I’ve been buying high-quality dividend growth stocks for more than a decade now. These are stocks that pay reliable, rising dividends. Those reliable, rising dividends are, of course, funded by reliable, rising profits.

High-quality dividend growth stocks represent equity in world-class businesses. But here’s the thing.

Some dividend growth stocks are more dividend. Other dividend growth stocks are more growth.

So you can go after dividend growth stocks… or dividend growth stocks.

The emphasis matters a lot. After more than a decade of doing this, I’ve learned an important lesson.

If you want outstanding long-term performance and total return, you will almost certainly want to lean more toward growth than dividend.

Better yet, dividend growth stocks tend to offer the safest dividends, most unlikely to be cut. This is a bitter pill to swallow for yield chasers. But that’s reality.

If you have the time to let the compounding process play out, dividend growth stocks that offer high rates of dividend growth can make you very wealthy and produce gobs of more reliable dividend income over time.

Today, I want to tell you about five dividend growth stocks that have grown dividends at 20%+ per year over the last decade.

Ready? Let’s dig in.

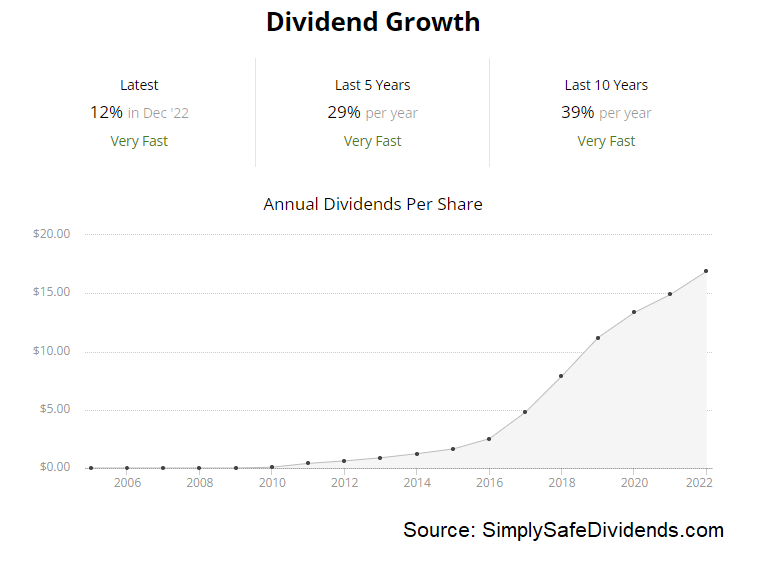

The first dividend growth stock I want to bring to your attention is Broadcom (AVGO).

Broadcom is a leading infrastructure software and digital semiconductor devices company. Nobody should be surprised to see a tech company up first. Tech is changing and shaping the world. It’s where so much of the economic growth is. And so if you want to profit from the future and participate in growth, you really have to be in tech to some degree.

Broadcom’s current technology offerings can be found in the likes of smartphones, servers, set-top boxes, storage systems, and controllers. The company is exposed to exciting, high-growth areas like data centers, broadband, wireless connectivity, and automation. Because the business is growing at a high rate, the dividend has been growing at a high rate.

Broadcom’s 10-year dividend growth rate is 39.4%. Wow. That is how you compound wealth and passive income. Broadcom’s dividend is 20 times bigger than it was a decade ago. Those who focus on yield only are missing the total return forest for the yield trees.

Broadcom’s 10-year dividend growth rate is 39.4%. Wow. That is how you compound wealth and passive income. Broadcom’s dividend is 20 times bigger than it was a decade ago. Those who focus on yield only are missing the total return forest for the yield trees.

That said, Broadcom is no slouch when it comes to yield. The stock does offer a 2.9% yield. I think that’s more than acceptable when the dividend is growing at such a high rate. Broadcom has increased its dividend for 13 consecutive years, and I foresee much more to come.

With a 62% payout ratio, there’s room for it. However, there has been a slowing in the dividend growth. The last dividend raise was a bit over 12%. But if every stock I bought had a 3% yield and a 12% dividend growth rate, I’d be a very happy dividend growth investor.

Broadcom is, in many ways, a dividend growth investor’s dream. It basically offers it all. Yield, growth, quality. Certainly performance – the stock is up 1,700% over the last 10 years. Plus, you even get a sprinkling of value.

The P/E ratio of 21.2 is surprisingly low for a business that has been able to sustain the kind of impressive growth that Broadcom has. There are a number of tech firms out there with less growth and higher multiples. We analyzed and valued the business late last year, estimating fair value for Broadcom at nearly $600/share.

The P/E ratio of 21.2 is surprisingly low for a business that has been able to sustain the kind of impressive growth that Broadcom has. There are a number of tech firms out there with less growth and higher multiples. We analyzed and valued the business late last year, estimating fair value for Broadcom at nearly $600/share.

But that was before the recent 12.2% dividend raise, which would improve the value of the business on a dividend discount model analysis. The stock was priced at about $512 back then. It’s now sitting in the $630 range. Overall, I think we’ve got a pretty fair deal here for one of the “growthiest” dividend growth stocks out there.

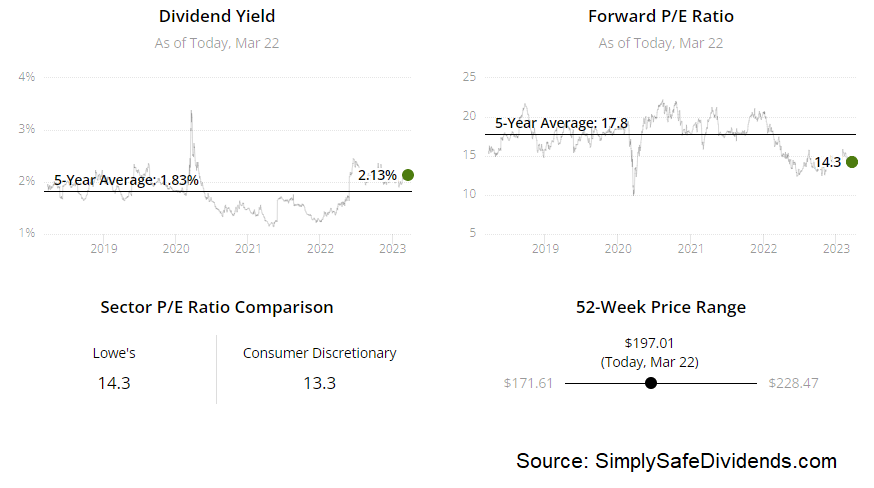

The second dividend growth stock I want to highlight is Lowe’s Companies (LOW).

Lowe’s is an American home improvement retailer. This is a titan in the American home improvement space, which is a great space to be in. Almost every American I’ve ever met owns or wants to own a house. And what do houses do?

Well, they decay over time. They’re physical structures that age. That’s just how it is. Because of this, houses need constant upkeep and maintenance in order to simply not fall apart. Plus, most people want a house to be a home, which requires personalization and modifications.

All of that plays right into the hands of Lowe’s, which offers thousands of products to homeowners. It’s a recipe that’s stood the test of time, allowing Lowe’s to grow its dividend at a very impressive rate for an impressively long period of time.

Lowe’s 10-year dividend growth rate is 20%. What’s crazy here is that there’s been an acceleration in dividend growth – the most recent dividend raise came in at a jaw-dropping 32.1%. Now, that kind of dividend growth can’t persist indefinitely.

But Lowe’s has shown a rare staying power when it comes to high dividend growth. The company has increased its dividend for 60 consecutive years, qualifying itself for its Dividend Aristocrat status more than twice over.

So, 10 years ago, the retailer had already been increasing the dividend for 50 straight years, and yet the dividend still compounded at 20% annually from there. The stock even offers a respectable 2.1% yield. And the payout ratio is only 30.4%, based on FY 2023 EPS guidance at the midpoint, even after huge dividend raises. This appears to be an extremely safe dividend.

I think this high-quality Dividend Aristocrat is undervalued. Not hugely so, but it might be the best deal out of the five names I’m covering today. We recently put together a full analysis and valuation video on Lowe’s. That video has to be edited, but it should be live soon. In the analysis video, the estimate for the retailer’s intrinsic value came out to $226.60 per share.

As I write this, the stock is priced at $197. This is one of the best businesses in all of America. It’s really hard to go wrong by getting a good deal on a great business. And I think that’s just what we’ve got here with Lowe’s. This stock is up by more than 400% over the last 10 years. From the current starting point, we’ve got a good shot at a repeat performance over the next decade.

As I write this, the stock is priced at $197. This is one of the best businesses in all of America. It’s really hard to go wrong by getting a good deal on a great business. And I think that’s just what we’ve got here with Lowe’s. This stock is up by more than 400% over the last 10 years. From the current starting point, we’ve got a good shot at a repeat performance over the next decade.

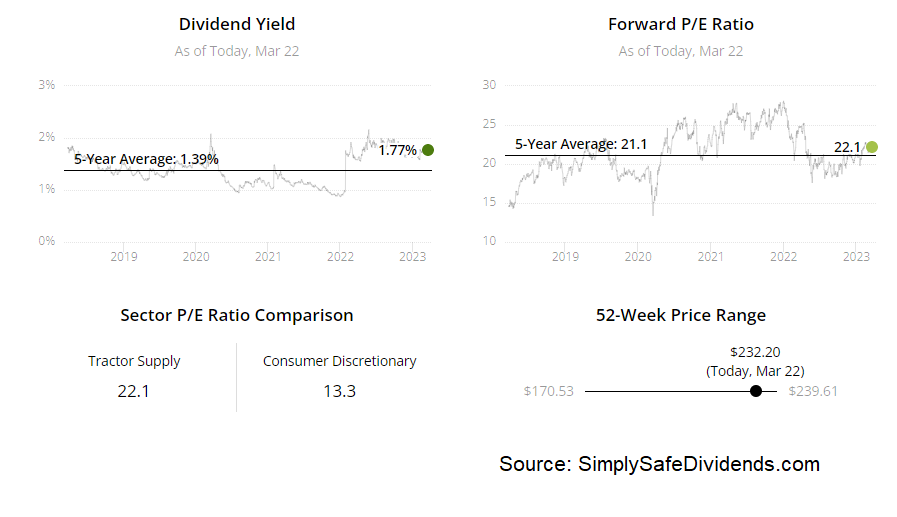

The third dividend growth stock we have to cover is Tractor Supply (TSCO).

Tractor Supply is an American retail chain that sells a variety of farm-oriented products. General retailing is very competitive. And it can be difficult to stand out when the stores are largely fungible. That’s why niche retailers often have an advantage.

Well, Tractor Supply is definitely a niche retailer, catering to a rural clientele in a way that nobody else really does. And what’s so great about this niche, in particular, is the way in which these products can’t easily be trafficked online.

We’re talking about a lot of heavy products, like huge bags of feed or, well, tractors. This is part of why Tractor Supply has been so prolific as a physical, B&M retailer in an e-commerce world, and it’s also part of why the dividend has grown at such a prolific rate.

We’re talking about a lot of heavy products, like huge bags of feed or, well, tractors. This is part of why Tractor Supply has been so prolific as a physical, B&M retailer in an e-commerce world, and it’s also part of why the dividend has grown at such a prolific rate.

Tractor Supply’s 10-year dividend growth rate is 26.2%. Sheesh. Using the Rule of 72, compounding your money at this kind of rate doubles it every 2.7 years. You’re looking at doubling your dividend income in less than three years, so focusing on the stock’s current yield of 1.8% kind of misses the point. The payout ratio is 42.4%, so the company’s 14 consecutive years of dividend increases is a track record that looks set to continue for many more years into the future.

This stock isn’t cheap, nor should it be. But I don’t think the valuation is outrageous. The P/E ratio of 23.9 is pretty close to its own five-year average of 23.2. Now, if this were a slow-growth business, I wouldn’t want to pay anything close to 24 times earnings.

This stock isn’t cheap, nor should it be. But I don’t think the valuation is outrageous. The P/E ratio of 23.9 is pretty close to its own five-year average of 23.2. Now, if this were a slow-growth business, I wouldn’t want to pay anything close to 24 times earnings.

But Tractor Supply’s most recent quarter dazzled, showing 25.9% YOY EPS growth. And so we’re talking about a PEG ratio of less than 1 here on a niche retailer that’s shown an ability to consistently grow revenue, EPS, and the dividend at very, very high rates. The stock is up about 350% over the last decade. I really don’t see why the next decade couldn’t provide something similar for those buying in now.

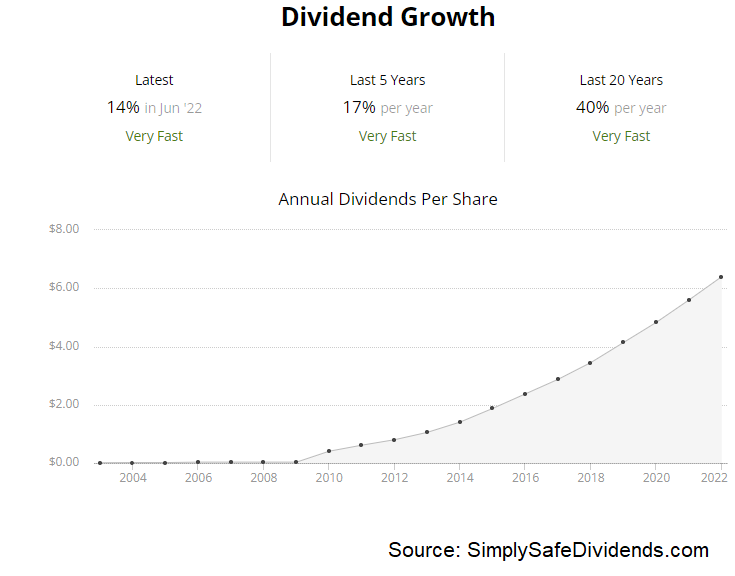

The fourth dividend growth stock I have to bring up is UnitedHealth Group (UNH).

UnitedHealth Group is a managed healthcare and insurance company. I’m a big fan of the insurance business model. If you underwrite properly, you can make a decent profit. But the real kicker is the “float” – the capital that builds up during the time delay between collecting premiums and paying out on claims.

The float can be a major profit driver for an insurance business, because it can be invested and earn a low-cost, low-risk return. What UnitedHealth Group does is take the basic insurance business model and supercharges it by operating in the healthcare space. That makes the business model practically invincible, as Americans basically can’t function without health insurance. This is why UnitedHealth Group has been a lock for huge growth and dividend raises.

UnitedHealth Group’s 10-year dividend growth rate is 23.1%. Outstanding. You wouldn’t expect that kind of dividend growth from a supposedly-sleepy insurance business, but, as I just alluded to, UnitedHealth Group is anything but sleepy. It’s a supercharged growth machine.

UnitedHealth Group’s 10-year dividend growth rate is 23.1%. Outstanding. You wouldn’t expect that kind of dividend growth from a supposedly-sleepy insurance business, but, as I just alluded to, UnitedHealth Group is anything but sleepy. It’s a supercharged growth machine.

Now, you do give up some yield here. The stock’s yield is 1.4%. However, I’m not sure why anyone would expect a high yield with this kind of growth rate. To be fair, the most recent dividend raise was 13.8%. And that might be a more realistic assumption of future dividend growth. But the company has increased its dividend for 13 consecutive years now, and I’m highly confident that will persist for many, many more years. Bolstering that confidence is the payout ratio of only 31.2%.

All metrics are indicating a fair deal for this stock. As Warren Buffett said, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” Well, I think we’ve got a wonderful business for a fair price here.

The P/E ratio of 22.5 is basically right there with its own five-year average of 25.4. The cash flow multiple of 17.3 compares slightly favorably to its own five-year average of 17.5. UnitedHealth Group is almost never cheap, nor should it be. It’s a great business. And it deserves a premium valuation relative to most other businesses.

If you don’t yet have this one in your portfolio, the stock’s recent 15% slide may be the opening you need to finally get in. That 15% slide, by the way, hardly detracts from the fact that the stock is up by more than 700% over the last 10 years. If you want to become wealthy, you want compounders like this one working for you.

If you don’t yet have this one in your portfolio, the stock’s recent 15% slide may be the opening you need to finally get in. That 15% slide, by the way, hardly detracts from the fact that the stock is up by more than 700% over the last 10 years. If you want to become wealthy, you want compounders like this one working for you.

The fifth dividend growth stock we have to talk about is Visa (V).

Visa is a multinational financial services corporation. One of my favorite businesses right here. Visa operates almost like a digital toll booth. They operate the financial “toll roads” and collect a fee for using those digital pipes. What do I mean by that?

Well, Visa offers merchants the ability to take payments through Visa’s network, and Visa charges businesses a fee for that payment option. Every time you swipe your Visa card, Visa earns a small percentage of that transaction. With the world becoming more cashless, and with inflation making average transactions more expensive, Visa is a money machine that keeps getting bigger and better. And all of this benefits shareholders, partially through large dividend raises each year.

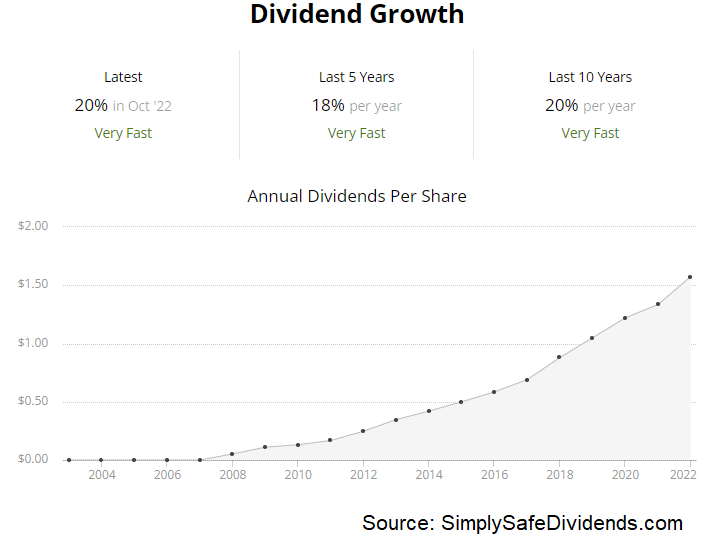

Visa’s 10-year dividend growth rate is 20.3%. And what’s so great about this is the remarkable consistency. There’s been no real deceleration in dividend growth from Visa. The most recent dividend raise came in at 20% on the nose. Just awesome.

Visa’s 10-year dividend growth rate is 20.3%. And what’s so great about this is the remarkable consistency. There’s been no real deceleration in dividend growth from Visa. The most recent dividend raise came in at 20% on the nose. Just awesome.

Visa has increased its dividend for 15 consecutive years. And even after these relentless 20% dividend raises, year after year, the payout ratio is only 25.1%. That’s because the business continues to grow so quickly, which keeps the payout ratio from expanding much.

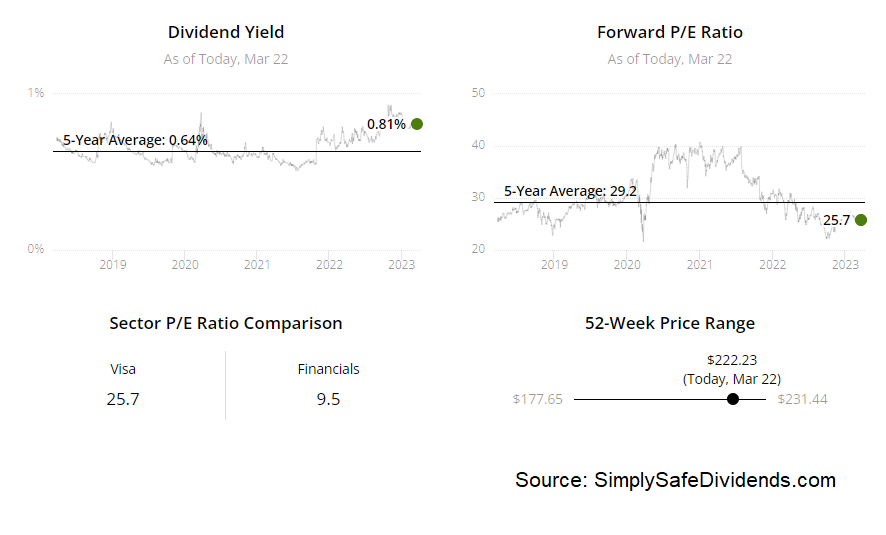

Again, this is a money machine. On the other hand, it’s not an income machine. The stock yields just 0.8%. So it is more suitable for long-term investors who are interested in compounding their money at a high rate.

Visa can be really expensive over long periods of time. But I don’t think now is one of those times. Keep in mind, Visa’s five-year average P/E ratio is 35.9. Yeah. The market has had a bit of a love affair with this business for quite a while, and who can blame the market?

All Visa does is crank out free cash flow. With that in mind, the current P/E ratio of 30.5 looks quite reasonable by comparison. Visa’s stock actually sported a similar valuation and yield back when I invested in 2014.

All Visa does is crank out free cash flow. With that in mind, the current P/E ratio of 30.5 looks quite reasonable by comparison. Visa’s stock actually sported a similar valuation and yield back when I invested in 2014.

Almost everyone thought it was way too expensive back then, yet Visa has quadrupled my investment and the dividend I collect. Will the stock quadruple again over the next nine years? Impossible to say for sure, but I think there’s a very good chance. If you’re looking for an ultra high-quality compounder, Visa is worth serious consideration.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income