The power of compounding is immense.

The Rule of 72 states that an investment compounding at a 10% annual rate will double in 7.2 years.

Just think about that.

Your money could double roughly every seven years.

That could turn even a small sum into a relatively large sum after only a few decades.

The best way to take advantage of compounding?

In my view, the answer is long-term dividend growth investing.

This investment strategy espouses buying and holding shares in world-class businesses paying reliable, rising dividends to their shareholders.

How are they able to afford reliable, rising dividends?

By producing reliable, rising profits.

And those reliable, rising profits are produced because these world-class businesses are providing the world with the products and/or services it demands.

It’s really that simple.

Check out the Dividend Champions, Contenders, and Challengers list to see what I mean.

This list contains hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

These are some of the best businesses in the world.

These are some of the best businesses in the world.

And many of them are compounding at annual rates higher than the 10% I mentioned earlier.

Better yet, they’re paying their shareholders safe, growing dividends along the way.

I’ve been implementing the dividend growth investing strategy for more than a decade.

In the process, I built the FIRE Fund.

This is my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

I’ve actually been living off of dividends for a number of years now.

I’ve actually been living off of dividends for a number of years now.

In fact, I was able to quit my job and retire in my early 30s, thanks to dividends.

How did I retire so early?

My Early Retirement Blueprint has the answers.

Suffice it to say, a key pillar of the Blueprint is dividend growth investing.

But it’s not just which stocks you buy but at what valuations you do the buying.

While price is what you pay, it’s value that you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Harnessing the power of compounding by buying undervalued high-quality dividend growth stocks can turn a small sum into a very large sum, all while generating lots of growing dividend income along the way.

But isn’t valuation complex and difficult to understand?

Not really.

My colleague Dave Van Knapp penned Lesson 11: Valuation in order to make it much easier to understand.

Part of an overarching series of “lessons” on dividend growth investing, it lays out a valuation template that can be easily applied toward almost any dividend growth stock you’ll find.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Lowe’s Companies Inc. (LOW)

Lowe’s Companies Inc. (LOW)

Lowe’s Companies Inc. (LOW) is a large home improvement retailer based in the United States.

Founded in 1921, Lowe’s is now a $118 billion (by market cap) retailing giant that employs 300,000 people.

Lowe’s operates approximately 1,700 home improvement and hardware stores in the US.

The typical store averages around 112,000 square feet in size and offers 40,000 different products.

In addition, the company offers hundreds of thousands of products via their special order system and e-commerce channel.

You almost can’t talk about America without referencing what’s known as the “American Dream”.

It’s a set of ideals based around freedom and prosperity.

And part of this prosperity relates to an aspiration toward homeownership.

Homeownership is as American as baseball and apple pie.

Well, what do we know about houses?

They’re physical structures that naturally deteriorate over time, requiring constant upkeep and repairs.

Moreover, because most people want a house to be a home, one that’s customized to their needs, houses almost require ongoing modifications.

All of this plays right into the hands of large home improvement retailers.

These retailers cater to homeowners’ needs by providing the right products and/or services for the job.

Plus, as the US population continues to grow, new houses need to come on the market in order to shelter these people.

That’s even more housing stock that will age and deteriorate over time.

So it’s ever-more products and/or services, to ever-more customers, at ever-higher prices.

And because of that, Lowe’s should be able to keep increasing its revenue, profit, and dividend for decades to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

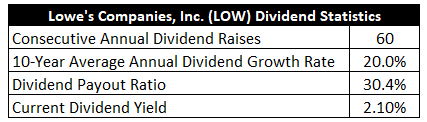

Lowe’s has already increased its dividend for 60 consecutive years.

That is super, super impressive, especially in retailing – an area of the economy that is notoriously competitive and difficult.

It qualifies Lowe’s for its esteemed Dividend Aristocrat status more than twice over.

I think this kind of reliability – six straight decades of ever-higher dividends – is worth something.

Making matters even more impressive, the 10-year dividend growth rate is 20%.

You might not be totally surprised to see a high dividend growth rate like this from some new upstart, fresh into their dividend hiking journey.

But for a company that was already 50 years into that journey a decade ago?

But for a company that was already 50 years into that journey a decade ago?

This is noteworthy.

And with a low payout ratio of 30.4%, based on FY 2023 EPS guidance at the midpoint, even after all of the aggressive dividend growth, this is a well-protected dividend.

The only drawback here might be the yield.

At 2.1%, the stock isn’t a big income play.

Instead, this is a high-quality compounder for those with the time horizon, patience, and vision to see it through.

That said, this yield does beat what the broader market gives you.

And it’s 40 basis points higher than its own five-year average.

These are phenomenal dividend metrics, in my view.

Revenue and Earnings Growth

As phenomenal as they may be, the metrics are largely looking in the rearview mirror.

However, investors must look through the windshield, as they’re risking today’s capital for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will later be of great help when it comes time to approximate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us the ability to roughly judge where the business could be going from here.

Lowe’s expanded its revenue from $53.4 billion in FY 2013 to $97.1 billion in FY 2022.

That’s a compound annual growth rate of 6.9%.

Strong top-line growth here.

I usually look for mid-single-digit top-line growth from a mature business like this.

Lowe’s obviously exceeded my expectations, although it’s been a prime beneficiary of certain pandemic trends, such as moving to the suburbs and/or working from home.

Earnings per share swelled from $2.14 to $10.17 over this period, which is a CAGR of 18.9%.

Incredible.

Excess bottom-line growth was driven by a combination of margin expansion and share buybacks.

For perspective on that latter point, the outstanding share count has been reduced by a stunning 41% over the last decade.

That’s one of the largest repurchase programs I’ve come across.

We can now see how Lowe’s was able to afford the 20% dividend growth rate over the last 10 years – like EPS growth funded most of it, allowing the payout ratio to avoid being expanded.

Looking forward, CFRA believes that Lowe’s will compound its EPS at an annual rate of 7% over the next three years.

This would obviously be quite the slowdown relative to what Lowe’s has done over the last 10 years.

I see this as a very reasonable assessment of the overall situation for the business.

Now, don’t get me wrong.

Lowe’s is a stellar retailer.

But the last few years have been unusually good for the business.

And recent results are unlikely to persist indefinitely.

The pandemic encouraged some people to move out of city apartments and into suburban homes, and some people were allowed to work from home.

All well and good.

But the pandemic is behind us.

Furthermore, odds of a recession are rising, which would almost certainly reduce demand for home improvement projects.

Putting it all together, Lowe’s has to get back to a normal environment.

Is a “normal” environment what CFRA has in mind?

It does seem reasonable to me, and CFRA backs up their assessment with the following passage: “Uncertainties remain in [2023] on how weak consumer spending may be with a potential recession. Home improvement spending is expected to see flat to negative revenue growth in [2023] as sales of existing and new homes slow, mortgage rates rise, and limited house price appreciation dampens home remodeling. [Lowe’s] is improving store layouts, supply of products, and MVP membership with better service for PRO contractors.”

On the other hand, I think we have to be careful about underestimating Lowe’s.

Lowe’s roughly doubled its EPS in the five years leading up to the pandemic.

That’s good for a 19.1% CAGR in EPS during that five-year stretch.

We can cherrypick good or bad stretches, but there’s no doubt that Lowe’s has operated at a high level for decades.

That 60-year dividend growth track record doesn’t get built by magic.

I can take CFRA’s projection at face value.

With the payout ratio being low, and with Lowe’s predisposed to generously rewarding shareholders with large dividend raises, I don’t see why Lowe’s can’t grow the dividend at least at a high-single-digit annualized rate over the next few years.

And you’re starting off with an above-average yield.

It’s difficult to be unhappy about this kind of setup.

Financial Position

Moving over to the balance sheet, Lowe’s has a very good financial position.

Because of negative common equity, there is no long-term debt/equity ratio.

However, the $32.9 billion long-term debt load is unconcerning for a company with a $118 billion market cap.

Furthermore, the interest coverage ratio is north of 17.

Profitability is quite robust for a retailer.

Over the last five years, the firm has averaged annual net margin of 6.2%.

ROE is not applicable because of negative common equity.

Speaking on the margin expansion I touched on earlier, Lowe’s was routinely printing net margin closer to the 4% mark a decade ago.

Overall, Lowe’s is easily one of the best retailers in all of America.

And the company does benefit from durable competitive advantages, including large economies of scale, pricing power, brand recognition, product specialization, and an expert workforce that guides consumer purchases.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

I see competition as the biggest risk of those three, as retailing is notoriously competitive.

Any major changes in the way consumers spend money can affect the business, such as possible pent-up demand for services (as a result of lockdowns) leading to consumer spending flowing away from home projects.

It’s currently unknown how much of a pull-forward of sales has occurred from pandemic-induced trends, but it’s likely that a near-term growth slowdown will materialize.

Rising rates and high inflation will lower demand for new homes, although this may encourage people to stay in, and maintain, their existing homes for longer.

A large-scale recession would almost certainly impact the business.

The company’s US-centric footprint eliminates international growth opportunities.

The global supply chain is still not back to full strength, making it challenging to match supply with demand.

I don’t see these risks as too much to accept, especially when compared to the quality of the business.

And with the stock down nearly 20% from its 52-week high, the attractive valuation only makes the risks easier to swallow…

Stock Price Valuation

The stock is trading for a forward P/E ratio of 14.4.

That’s based on the FY 2023 EPS guidance, at the midpoint.

For a business that’s compounded EPS at nearly 20% annually over the last decade, that’s an extremely low earnings multiple.

We can also compare the current P/CF ratio of 14.6 up against its own five-year average of 15.9.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

Compared to the demonstrated 10-year growth across both EPS and the dividend, this is a very conservative model.

But I’m erring on the side of caution, seeing as how the near-term EPS growth projection is near this level.

My outlook for Lowe’s over the long run is very favorable.

However, it’s also possible that we’ve pulled forward a lot of long-term dividend growth, leading to more modest dividend raises over the coming years.

For example, the most recent dividend raise was a whopping 31%.

I think that gave investors a bit more bird in the hand at the expense of what’s left in the bush.

With EPS growth slowing, that kind of dividend growth cannot continue.

Still, a high-single-digit dividend growth rate, paired with a 2%+ starting yield, is a compelling total package.

The DDM analysis gives me a fair value of $226.80.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I believe I really erred on the side of caution with my valuation, yet the stock still looks at least moderately undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates LOW as a 3-star stock, with a fair value estimate of $218.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates LOW as a 3-star “HOLD”, with a 12-month target price of $235.00.

We’re all pretty much on the same page here. Averaging the three numbers out gives us a final valuation of $226.60, which would indicate the stock is possibly 12% undervalued.

Bottom line: Lowe’s Companies Inc. (LOW) is one of America’s best retailers. It’s really one of America’s best businesses, period. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, 60 consecutive years of dividend increases, and the potential that shares are 12% undervalued, long-term dividend growth investors looking for a good deal on a high-quality Dividend Aristocrat should have their eyes on this name.

Bottom line: Lowe’s Companies Inc. (LOW) is one of America’s best retailers. It’s really one of America’s best businesses, period. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, 60 consecutive years of dividend increases, and the potential that shares are 12% undervalued, long-term dividend growth investors looking for a good deal on a high-quality Dividend Aristocrat should have their eyes on this name.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is LOW’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 93. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, LOW’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income