Warren Buffett’s wisdom was recently on full display once again.

His released his 2023 annual letter only days ago.

That letter included an important lesson for investors.

After reminiscing on his long, fabled career, he pointed out that only a few key decisions have made up the bulk of his success.

He summed it up like this: “Over time, it takes just a few winners to work wonders.”

See, a few big winners can make up for a lot of small losers.

Winners can win far more than losers can lose – a stock’s upside is theoretically infinite, while the downside is limited to going to $0.

So how do we find winners?

Well, I’d argue that we should, yet again, follow in Buffett’s footsteps and look for high-quality dividend growth stocks.

These stocks represent equity in world-class businesses that pay reliable, rising dividends to their shareholders.

Those reliable, rising dividends get funded by reliable, rising profits.

Many of Buffett’s biggest winners are high-quality dividend growth stocks that he’s held for decades.

You can find many of these stocks by perusing the Dividend Champions, Contenders, and Challengers list.

This list contains invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

My FIRE Fund is loaded to the gills with these stocks.

My FIRE Fund is loaded to the gills with these stocks.

The Fund is my real-money dividend growth stock portfolio, and it produces enough five-figure passive dividend income for me to live off of.

I built the Fund so that I could retire early and live off of the dividend income it produces.

Well, it worked out pretty well.

I quit my job and retired in my early 30s.

My Early Retirement Blueprint lays out exactly how I was able to do that.

Suffice it to say, routinely using my savings to buy high-quality dividend growth stocks has been a big part of it.

But, as Buffett would point out, that’s not all.

But, as Buffett would point out, that’s not all.

It’s not just which stocks you buy but at what valuations you buy.

Price is what you pay, but it’s value that you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Funneling Warren Buffett’s lesson on winners into buying undervalued high-quality dividend growth stocks should serve an investor very well over the long term, leading to extraordinary amounts of wealth and passive dividend income.

Of course, finding undervaluation requires one to first understand valuation.

But this isn’t as difficult as it might seem.

Dave Van Knapp, my colleague, put together Lesson 11: Valuation in order to break down the concept of valuation.

Part of a comprehensive series of “lessons” on dividend growth investing, it provides a template that can be used to estimate the fair value of just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

American Tower Corp. (AMT)

American Tower Corp. (AMT)

American Tower Corp. (AMT) is a real estate investment trust that owns, operates, and develops broadcast communications infrastructure across the world.

Founded in 1995, American Tower is now a $91 billion (by market cap) infrastructure giant that employs over 6,000 people.

The company’s portfolio includes approximately 223,000 communications sites, with more than 43,000 in the US and roughly 180,000 internationally.

American Tower’s basic business model involves the rental and management of vertical antenna sites to service providers.

Service providers sign multiyear leases in order to access towers and install their equipment.

This equipment is necessary to carry out services such as telephony, mobile data, radio, and broadcast television.

In addition, after the acquisition of CoreSite Realty Corporation in late 2021, American Tower owns and operates interconnected data center facilities.

American Tower expects this acquisition to enhance the value of its existing tower real estate through emerging edge computing opportunities.

Regardless of exactly how that plays out, 5G and IoT are converging to make American Tower’s infrastructure more critical than ever before.

For example, an average smartphone user might consume somewhere around 10 gigabytes per month in mobile data.

On the other hand, a self-driving car is thought to use somewhere around 4 terabytes of data per day.

We’re talking about exponential increases in mobile data usage that can be measured in orders of magnitude.

Moreover, American Tower has a unique advantage built right into the business model.

It domes down to the way in which its real estate can be easily leveraged.

Once a tower is built, there is a lot of available scalability in terms of bringing on additional tenants.

Each tower is a bit of a compounding money machine for American Tower: Adding tenants, equipment, and upgrades results in much higher returns per tower, as revenue is added with minimal incremental cost.

When you have thousands of compounding money machines, it’s not hard to imagine how the entire enterprise has become a compounding money machine.

That’s what bodes so well for American Tower to continue increasing its revenue, profit, and dividend for many years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

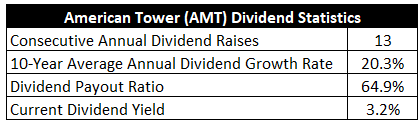

To date, the REIT has increased its dividend for 13 consecutive years.

The 10-year dividend growth rate of 20.3% is uncharacteristically high for a REIT, although more recent dividend growth has been in the 13% range.

Still, that’s an exceptionally high dividend growth rate for what is typically an income vehicle.

On the other hand, the stock’s 3.2% yield isn’t terribly impressive for a REIT.

On the other hand, the stock’s 3.2% yield isn’t terribly impressive for a REIT.

But it is 130 basis points higher than its own five-year average.

That’s a noteworthy spread.

What I think is happening here is, the market is adjusting the yield higher to account for the slowing dividend growth rate.

The business has become very large and mature, making that 20%+ dividend growth rate almost certainly a thing of the past.

However, a new reality of a 3%+ yield and a 10%+ dividend growth rate would be a very nice once.

And with the payout ratio sitting at 64.9%, based on midpoint guidance for FY 2023 AFFO/share, the dividend is healthy and positioned for business-like growth.

I like dividend growth stocks in what I refer to as the “sweet spot” – a yield of between 2.5% and 3.5%, paired with high-single-digit (or better) dividend growth.

Both the yield and dividend growth here are very, very sweet.

Revenue and Earnings Growth

As sweet as these dividend metrics may be, they’re largely looking backward.

But investors are risking today’s capital for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will later be of great use when it comes time to estimate intrinsic value.

I’ll first show you what this business has done over the last decade in terms of top-line and bottom-line growth.

I’ll then uncover a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us what we need in order to gauge where the business might be going from here.

American Tower pushed its revenue from $3.4 billion in FY 2013 to $10.7 billion in FY 2022.

That’s a compound annual growth rate of 13.6%.

Extremely strong top-line growth.

However, when it comes to REITs, you really have to look at profit growth on a per-share basis.

That’s because REITs use debt and equity to fund growth, as they’re legally required to distribute at least 90% of their taxable earnings to shareholders.

This circles back around to why I earlier referred to this REIT as an income vehicle.

Now, when assessing profit for a REIT, it’s imperative to look at funds from operations instead of normal earnings.

FFO (or adjusted FFO) is a measure of cash generated by a REIT, which adds depreciation and amortization expenses back to earnings.

American Tower’s AFFO/share grew from $3.68 to $10.12 over this period, which is a CAGR of 11.9%.

We can clearly see a business that has been growing at a double-digit clip for a long time.

Impressive stuff.

Looking forward, CFRA currently has no projection for American Tower’s FFO/share growth over the next three years.

This is unfortunate, as I do like to compare the proven past up against a future forecast and see how things line up.

However, this passage from CFRA highlights their optimism: “[American Tower] will likely benefit, in our view, from higher demand from U.S. wireless carriers as growth in mobile data traffic remains robust and as new spectrum deployments take place throughout the year.”

CFRA adds this: “International markets pose the greatest opportunity for [American Tower] moving forward, by our analysis. 4G penetration remains moderate in many international markets such as Latin America (currently about 50%) and Africa (around 15%). [American Tower] will continue investing heavily in these regions through both tower acquisitions and new builds to address the upcoming wave of demand.”

I see good reason to be optimistic.

On the other hand, the deceleration in growth is noticeable.

The $10.12 in AFFO/share for FY 2022 was only 4.9% higher than the $9.65 produced for FY 2021.

And American Tower is guiding for $9.61 at the midpoint in AFFO/share for FY 2023.

It’s still a fantastic business centered around necessary infrastructure.

But it’s starting to become a victim of its own success, in my view – its size may be starting to work against it.

And so some of the downward adjustment in price by the market seems justified.

This action has caused the yield to rise in order to compensate investors for the lower growth.

I think it’s reasonable to expect a high-single-digit growth rate in AFFO/share and the dividend for the foreseeable future.

That wouldn’t be the kind of growth that shareholders have enjoyed in the past, but it would still be great.

It should be pointed out that those buying in now are getting a much higher starting yield than shareholders in the past.

If you lean a bit more toward yield than growth, American Tower may actually be more interesting now than it’s ever been before.

Financial Position

Moving over to the balance sheet, American Tower has a good financial position.

The REIT has $67.2 billion in total assets against $54.8 billion in total liabilities.

American Tower’s credit ratings are in investment-grade territory: BBB-, S&P; BBB+, Fitch; Baa3, Moody’s.

While the company may not be growing as fast as it once was, there’s still a lot to like about American Tower.

And with economies of scale, switching costs, and entrenched infrastructure, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

A REIT’s capital structure relies on external funding for growth, which exposes the company to volatile capital markets (via equity) and interest rates (via debt).

Speaking of interest rates, higher rates can hurt the company twice over: Debt becomes more expensive to take on and service, and equity can become more expensive (because income-sensitive investors have alternatives, which pressures the stock).

The international footprint comes with more growth opportunities, but it also exposes the company to currency exchange fluctuations and geopolitics.

Customer concentration is a risk, as three major telecommunications companies account for over half of the company’s revenue.

The company’s scale is an advantage, but it also introduces questions around growth and the law of large numbers.

LEO satellites present a technological risk, as the possible viability of LEO satellites as an antenna alternative in the future could make towers obsolete.

I see these risks as manageable.

And with the stock down 30% from its 52-week high, the attractive valuation seems to be more than pricing these risks in…

Stock Price Valuation

The forward P/AFFO ratio is 20.3.

That’s based on midpoint guidance for this year’s AFFO/share.

This stock has typically commanded a much higher cash flow multiple than that – commonly over 25.

Consider the current P/S ratio of 8.4, which is much lower than its own five-year average of 12.

I do think some multiple compression is justified here.

But, as noted earlier, as a result of this compression, the yield is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

Now, this kind of growth rate can look aggressive or conservative, depending on which way you look at it.

Compared to the demonstrated dividend growth over the last decade, it’s super conservative.

In comparison to more recent bottom-line growth, it might look a tad aggressive.

If I were doing this analysis five years ago, this kind of dividend growth rate expectation would almost be an insult to American Tower.

But it’s a new reality.

That reality is not at all a bad one.

It’s just one in which the business grows slower than it used to, which is part of the lifecycle for just about every business on the planet.

Overall, I see this as a reasonable expectation for American Tower on a go-forward basis.

The DDM analysis gives me a fair value of $222.56.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I feel that my analysis was prudent, yet the stock still comes out looking decently cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates AMT as a 3-star stock, with a fair value estimate of $220.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates AMT as a 4-star “BUY”, with a 12-month target price of $230.00.

Pretty tight consensus this time around, which gives me even more confidence in my analysis. Averaging the three numbers out gives us a final valuation of $224.19, which would indicate the stock is possibly 15% undervalued.

Bottom line: American Tower Corp. (AMT) is a great way to play real estate, infrastructure, and humanity’s increasing thirst for mobile data. With a market-beating yield, a double-digit long-term dividend growth rate, a healthy payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, this looks like a compelling long-term investment idea for dividend growth investors.

Bottom line: American Tower Corp. (AMT) is a great way to play real estate, infrastructure, and humanity’s increasing thirst for mobile data. With a market-beating yield, a double-digit long-term dividend growth rate, a healthy payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, this looks like a compelling long-term investment idea for dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is AMT’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 78. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, AMT’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income