Great investment opportunities are everywhere.

Some of the world’s best businesses are very obvious.

You see their brands.

You see, and sometimes personally use, their products and/or services.

So why not put some capital to work and profit from what you see and use?

I’ve taken this advice myself, investing in many companies that are providing what I use every day.

Best of all?

I’m getting paid to use what I’d use anyway.

That occurs through safe, growing dividends.

That’s because I only invest in high-quality dividend growth stocks.

These stocks represent equity in world-class businesses that reward their shareholders with reliable, rising dividends.

Reliable, rising dividends are possible because reliable, rising profits are being produced.

And reliable, rising profits are being produced because the products and/or services the world demands are being sold at ever-higher quantities.

You can find hundreds of these stocks by perusing the Dividend Champions, Contenders, and Challengers list.

This list contains invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

By routinely buying these stocks with my hard-earned savings, I built the FIRE Fund.

This is my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I’ve actually been living off of dividends for years.

I’ve actually been living off of dividends for years.

I even quit my job and retired in my early 30s.

How did I do that?

My Early Retirement Blueprint explains.

Much of my success has come down to buying the right stocks.

But that’s not all.

It’s also been about buying them at the right valuations.

Whereas price tells you what you pay, value tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Investing in the obvious by buying high-quality dividend growth stocks when they’re undervalued can allow one to become wealthy and get paid ever-more passive dividend income to use the products and/or services they’re already using.

Now, this would require one to first have a basic understanding of valuation.

But this, too, is more obvious than you might think.

My colleague Dave Van Knapp penned Lesson 11: Valuation in order to make the concept of valuation even more simple and obvious.

This is part of an overarching series of “lessons” that are designed to teach the dividend growth investing strategy.

It can help you to estimate the fair value of just about any dividend growth stock you’ll run across.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Pfizer Inc. (PFE)

Pfizer Inc. (PFE)

Pfizer Inc. (PFE) is a multinational pharmaceutical and biotechnology corporation.

Founded in 1849, Pfizer is now a $231 billion (by market cap) healthcare behemoth that employs approximately 83,000 people.

The company’s FY 2022 sales are broken down into the following three customer groups: Primary Care, 73%; Specialty Care, 14%; and Oncology, 12%.

The US is Pfizer’s largest single market and accounts for 42% of sales, while the remainder is international.

Pfizer has a roster of blockbuster drugs that includes Ibrance and Eliquis – both doing over $5 billion annually in sales.

The company’s Prevnar family of vaccines also does over $5 billion per year in sales.

And, perhaps unsurprising to anyone not living under a rock, Pfizer has had great financial success with its Covid-19 treatments, including the Comirnaty vaccine and the Paxlovid oral medication.

These two products have greatly boosted Pfizer’s overall sales – and they continue to do so, despite the fact that we are more than three years removed from the onset of the pandemic.

For perspective here, Pfizer is guiding for ~$21.5 billion in combined sales for these two Covid-19 offerings alone during FY 2023.

While these massive sales numbers will not persist indefinitely, the temporary bonanza has allowed Pfizer to amass a war chest of cash that can be used for M&A in order to bolster the pipeline.

Indeed, the company has already been putting some of that capital to work.

Pfizer’s $5.4 billion acquisition of Global Blood Therapeutics and $11.6 billion acquisition of Biohaven Pharmaceutical Holding Co. – both completed in 2022 – are perfect examples.

This is a strong legacy business becoming even stronger.

That bodes extremely well for Pfizer’s ability to drive its revenue, profit, and dividend higher for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

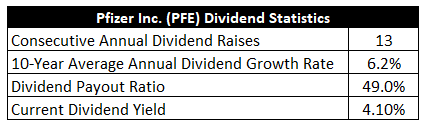

To date, the company has increased its dividend for 13 consecutive years.

The 10-year dividend growth rate is 6.2%, which is right about what I’d expect for a mature pharmaceutical business like this.

That said, the last few dividend raises have been quite small – in the 3% range.

That said, the last few dividend raises have been quite small – in the 3% range.

There are reasons for this, which I’ll get into, but I also expect this to be a temporary reduction in growth rate of the dividend.

Meantime, the stock offers a market-smashing 4.1% yield.

Notably, that’s 50 basis points higher than its own five-year average.

And with the payout ratio sitting at 49%, based on adjusted EPS guidance at the midpoint for FY 2023, this dividend appears to have no issues whatsoever with sustainability.

For income-oriented dividend growth investors, there’s a lot to like here.

Revenue and Earnings Growth

As likable as these numbers may be, they’re largely looking backward.

But investors are always risking the capital of today for the rewards of tomorrow.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will later be instrumental when it comes time to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then unveil a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this manner should give us the ability to roughly gauge where the business may be going from here.

Pfizer moved its revenue from $51.6 billion in FY 2013 to $100.3 billion in FY 2022.

That’s a compound annual growth rate of 7.7%.

Strong top-line growth for a mature business like this.

However, this has been anything but straightforward.

There are a lot of moving parts to account for.

Pfizer spun out what become the pets and livestock medicine and vaccinations maker Zoetis Inc. (ZTS) in 2013.

Zoetis is now a $77 billion (by market cap) company in its own right.

Pfizer completed a joint venture with GlaxoSmithKline PLC (GSK) in August 2019.

This JV saw Pfizer merge its former consumer healthcare segment with GlaxoSmithKline’s consumer healthcare division.

This division was later spun out into what is now an independent business called Haleon PLC, which is traded on the London Stock Exchange.

Pfizer owns 32% of Haleon, which has a market cap of $30 billion.

Also, Pfizer recently spun off and combined Upjohn, its off-patent branded and generic established medicines business, with Mylan N.V., creating a new global pharmaceutical company named Viatris Inc. (VTRS).

Viatris is a $13 billion (by market cap) company.

Pfizer has been busy.

Looking at profit growth on a per-share basis will clean up some of this messiness, although even this has unusual activity to account for.

Earnings per share grew from $3.19 to $5.47 over this period, which is a CAGR of 6.2%.

We can see how this lines up precisely with the 10-year dividend growth rate, showing prudence and care on the part of management – even through all of the corporate movements.

Recent results can’t be discussed without mentioning the massive, but temporary, impact that Pfizer’s Covid-19 offerings have had.

We’re talking billions of dollars in sales that wouldn’t otherwise exist in a world where the pandemic had never occurred.

On one hand, had they left things alone, Pfizer might be even better today than it already is.

Zoetis, for instance, has been wildly successful.

On the other hand, regardless of how one personally feels about the situation, the pandemic was an economic boon for the business, as Pfizer stepped in with tailor-made vaccines and medicines and raked in the cash.

However, this hasn’t necessarily been a boon for the stock.

This was a $39 stock in early 2020.

It’s currently a $40 stock.

Those who don’t follow the stock market would be forgiven for assuming that Pfizer’s stock has skyrocketed.

Indeed, revenue has skyrocketed – the $100 billion sales base is twice what it was heading into early 2020.

Despite all of the hoopla, though, the stock has “round tripped” and is now back to where it started more than three years ago.

Of course, this surprising disconnect between expectations and reality is why I’m covering the name for the first time in nearly three years.

Furthermore, it’s where a business is going, not where it’s been, that matters to those investing today.

Looking forward, CFRA is forecasting a 10% CAGR for Pfizer’s EPS over the next three years.

If this projection materializes, it would represent a substantial acceleration in bottom-line growth.

It’s always difficult to forecast a growth rate for a business.

But I think it’s especially difficult in this case, as there are just so many moving parts.

CFRA does a pretty good job of summing up the situation from a high level with this passage: “On the one hand, [Pfizer] estimates it has about $17B of revenues at risk between 2025 and 2030 due to looming loss of exclusivity. On the other hand, though, we think the pipeline is strong enough to offset these risks and thrive. [Pfizer] has 19 drugs in development (including 15 developed in house) with potential for $20 billion in revenues by 2030. That so many of these prospective drugs have been developed internally is a positive sign in our view that [Pfizer] is not dependent on M&A to replenish its portfolio. On the M&A front, [Pfizer] still has the ability (and the war chest) to pursue business development opportunities, given the windfall from Covid-19 related sales.”

That’s basically how I see it.

You’ve got a very decent legacy business that’s probably been overly tweaked via unnecessary busyness and portfolio tinkering, and this business fortunately walked right into a pandemic windfall.

The pipeline is huge, and the company’s war chest is being deployed in a way that makes it even bigger.

Pfizer has 110 total compounds its pipeline, with 23 in phase 3.

This negates a lot of concern around patent cliffs, such as the 2023 US patent expiration for Ibrance.

So how does all of this translate over to the dividend?

Well, if Pfizer is able to compound its EPS at a 10% annual rate over the foreseeable future, that would open the door for similarly-sized dividend raises.

I believe Pfizer has been conservative with the dividend raises of late because of the Viatris spin off and the desire to use cash to buy growth.

I have no problems with that.

But with Viatris in the rearview mirror, and with M&A mostly being digested now, Pfizer could be set up to get back to its prior dividend growth ways of 6% or so – at the very least.

In fact, I’d argue, as CFRA seems to believe, that the Pfizer of 2023 is better than the Pfizer of 2020 was.

Now, some near-term caution may still be warranted, as overall sales will be falling in the wake of much less demand for Covid-19 offerings.

But things should smooth out nicely over the next 24-36 months.

And if Pfizer is able to increase the dividend at a high-single-digit rate, the 4%+ starting yield makes this a compelling total package.

Financial Position

Moving over to the balance sheet, Pfizer has a terrific financial position.

The long-term debt/equity ratio is 0.3, while the interest coverage ratio is over 29.

Furthermore, Pfizer has a total cash position that’s nearly enough to wipe out all long-term debt.

The balance sheet is something that has shown marked improvement over the last few years.

Profitability is spectacular, although the last two years have really juiced the numbers.

Over the last five years, the firm has averaged annual net margin of 28.9% and annual return on equity of 26.2%.

I suspect that these numbers will come down a bit, but there’s a lot of cushion here.

Overall, Pfizer is running a great outfit.

Sales will fall from unsustainable levels, but the pipeline strengthening should assist the company for years to come.

And with patents, IP, inelastic demand for products, R&D, economies of scale, technological know-how, and global relationships, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Competition, regulation, and litigation are omnipresent risks in every industry.

I see all three of these risks as elevated in this particular industry.

Pfizer is facing concerns around patent losses over the next few years, which puts pressure on the large pipeline to produce more blockbuster drugs.

Any large-scale changes to the US healthcare system would almost certainly impact Pfizer.

The company’s international footprint exposes it to currency, geopolitical, and foreign regulatory risks.

Pfizer has recently been very acquisitive, introducing integration risks and questions around capital allocation.

Pfizer’s size is an advantage, but the law of large numbers may start to come into play and limit growth.

I see these risks as pretty standard and quite acceptable for a large pharmaceutical business.

And with the stock down nearly 30% from its 52-week high, the valuation appears to be pricing in all of these risks and then some…

Stock Price Valuation

The P/E ratio is 7.3.

That’s less than half of the stock’s five-year average P/E ratio of 15.7.

However, this is somewhat misleading, as it’s capturing a lot of temporary sales and profits.

The forward P/E ratio of 12, using midpoint guidance for FY 2023 adjusted EPS, is a fairer way to look at the earnings multiple.

Still, that’s well below average and what I think one would reasonably expect to pay for a business of this stature and quality.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 6%.

This dividend growth rate lines up almost exactly with what Pfizer has demonstrated in terms of its EPS and dividend growth over the last decade.

I’m essentially ascribing zero value to the windfall, war chest, pipeline improvement, and growth acceleration forecast by CFRA.

It’s a huge margin of safety being built in, as I just see so many moving parts and uncertainty.

Moreover, the last few dividend raises have been relatively small.

I believe Pfizer could easily blow away this model over the next decade, even if the next one or two dividend raises are underwhelming.

Weighing out the desire to sleep well at night, I’m erring on the side of caution here.

The DDM analysis gives me a fair value of $43.46.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think I was being very cautious and judicious with the valuation, yet the stock comes out looking cheap anyway.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates PFE as a 4-star stock, with a fair value estimate of $48.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates PFE as a 4-star “BUY”, with a 12-month target price of $52.00.

I came out rather low. Perhaps I was too cautious. Averaging the three numbers out gives us a final valuation of $47.82, which would indicate the stock is possibly 16% undervalued.

Bottom line: Pfizer Inc. (PFE) is a world-class firm that comes out of the pandemic looking far better than it went into it. It’s wisely using its war chest to bolster its pipeline and set up the business for another generation of growth. With a market-smashing yield, solid dividend growth, a balanced payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 16% undervalued, income-oriented dividend growth investors ought to take a close look at this stock after its stunning fall.

Bottom line: Pfizer Inc. (PFE) is a world-class firm that comes out of the pandemic looking far better than it went into it. It’s wisely using its war chest to bolster its pipeline and set up the business for another generation of growth. With a market-smashing yield, solid dividend growth, a balanced payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 16% undervalued, income-oriented dividend growth investors ought to take a close look at this stock after its stunning fall.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is PFE’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 75. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, PFE’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income