Note from DTA: To access Jason’s entire dividend growth stock portfolio, as well as stock trades he makes with his own money, he’s made all of that available exclusively through Patreon.

The S&P 500 has calmed down. It got off to a fast start this year.

But then March came… …With Jay Powell’s aggressive tone. …And the failure of a few banks.

Now we’re basically flat on the year for the broader market.

However, it’s a market of stocks, not a stock market. A lot of individual names are down heavily. But this isn’t a bad thing at all.

Price and yield are inversely correlated. All else equal, lower prices result in higher yields. If your aim is to live off of the safe, growing dividend income your investments provide for you, these lower prices are a gift.

With this in mind, today, I want to tell you about a dividend growth stock that’s down around 30% from its 52-week high…

Hormel Foods (HRL) is an American food processing company with a market cap of $21 billion. Very simple investment thesis here with Hormel. We’re talking about basic food products, primarily based around proteins like chicken. And what do we know about proteins? Well, people have to eat. And with more mouths than ever to feed, that bodes well for food companies.

However, there’s more to it than that, as people tend to demand more proteins when their means improve. As one of the world’s largest providers of proteins, Hormel has a pretty clear path to continued growth, which started all the way back to the company’s founding in 1891. That growth pathway also extends over to the dividend.

The food processing company has increased its dividend for 57 consecutive years.

Yep… a Dividend Aristocrat. Nearly 60 straight years of ever-higher dividends to shareholders. That is the kind of consistency that I really, really love to see and personally benefit from. Stocks move up and down every day. But when your dividend is only increasing, that makes for sound sleeping.

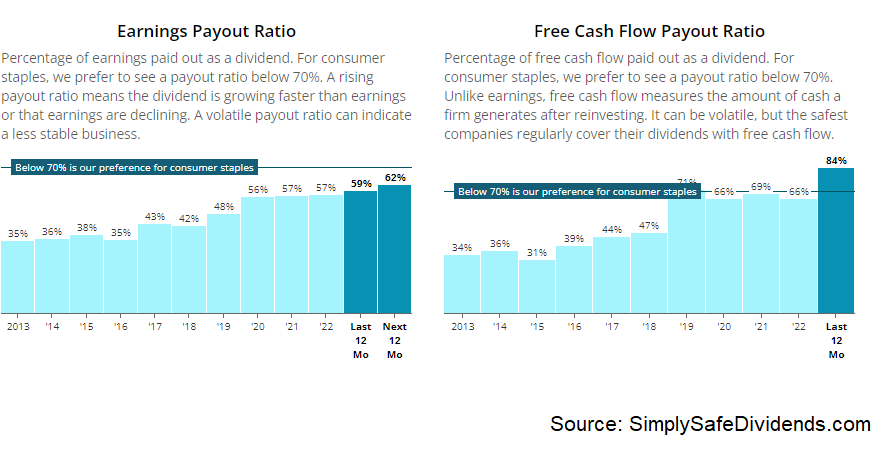

The 10-year DGR is 13.2%, although more recent dividend raises have been in the mid-single-digit range. To compensate for the slowing dividend growth, the yield has risen to 2.8% – 80 basis points higher than its five-year average. The 62.9% payout ratio is slightly elevated, but it’s not concerning.

This stock’s 29% collapse in price has led to a more reasonable valuation.

This stock’s 29% collapse in price has led to a more reasonable valuation.

The 52-week high for this one is $55.11. Shares are currently priced at about $39/each. What this has done is, it’s created a more favorable entry point for long-term investors. To be honest, Hormel has often defied gravity and commanded outrageous valuations.

But a disappointing Q1 report, which lowered FY 2023 EPS guidance to $1.76 at the midpoint, has only reinforced a yearlong correction that has more properly valued the business. The forward P/E ratio, using that guidance, is 22.3. Not super low. But the five-year average P/E ratio for Hormel is 25.9. I’d actually like to see it even lower, but Hormel is interesting again for the first time in a while.

— Jason Fieber

P.S. Shares of Hormel are certainly more attractive today than they have been in a while, but there are much better deals out there right now. In fact, there’s one dividend growth stock in particular I’ve been aggressively buying in recent days… and if you’ve got room in your portfolio for this name, I’d be hitting the gas pedal here. Now is one of the best times you’ll ever see to invest in a business like this, in my view. For the full details on my latest purchases, as well as access to my entire stock portfolio, I invite you to join me over at Patreon.