Successful long-term investing can be paradoxical in some ways.

When great investment opportunities are few and far between, that can feel like a fantastic time to invest.

After all, this is when the economy is humming along, everyone is optimistic, and liquidity is flowing.

Conversely, when the best investing opportunities come, that can feel like the worst time to invest.

This is because the economy is stumbling, everyone is pessimistic, and liquidity stops flowing.

Yet the latter scenario is precisely when you want to be aggressive.

Angel investor Jason Calacanis has said: “Fortunes are built during the down market and collected in the up market.”

Cranking up the aggressiveness during times of pessimism has served me well.

It’s helped me to build my FIRE Fund over the years.

It’s helped me to build my FIRE Fund over the years.

This is my real-money stock portfolio.

It produces enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been living off of dividends for a number of years now.

In fact, I retired in my early 30s.

My Early Retirement Blueprint shares how I was able to do that.

A pillar of the Blueprint is the investment strategy that I’ve followed – a strategy that forms the backbone of the Fund.

It’s dividend growth investing.

This strategy involves buying and holding shares in world-class businesses that pay reliable, rising dividends to their shareholders.

Perusing the Dividend Champions, Contenders, and Challengers list will show you what I mean.

This list contains invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

How does a business safely pay a dividend, and reliably increase that dividend every year?

By producing ever-more profit.

By producing ever-more profit.

It’s really that simple.

So why is the best time to invest when it feels like it’s the worst?

Because valuations will almost certainly have fallen to the point that terrific businesses are available for deep discounts.

While price is what you pay, it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Taking advantage of the best times to invest, even when it feels like it’s the worst, by buying high-quality dividend growth stocks when they’re undervalued can set you up for an impressive fortune when pessimism has turned into optimism.

Of course, this does mean that one already understands how to go about valuing a business.

But this isn’t all that difficult.

Fellow contributor Dave Van Knapp’s Lesson 11: Valuation, which is part of a comprehensive series of “lessons” on dividend growth investing, provides a simple-to-follow valuation template.

This template can be applied in a way that helps you to estimate the fair value of just about any dividend growth stock you’ll run across.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

U.S. Bancorp (USB)

U.S. Bancorp (USB)

U.S. Bancorp (USB) is a bank holding company that offers a diversified mix of financial services, including traditional retail banking, wealth management, commercial banking, and payment services.

Founded in 1863, U.S. Bancorp is now a $50 billion (by market cap) banking behemoth that employs 76,000 people.

Operating as the fifth-largest American bank by deposits, U.S. Bancorp has over 2,000 branches spread out across 26 different states (primarily in the Midwest and West).

The bank ranks first in deposit share in four states, while it has a top-five position in 17 states.

The company reports results across five business segments: Consumer & Business Banking, 35% of FY 2022 revenue; Payment Services, 26%; Corporate & Commercial Banking, 18%; Wealth Management & Investment Services, 17%; and Treasury and Corporate Support, 4%.

There are so many reasons to love the banking business model.

When someone says they “make bank”, it means they’re making a lot of money.

The word “bank” has come to be strongly associated with “money”.

That’s because banks are literally in the business of money.

And if one wants to make money, money itself is a pretty good place to start.

But it’s not just money.

It’s other people’s money.

Banks take in deposits from depositors.

Deposits become a “float” – a low-cost and low-risk source of capital that allows a bank to fund loans and other ventures in order to earn a return.

It’s been said that you need money to make money.

Well, banks take that pretty seriously by gathering lots of money in order to make lots of money.

This is an idea that is timeless.

Banks have been around for thousands of years.

You can trace banking back to antiquity.

Why is the business model so enduring?

It comes down to commerce and the flow of money, goods, and services.

Without the financial framework that banking allows for, our way of life collapses and we go back to a bartering existence.

Here’s how Morningstar describes U.S. Bancorp: “U.S. Bancorp is the largest non-GSIB in the U.S. and has been one of the most profitable regional banks we cover. Few domestic competitors can match its operating efficiency and returns on equity over the past 15 years.”

Good stuff.

Because U.S. Bancorp runs such a powerful, necessary, and enduring business model, the company is positioned to continue increasing its revenue, profit, and dividend for many more years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

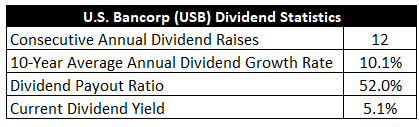

The company has increased its dividend for 12 consecutive years.

The 10-year dividend growth rate of 10.1% is quite strong.

What’s really notable here is the fact that you’re pairing that with the stock’s starting yield of 5.1%.

If you think that kind of yield is unusually high for a large, stable bank, you’re right.

This market-smashing yield is 180 basis points higher than its own five-year average.

This market-smashing yield is 180 basis points higher than its own five-year average.

And with the payout ratio sitting at 52%, this is not an unsafe dividend.

The yield is so high not because of specific dividend danger but because of a temporary panic across the general banking industry, which I’ll delve into later.

It’s very rare that a bank will offer a yield that’s competitive with high-yield instruments, such as REITs, but that’s the kind of opportunity we could have on our hands right now.

For dividend growth investors who like to be greedy when others are fearful, these dividend metrics are quite enticing.

Revenue and Earnings Growth

As enticing as these dividend metrics may be, we’re mostly looking backward here.

However, investors are always risking the capital of today for the rewards of tomorrow.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will later be of assistance when it comes time to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Fusing the proven past with a future forecast in this way should give us the capability to gauge where the business might be going from here.

U.S. Bancorp enlarged its revenue from $19.6 billion in FY 2013 to $24.3 billion in FY 2022.

That’s a compound annual growth rate of 2.4%.

So-so top-line growth here.

It’s been a very challenging decade for banks, with heightened regulation, low interest rates, and a floundering economy all conspiring to limit growth across the industry.

We then threw a global pandemic in there for good measure.

This is about as bad as it gets for banks.

In my view, even modest expansion in the business is comforting.

Meanwhile, earnings per share grew from $3.00 to $4.45 (adjusted) over this period, which is a CAGR of 4.5%.

I used adjusted EPS for FY 2022 in order to factor out unusual expenses related to the company’s recent acquisition of MUFG Union Bank (completed in December 2022).

I should note that regular share repurchases did help to drive excess bottom-line growth.

The outstanding share count is down by 19% over this period.

Again, not super inspiring growth.

Like I already pointed out, it’s been a tough decade, and recent events aren’t making things any better.

That said, it’s ultimately where a business is going, not where it’s been, that matters most to the investors of today.

Looking forward, CFRA believes that U.S. Bancorp will grow its EPS at a CAGR of 7% over the next three years.

This forecast hinges quite a bit on the company’s recent acquisition coinciding perfectly with a normalizing/improving post-pandemic environment.

Regarding the acquisition, CFRA states: “On December 1, 2022, [U.S. Bancorp] closed its acquisition of Union Bank and added one million consumer accounts, 190,000 business clients, 50,000 affluent households, and 280 new branches in California.”

The acquisition of MUFG Union Bank didn’t close until FY 2022 was almost over, so we haven’t really had a chance to see how much this can positively impact the combined enterprise.

But it does shape U.S. Bancorp in a positive way, and CFRA is enthusiastic about the tie-up: “We continue to be impressed with [U.S. Bancorp’s] digital transformation and are excited by its increased West Coast presence. Additionally, we expect improving bank efficiency over the next few years as [U.S. Bancorp] benefits from costs synergies stemming from the Union Bank acquisition.”

U.S. Bancorp is guiding for adjusted total revenue of $29 billion to $31 billion for FY 2023, which would represent a substantial move up from what was reported for FY 2022.

I think it’s important to take notice of two important points here.

First, it goes without saying that higher interest rates benefit U.S. Bancorp in terms of net interest margin.

Second, about half of the business has a steady fee-based framework.

I concur with CFRA’s overall enthusiasm.

With that positivity out of the way, let’s delve into some negativity.

Unless you’re living under a rock, you’ll know that bank stocks have been absolutely rocked over the last few weeks.

A few bank failures caused widespread panic among the investing community, with many believing that contagion and bank runs across the board would result in a cascading domino effect across almost all banking institutions.

However, it’s important to point out what actually happened here.

A few banks failed, yes.

But these failures can be largely pinned down to idiosyncratic issues, including (but not limited to): concentrated depositors, cryptocurrency exposure, poor risk management, and a large percentage of uninsured deposits.

That last point is especially germane.

One of the banks that failed, Silicon Valley Bank, had an extremely high ratio of uninsured deposits to total deposits – approximately 90%.

This resulted in a fear of potential losses among depositors, which then led to a bank run.

U.S. Bancorp’s ratio is closer to 50%.

Furthermore, Silicon Valley Bank had a depositor base that was very concentrated around the venture capital community, and this concentrated depositor base exacerbated the velocity and intensity of the bank run.

U.S. Bancorp has a far more granular and “regular” depositor base.

There are many reasons why U.S. Bancorp has nothing to do with what happened to Silicon Valley Bank.

In addition, it’s quite possible that some banks’ pain will end up being U.S. Bancorp’s gain – to the extent that a deposit flight has occurred, which appears to be relatively muted and mostly overblown, this capital has seemingly flowed upward with a bank’s size, benefiting larger financial institutions like U.S. Bancorp.

Overall, I think U.S. Bancorp is one of America’s best banks.

It’s definitely one of the biggest.

On the other hand, it’s quite possible, even likely, that banks across the board will see higher fees and more regulation in the aftermath of recent bank failures, which slightly reduces the long-term profitability outlook.

Getting back to the forecast, a 7% CAGR in EPS would allow for a similar rate of dividend growth.

While dividend raises may be conservative in the near term, if only to account for the uncertainty across the industry, you’re already starting off with a 5%+ yield.

I don’t think you need high-single-digit dividend growth to make sense of an investment here.

But the fact that this kind of dividend growth could transpire on top of a 5%+ yield makes this a particularly compelling long-term investment idea right now.

Financial Position

Moving over to the balance sheet, U.S. Bancorp has a great financial position.

Total assets of $675 billion line up well against $624 billion in total liabilities.

Their senior unsecured debt has the following credit ratings: A2, Moody’s; A+, S&P; A+, Fitch.

These ratings are well into investment-grade territory.

Profitability for the bank is outstanding.

Over the last five years, the firm has averaged annual net margin of 27.7% and annual return on equity of 13.9%. Net interest margin came in at 2.7% last year.

The banking industry is experiencing turmoil, but U.S. Bancorp is running a steady, stodgy financial institution.

And with economies of scale, “sticky” deposits, switching costs, established relationships, and an entrenched float, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Competition, regulation, and litigation are omnipresent risks in every industry.

I see increased regulation stemming from the fallout of recent bank failures.

However, bank failures, and possible consolidation across the industry, eliminates some competition.

As we’ve been reminded of recently, any bank is vulnerable to a sudden bank run.

Banks are highly exposed to economic cycles; a recession could hurt the bank through reduced deposits and loan demand on the income statement, as well as higher credit losses on the balance sheet.

Interest rates have been persistently low over the last decade, which has put a lid on what banks can do, but rates are finally on the rise.

The acquisition of MUFG Union Bank adds near-term questions around execution and capital use.

I’d argue that these are pretty customary risks for a bank, but the valuation is currently anything but customary.

With the stock down 40% from its recent high, the valuation looks as attractive as I’ve ever seen it…

Stock Price Valuation

The P/E ratio is 7.8.

That’s using adjusted EPS, to factor out the one-time acquisition impact.

This is absurdly low for one of the biggest and best financial institutions in the United States.

Now, to be fair, banks never really command very high multiples.

But the five-year average P/E ratio for this stock is 12.4.

We’re not even close to that.

Another way to look at it is the P/B ratio, which is 1.2.

Banks typically command P/B ratios that are between 1 and 2, depending on the growth and quality of the bank.

This bank’s five-year average P/B ratio is 1.7, which expresses its quality.

Again, we’re not even close to that level right now.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 6.5%.

That dividend growth rate is actually on the low end of what I ordinarily allow for when valuing a bank.

It’s lower than the 7% mark I used the last time I looked at U.S. Bancorp, and I’ve dialed expectations back a bit in order to account for the general turmoil and uncertainty across banking.

This mark looks awfully conservative when you weigh it up against the demonstrated dividend growth over the last decade.

And I’m also a bit below where CFRA sees EPS growth coming in at over the next few years.

But I really would rather err on the side of caution here, especially because of so many moving parts that are impossible to fully appreciate.

In the fullness of time, we’ll see how this all plays out.

But I think U.S. Bancorp could easily meet, or even exceed, this kind of dividend growth target.

The DDM analysis gives me a fair value of $58.42.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think I was being very, very fair with my analysis, yet the steep drop in the pricing has caused the stock appear to be quite cheap anyway.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates USB as a 5-star stock, with a fair value estimate of $58.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates USB as a 3-star “HOLD”, with a 12-month target price of $50.00.

I came out within pennies of where Morningstar is at. Averaging the three numbers out gives us a final valuation of $55.47, which would indicate the stock is possibly 37% undervalued.

Bottom line: U.S. Bancorp (USB) is one of the biggest and best banks in the United States. While there’s undoubtedly a lot of turmoil occurring around it, the makeup of the institution, including a strong focus on fee-based offerings, creates a rock in the storm. With a market-smashing yield, a balanced payout ratio, a double-digit long-term dividend growth rate, more than 10 consecutive years of dividend increases, and the potential that shares are 37% undervalued, this looks like a textbook opportunity for long-term dividend growth investors to be greedy while others are fearful.

Bottom line: U.S. Bancorp (USB) is one of the biggest and best banks in the United States. While there’s undoubtedly a lot of turmoil occurring around it, the makeup of the institution, including a strong focus on fee-based offerings, creates a rock in the storm. With a market-smashing yield, a balanced payout ratio, a double-digit long-term dividend growth rate, more than 10 consecutive years of dividend increases, and the potential that shares are 37% undervalued, this looks like a textbook opportunity for long-term dividend growth investors to be greedy while others are fearful.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is USB’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 55. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, USB’s dividend appears Borderline Safe with a moderate risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income