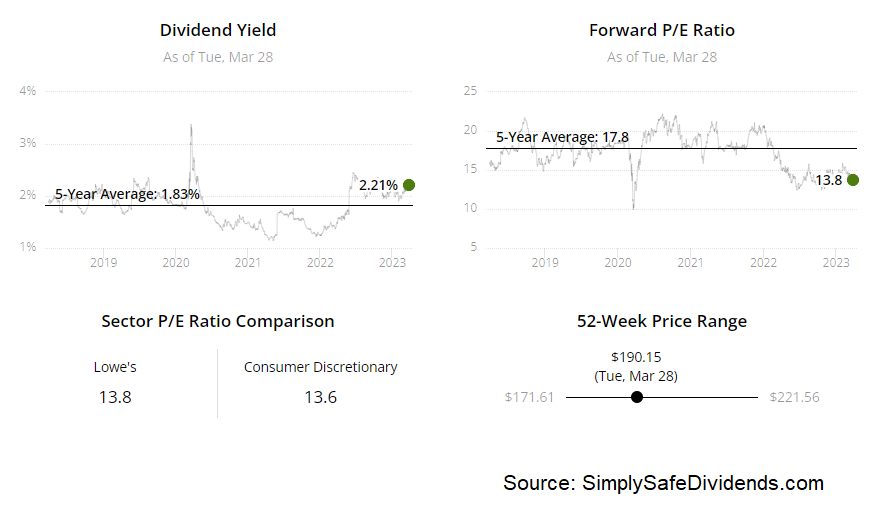

That would be impressive for some new upstart, fresh into a dividend hiking cycle. But for a company that had already been increasing dividends for 50 years in a row at the start of the prior decade? It’s almost unbelievable. The yield of 2.2% is pretty decent, especially when paired with a double-digit dividend growth rate. And the payout ratio remains a low 30.4%, based on FY 2023 EPS guidance at the midpoint, even after all of those dividend raises.

This is a very high-quality Dividend Aristocrat. And it looks modestly undervalued right now.

Is it back-up-the-truck cheap? No. But this is one of the best businesses in America. And if you can invest in terrific businesses like this at even just modest discounts, you’re going to have a very fruitful experience as a long-term dividend growth investor.

To see this stock with a P/E ratio below 20 kind of surprises me. It’s sitting at 18.6 right now. Its five-year average is 23.1. So you can see that disconnect. We’ll have a full analysis and valuation video coming out soon on Lowe’s, which will show why this great retailer could be worth $226.60/share.

To see this stock with a P/E ratio below 20 kind of surprises me. It’s sitting at 18.6 right now. Its five-year average is 23.1. So you can see that disconnect. We’ll have a full analysis and valuation video coming out soon on Lowe’s, which will show why this great retailer could be worth $226.60/share.

The stock is currently priced at about $189. I don’t own a house, so shopping at Lowe’s has never really been a thing for me personally, but I am very keen to go shopping for the stock right now. Consider stocking up on this stock before the sale ends.

My third dividend growth stock for April 2023 is Masco (MAS).

Masco is a manufacturer of products for the home improvement and new home construction markets.

The investment thesis around Masco is similar to that of Lowe’s, except you’re looking at a manufacturer instead of a retailer. But it really does come down to the relationship between Americans and homeownership.

Americans want to own houses. And there will almost certainly be more Americans alive 10 years from now, which means more houses. Well, all of that circles right back around to Masco, which manufactures a variety of components necessary to the construction of homes, such as faucets, toilets, plumbing valves, shower enclosures, and paints. This business might fly under the radar, but the growth isn’t bad at all. We’re talking a 1.3% CAGR for revenue over the last decade, while EPS has a CAGR of 9.2% over that period.

Even better is the dividend growth.

Masco has grown its dividend for 10 consecutive years, and the five-year DGR is 22.6%. That is really strong. Plus, the stock yields 2.4%, which is 110 basis points higher than its own five-year average. That’s a noticeable spread. Also, the payout ratio is 29.9%, based on midpoint adjusted EPS guidance for this fiscal year. That indicates a very healthy dividend. And so even if there are short-term bumps with the US housing market, there’s a nice cushion in place here.

Masco has grown its dividend for 10 consecutive years, and the five-year DGR is 22.6%. That is really strong. Plus, the stock yields 2.4%, which is 110 basis points higher than its own five-year average. That’s a noticeable spread. Also, the payout ratio is 29.9%, based on midpoint adjusted EPS guidance for this fiscal year. That indicates a very healthy dividend. And so even if there are short-term bumps with the US housing market, there’s a nice cushion in place here.

This stock is priced the same as it was before the pandemic hit, and I think we’ve got some serious undervaluation present.

This was a $48 stock in early 2020. It’s currently a $48 stock. The stock has gone nowhere, yet Masco is now a bigger business paying out a bigger dividend than it was three years ago. And so what’s happened here is, the valuation has become compressed.

The P/E ratio of 13.1 is well off of its own five-year average of 20.8. We put together a video not long ago that analyzed and valued Masco, estimating intrinsic value for the business at $62.83/share. That’s a pretty sizable margin of safety. Masco is worth a close look here.

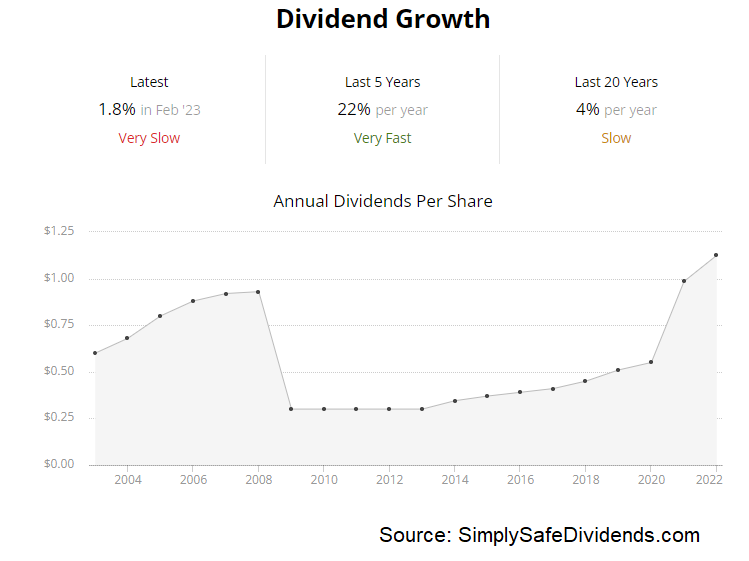

My fourth dividend growth stock for April 2023 is Pfizer (PFE).

Pfizer is a multinational pharmaceutical and biotechnology corporation. Pfizer is super interesting. I’d bet that a lot of people who don’t follow the market closely would assume that this stock must have skyrocketed as a result of the pandemic and sales of its Comirnaty vaccine and Paxlovid oral medication.

While the stock did spend some time in the sun, it’s come crashing back down. The stock was priced at about $40 in early 2020, before the pandemic hit. It’s currently priced at $40. So it’s round-tripped, effectively pricing all of the supposed pandemic-related financial benefits at $0. Digging into the business, though, does show steady growth – a 7.7% CAGR for revenue and 6.2% CAGR for EPS over the last decade.

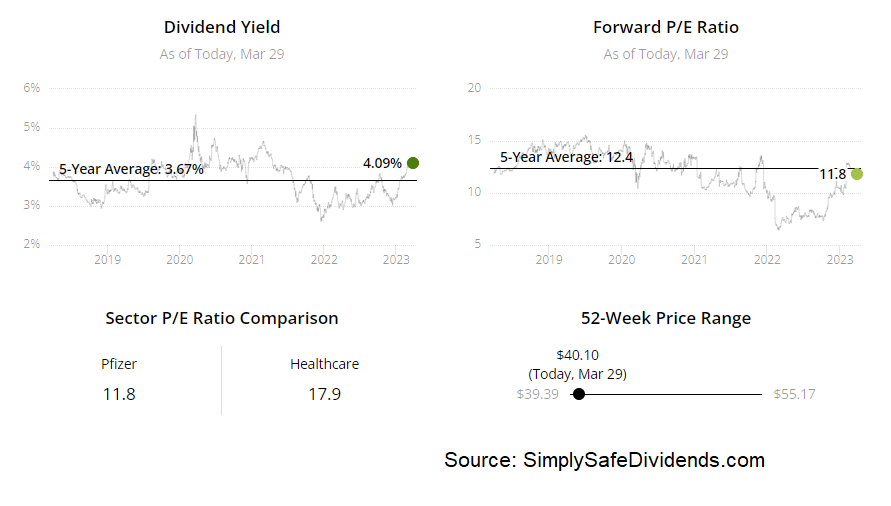

Also steady is the dividend growth. The dividend has been raised for 13 consecutive years. The 10-year DGR of 6.2% lines up perfectly with EPS growth over the same time frame, showing excellent prudence from management. And stock’s yield of 4.1% is pretty juicy.

That’s 50 basis points higher than its own five-year average. Nothing wrong at all with a 4%+ yield and a mid-single-digit dividend growth rate. And with a payout ratio of 49%, based on adjusted EPS guidance at the midpoint for FY 2023, we have great balance here between the shareholder returns and capital retainment. Again, just good prudence here on the part of management.

Good growth, good yield, good value.

Pfizer doesn’t necessarily “wow” me in any one department. Instead, it’s just a solid combination of everything across the board. Speaking on the valuation, every basic valuation metric I look at is well below its respective recent historical average.

Now, the P/E ratio of 7.4 is silly low, but that number captures a lot of temporary sales and profits. The forward P/E ratio of 12, using midpoint guidance for FY 2023 adjusted EPS, is a more fair assessment of the earnings multiple.

Now, the P/E ratio of 7.4 is silly low, but that number captures a lot of temporary sales and profits. The forward P/E ratio of 12, using midpoint guidance for FY 2023 adjusted EPS, is a more fair assessment of the earnings multiple.

But that’s still quite low. We’re in the midst of editing a full analysis and valuation video on Pfizer, and that video will show why the intrinsic value of the business is estimated at slightly under $48/share. Pfizer offers something to like for just about every long-term dividend growth investor. Make sure it’s on your radar.

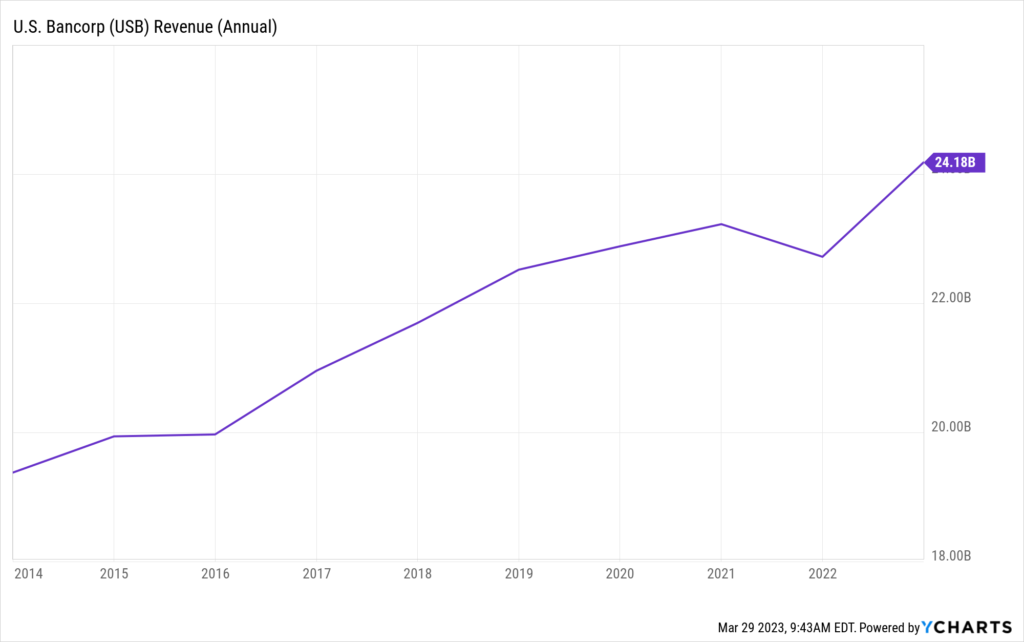

My fifth dividend growth stock for April 2023 is U.S. Bancorp (USB).

U.S. Bancorp is one of the largest banks in the United States. The US runs on capitalism. And banks are the lubrication for the capitalistic machine. Banks have been around for thousands of years. Why is the business model seemingly immortal?

Well, it’s all about commerce and the flow of money, goods, and services. Without the financial framework that banking allows for, our way of life ceases to exist in its current form. Banks make money from money. Better yet, banks make money from other people’s money, using low-cost, low-risk deposits as a mechanism to fund for-profit ventures. This is where the “float” comes from. It’s also where pretty decent growth comes from – a 2.4% CAGR for revenue and 4.5% CAGR for EPS over the last decade.

The dividend growth has been better than decent. Now, the last decade has been super challenging for banks. Low rates, high regulation, a sputtering economy, and even a global pandemic. Not a great recipe for bank outperformance.

The dividend growth has been better than decent. Now, the last decade has been super challenging for banks. Low rates, high regulation, a sputtering economy, and even a global pandemic. Not a great recipe for bank outperformance.

Despite all of this, the bank has increased its dividend for 12 consecutive years, with a 10-year DGR of 10.1%. A double-digit dividend growth rate is always nice to see, but it’s especially nice in this case. That’s because the stock also yields 5.5%. How often are you able to pair a yield that high with a dividend growth rate this high? And with a payout ratio of 52%, I don’t see any danger around the dividend.

This stock looks cheeeeeeap. Yes, we’ve had a few bank failures. But those idiosyncratic issues around things like mismanagement, exposure to crypto, and narrow depositor bases with high uninsured deposits all have nothing to do with the likes of U.S. Bancorp.

If we have a scenario in which U.S. Bancorp is actually threatened, we’ve got way bigger issues than the stock. This stock is down 40% and now sports a P/E ratio in the single digits. We’re putting together a full analysis and valuation video on the large bank, and you’ll see in this video why the estimate for fair value shakes out to a bit over $55/share.

If we have a scenario in which U.S. Bancorp is actually threatened, we’ve got way bigger issues than the stock. This stock is down 40% and now sports a P/E ratio in the single digits. We’re putting together a full analysis and valuation video on the large bank, and you’ll see in this video why the estimate for fair value shakes out to a bit over $55/share.

The stock is currently sitting around $35. If you like being greedy while others are fearful, there’s a lot of fear around banks. Here’s your shot.

— Jason Fieber

The old way of investing in tech giants is over. A NEW strategy unlocks 146X more income on the SAME underlying stocks (like Meta, Apple, and Amazon) -- WITHOUT options trading. Click here to uncover the NEW MAG-7 alternative.

Source: Dividends & Income