I look at high-quality dividend growth stocks as golden geese. And these golden geese lay golden eggs.

Those golden eggs are, of course, dividends. Best of all, the pile of eggs that a true golden goose can lay… grows and grows and grows. That occurs via dividend increases.

Those dividend increases are possible because profit is increasing. And profit is increasing because you’re running a world-class business.

It’s an amazing virtuous circle. If you want to live off of safe, growing dividends, you want to own high-quality dividend growth stocks for the long run.

Today, I want to tell you about 6 dividend growth stocks that just increased their dividends.

Ready? Let’s dig in.

The first dividend increase I want to highlight is the one that came from Essex Property Trust (ESS).

Essex Property Trust just increased its dividend by 5%.

Good stuff. Essex Property Trust shareholders are now getting 5% more dividend income for doing nothing other than holding the shares they already had. That’s how easy dividend growth investing is. Dividends are the most passive form of income I’ve ever come across. And dividend raises are the easiest pay raises I’ve ever come across.

This is the 29th consecutive year of dividend increases for the multifamily property real estate investment trust.

We’ve got an esteemed Dividend Aristocrat on our hands. For nearly 30 straight years, Essex Property Trust has been delivering the goods, acting as a golden goose laying ever-more golden eggs for its owners.

We’ve got an esteemed Dividend Aristocrat on our hands. For nearly 30 straight years, Essex Property Trust has been delivering the goods, acting as a golden goose laying ever-more golden eggs for its owners.

The 10-year DGR is 7.2%, although more recent dividend raises have been in this mid-single-digit range. Meanwhile, the stock offers a compelling 3.8% yield. And based on midpoint guidance for FY 2023 core FFO/share, the payout ratio is 62.6%. That’s actually quite healthy for a REIT.

In my view, Essex Property Trust is a no-brainer long-term investment here.

In fact, I named it as one of my top five dividend growth stock ideas for 2023. We last analyzed and valued the REIT late last year, showing why fair value was estimated at just under $300/share. The stock is currently priced at right about $230. I see a lot of upside on this Dividend Aristocrat offering a near-4% yield. And it only looks better after yet another solid dividend raise.

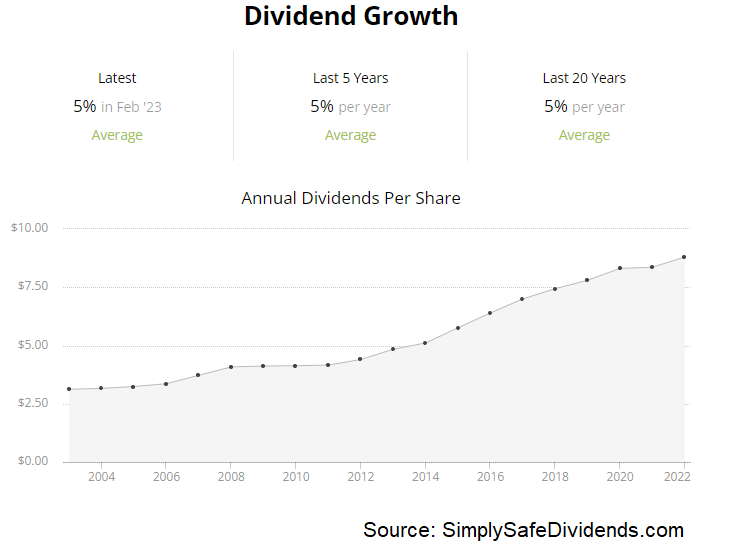

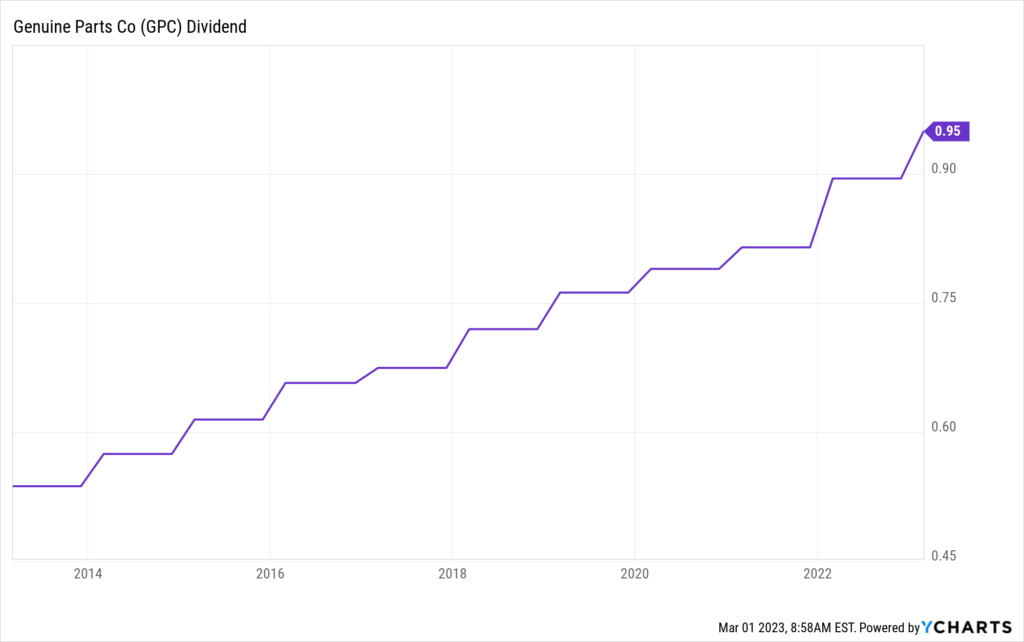

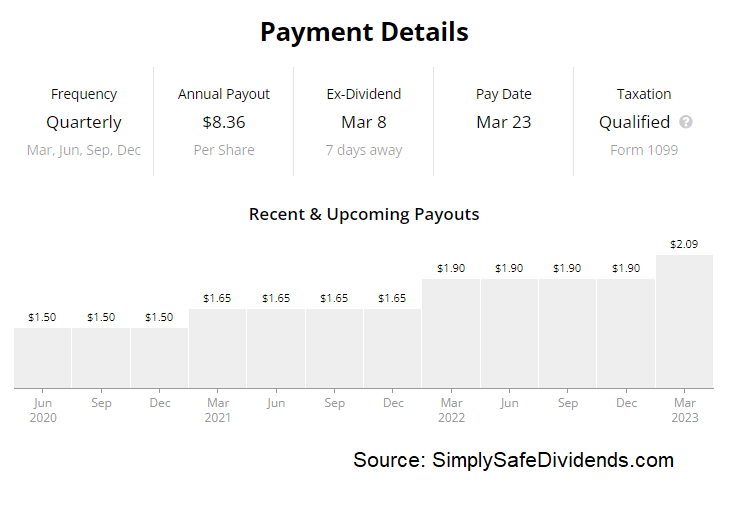

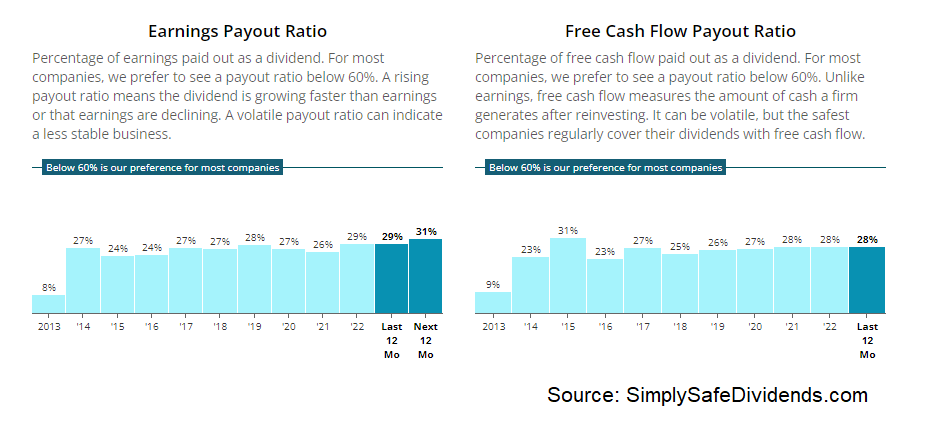

The second dividend increase I have to cover for you is the one that given out by Genuine Parts Company (GPC).

Genuine Parts just increased its dividend by 6.1%. Okay. Not the biggest dividend increase in today’s group. Still, it is more money. What Genuine Parts might lack in terms of huge growth, they more than make up for in terms of incredible consistency.

The automotive parts company has now increased its dividend for 67 consecutive years.

Wow. As someone who loves to own businesses that can demonstrate the ability to reliably increase dividends over the course of decades, I absolutely adore this track record. It’s one of the best out there.

Wow. As someone who loves to own businesses that can demonstrate the ability to reliably increase dividends over the course of decades, I absolutely adore this track record. It’s one of the best out there.

The 10-year DGR of 6.1% is yet another hallmark of the legendary consistency. That lines up pretty nicely with this most recent dividend raise. The stock’s yield of 2.1% is a bit lower than I’d like to see it. Then again, based on the midpoint of FY 2023 adjusted EPS, the payout ratio of 42.8% indicates that this dividend will be increased in about a year’s time yet again. Just like clockwork.

So much to like about Genuine Parts, except the valuation. Love the company’s commitment to dividend increases, year in and year out, no matter what. Even among fellow Dividend Aristocrats, Genuine Parts is royalty. It exists in rarefied air.

Unfortunately, that kind of quality is commanding a hefty premium right now. Just about every valuation metric I look at is well above its respective recent historical average. The P/CF ratio of 17.4 is quite a bit higher than its own five-year average of 13.1. On the other hand, using that aforementioned adjusted EPS guidance for the coming fiscal year, the forward P/E ratio is 20.2. Not totally unreasonable for this kind of business, but I’d really like to see a good-sized pullback here.

The third dividend increase I want to bring to your attention is the one that was announced by Home Depot (HD).

Home Depot just increased its dividend by 10%. How can you not love this? A 10% “pay raise” for doing nothing other than being a shareholder? That’s about as good as it gets in life. I’ve said it before, and I’ll say it again. Home Depot oughta be thought of as the dividend depot.

This marks the 14th consecutive year of dividend increases for the home improvement retailer. What’s great about Home Depot is the way in which they consistently increase the dividend by a double-digit rate. The 10-year DGR is 20.7%. And last year’s dividend raise came in at over 15%.

A deceleration? Sure. But the US housing market has been due for an epic correction. Home Depot coming through, despite it all, is evidence of just how reliable this business is.

A deceleration? Sure. But the US housing market has been due for an epic correction. Home Depot coming through, despite it all, is evidence of just how reliable this business is.

The stock yields 2.8%, which is 60 basis points higher than its own five-year average. And even after the dividend boost, the payout ratio is an even 50%, which I regard as, essentially, a “perfect” payout ratio that exactly balances retaining earnings against returning capital back to shareholders.

Home Depot isn’t super cheap, but I think it’s a pretty good idea right now. Our last full analysis and valuation video on this business came out back in September. In that video, the estimate for intrinsic value came out to a bit under $350/share. The stock’s price is now at under the $300 mark. This is one of the best retailers I’ve ever looked at. And being able to buy in at a reasonable valuation, with a near-3% yield, fresh off of a 10% dividend raise? All of that sounds good to me.

The fourth dividend increase we have to talk about is the one that came courtesy of Intercontinental Exchange (ICE).

Intercontinental Exchange just increased its dividend by 10.5%. Boom. Another double-digit dividend raise. You know, I could get used to this. It’s a tough life, being a dividend growth investor, but I think we can manage. Right?

The global financial and technology company has now increased its dividend for 11 consecutive years.

These dividend metrics are really nice for younger dividend growth investors who are more interested in long-term compounding over current income. The five-year DGR is 13.7%, so double-digit dividend growth is a pretty common feature here.

And with a payout ratio of only 31.7%, based on FY 2022 adjusted EPS, it does seem like more double-digit dividend growth is on its way. The only issue here is the 1.6% yield. As I just alluded to, it’s not an income play. It’s a compounder.

I think this is a terrific business that should make its shareholders very wealthy over the coming decades.

I think this is a terrific business that should make its shareholders very wealthy over the coming decades.

If you want cheap yield, you can find that elsewhere. Of course, cheap yield tends to perform quite poorly. You tend to get what you pay for. This business, on the other hand, just continues to print money and make its investors a lot of money, as evidenced by yet another strong dividend raise.

We recently put out a video analyzing and valuing the business, estimating its fair value at right about $120/ share. This business owns the New York Stock Exchange. The stock market store is my favorite store, and high-quality dividend growth stocks like this one are my favorite merchandise. Plus, my merchandise pays me more and more to buy and own it. Pretty sweet.

Next up, let’s have a quick discussion about the dividend increase that came from PepsiCo (PEP).

PepsiCo just increased its dividend by 10%. Yet another double-digit dividend increase from yet another high-quality company providing the world with more and more of the products it demands – and doing that providing to more people, at higher prices.

This is the 51st consecutive year of dividend increases for the global beverage, food, and snack company.

PepsiCo is living up to its Dividend Aristocrat status. When I was born, this company had already been increasing its dividend for more than a decade straight. And I’m no spring chicken any more.

PepsiCo is living up to its Dividend Aristocrat status. When I was born, this company had already been increasing its dividend for more than a decade straight. And I’m no spring chicken any more.

The 10-year DGR is 7.8%, so this most recent dividend boost is actually outsized and most welcome by shareholders. The stock now yields a respectable 2.9%. And the payout ratio, based on midpoint guidance for FY 2023 Core EPS, is 69.8%. Higher than I’d like to see it, but PepsiCo has been operating with an elevated payout ratio for a number of years now.

It’s one of my favorite businesses. Not cheap. But it’s a terrific long-term compounder.

I’ve been investing for more than a decade now. Guess what I’ve consistently heard about PepsiCo for the whole time? That its stock is too expensive. Well, all PepsiCo has done over the last decade is grow the business and compound its shareholders’ wealth at about 12% annually.

What’s it worth to have your wealth compound at a 12% clip annually – from a very predictable, low-risk business model? I think that’s worth quite a bit. The forward P/E ratio, based on that aforementioned guidance, is 24.3. The stock’s five-year average P/E ratio is 25.5. I see nothing egregious here. Decades from now, I think shareholders are going to be very happy with their investment. Those complaining about expensiveness will still be doing so and missing out.

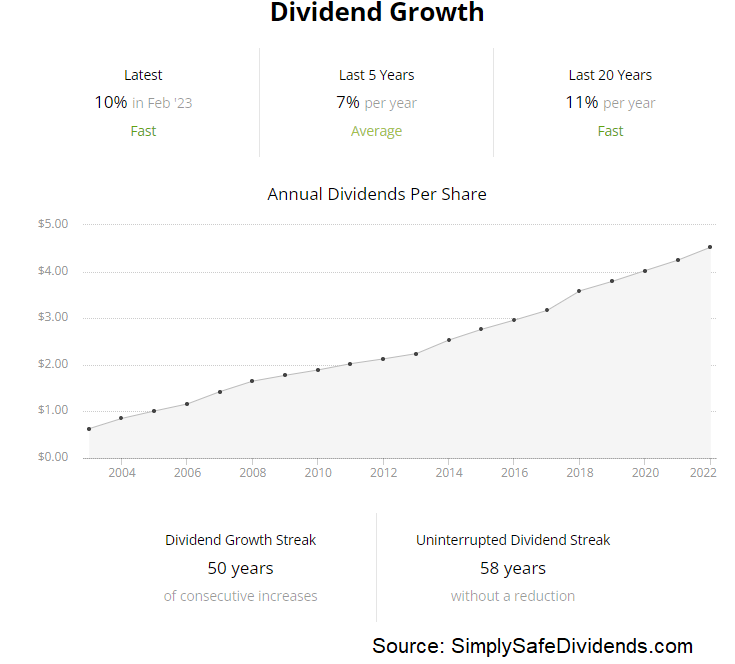

Last but not least, let’s talk about the dividend increase that was announced by Prudential Financial (PRU).

Prudential just increased its dividend by 4.2%. The smallest dividend increase I’m featuring today, but here’s the thing: When you own a diversified portfolio of high-quality dividend growth stocks, things tend to average out nicely. You might get some small dividend raises here and there, but then those big, double-digit dividend raises will come in and boost the overall average.

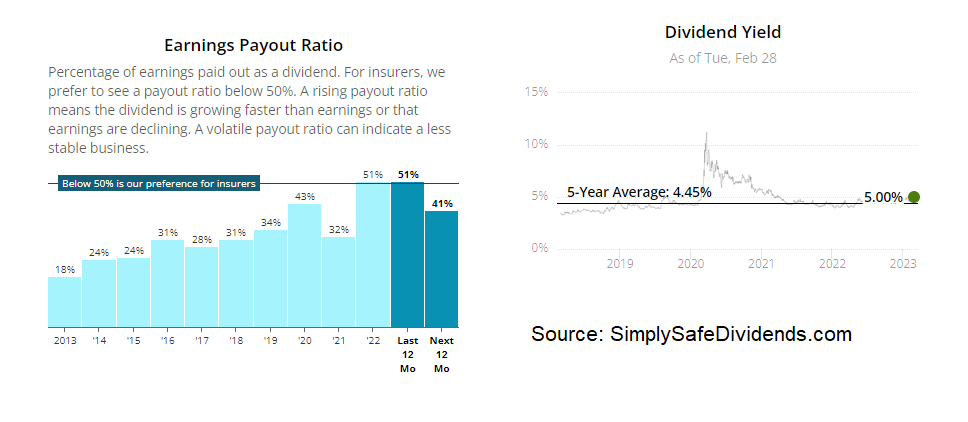

The global insurance and investment management company has now increased its dividend for 15 consecutive years. This name works really well for income-oriented dividend growth investors. That’s because the stock yields 5.1%.

That’s about three times higher than the broader market’s yield. It’s well into the territory of income vehicles, like, say, REITs. On the other hand, the last few dividend raises have been in this mid-single-digit range. And that’s a pretty reasonable expectation on a go-forward basis. The payout ratio is 52.9%, based on FY 2022 adjusted EPS, indicating more of the status quo.

To my eye, this stock looks fairly valued. We put out a full analysis and valuation video on the business back in late October, where the estimate of intrinsic value came out to $102.60/share. Notably, my dividend discount model analysis in that video estimated a long-term dividend growth rate of 5%, so we’re roughly on pace here.

To my eye, this stock looks fairly valued. We put out a full analysis and valuation video on the business back in late October, where the estimate of intrinsic value came out to $102.60/share. Notably, my dividend discount model analysis in that video estimated a long-term dividend growth rate of 5%, so we’re roughly on pace here.

With the stock currently trading hands for about $99, I think we’re basically sitting at fair value. Still, if you’re in the market for a 5%+ yield, and you’re okay with that dividend growing at a mid-single-digit rate per year, Prudential is worth a closer look.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income