Investing works a lot like most other things in life.

I mean, if you want to be truly great at anything, you surround yourself with greatness within that field.

You look for the best, cozy up to the best, and try to be the best.

That’s how it works.

Well, if you want to be a great investor, you should invest in great businesses.

It sounds simple.

That’s because it is.

Of course, simple doesn’t mean easy, and there is a bit more to it than that, but I’ve never heard of a great investor who consistently invested in lousy businesses.

So how do you identify great businesses?

Well, I think the dividend growth investing strategy funnels you right into them by default.

This strategy is all about buying and holding shares in world-class enterprises that pay reliable, rising cash dividends to shareholders.

It basically requires a business to be great in order to pay reliable, rising cash dividends to shareholders.

That’s because reliable, rising dividends must be funded by reliable, rising profits.

That’s because reliable, rising dividends must be funded by reliable, rising profits.

And you don’t produce reliable, rising profits without doing a lot of things great.

You can find hundreds of examples of these businesses by perusing the Dividend Champions, Contenders, and Challengers list.

This list contains invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I’ve been personally using this strategy for more than a decade now.

It helped me to build the FIRE Fund.

That’s my real-money portfolio, which generates enough five-figure passive dividend income for me to live off of.

I’ve actually been living off of dividends for many years.

I’ve actually been living off of dividends for many years.

I’m 40 now, but I was able to retire in my early 30s.

How?

Check out my Early Retirement Blueprint for the details.

Now, investing in great businesses is an indispensable part of becoming a great investor.

But one also must seek out great valuations.

While price is what you pay, it’s value that you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Becoming a great investor could be as simple as routinely buying high-quality dividend growth stocks when they’re undervalued.

Of course, again, simple doesn’t mean easy, and going about properly valuing businesses isn’t exactly intuitive.

But fear not.

It’a also not as difficult as you might think it is.

Fellow contributor Dave Van Knapp has made it much easier with his Lesson 11: Valuation, which is part of an overarching series of “lessons” on all aspects of dividend growth investing.

This lesson provides a valuation template that can be applied to just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Cummins Inc. (CMI)

Cummins Inc. (CMI)

Cummins Inc. (CMI) is a multinational company that designs, manufactures, and distributes engines, filtration, and power generation products.

Founded in 1919, Cummins is now a $36 billion (by market cap) manufacturing giant that employs nearly 74,000 people.

The company reports results across five business segments: Distribution, 32% of FY 2022 sales; Engine, 29%; Components, 28%; Power Systems, 11%; New Power, less than 1%.

The company makes money by manufacturing, distributing, and supplying a range of diesel and natural gas engines and related components.

Many types of vehicles use these engines.

Think heavy-duty trucks, medium-duty trucks, buses, recreational vehicles, construction machinery, agricultural machinery, and watercraft.

If that’s all there was to Cummins, you’d have a pretty good story.

However, there’s more to it than that.

Cummins is positioning itself for the future of mobility by investing in fully electric and hybrid powertrain systems, as well as hydrogen fuel cell technology.

Unfamiliar investors might assume that Cummins is just an engine company.

That’s missing the big picture.

Cummins is providing a full suite of products to cater to present and future mobility and power generation.

This distinction is important.

Everyday goods are often produced and moved around using the power generation products that Cummins manufactures and distributes.

Thus, Cummins is a vital element of the industrial backbone of the American economy.

This is why Cummins has been wildly successful for more than a century.

And with prescient preparations for the next era in mobility and power generation, Cummins may see even more success over the next century.

A more successful Cummins would result in more successful shareholders, which would partially play out through growing dividends.

Dividend Growth, Growth Rate, Payout Ratio and Yield

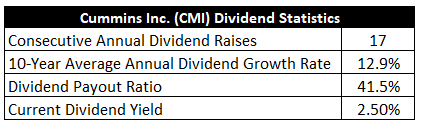

Already, Cummins has increased its dividend for 17 consecutive years.

The 10-year dividend growth rate of 12.9% is very solid, although more recent dividend raises have been in the 8% range.

Still, I’d argue that’s enough dividend growth when you consider the stock’s yield of 2.5%.

Still, I’d argue that’s enough dividend growth when you consider the stock’s yield of 2.5%.

While that yield beats what the broader market offers, it does slightly trail its own five-year average.

However, there’s a case to be made that the yield was, at times, surprisingly high for a world-class manufacturer.

The payout ratio of 41.5% shows us a healthy dividend poised for much more growth ahead.

I like dividend growth stocks in what I call the “sweet spot” – a yield of between 2.5% and 3.5%, paired with a high-single-digit (or higher) dividend growth rate.

The yield is at the low end of the range, but the dividend growth rate is dead on.

We’re looking at a really solid dividend package here.

Revenue and Earnings Growth

As solid as this package may be, it’s largely a backward-looking package.

But investors must invest in the future, not the past, and risk today’s capital for tomorrow’s rewards.

That’s precisely why I’ll now build out a forward-looking growth trajectory for the business, which will later be instrumental during the valuation process.

I’ll first show you what the top-line and bottom-line growth over the last decade looks like.

And I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past against a future forecast in this way should give us plenty of insight into where the business might be going from here.

Cummins moved its revenue from $17.3 billion in FY 2013 to $28.1 billion in FY 2022.

That’s a compound annual growth rate of 5.5%.

I like to see at least mid-single-digit top-line growth from a mature business like this.

Cummins delivered.

Meanwhile, earnings per share grew from $7.91 to $15.12 over this period, which is a CAGR of 7.5%.

Good stuff.

Excess bottom-line growth was mostly created through consistent buybacks – the outstanding share count is down by approximately 24% over the last 10 years.

Looking forward, CFRA believes that Cummins will compound its EPS at an annual rate of 8% over the next three years.

I like and concur with this forecast.

It’s a safe call – a bet on the status quo continuing – in line with what Cummins has done over the last decade.

In my view, an investment in Cummins is a long-term bet on mobility.

What I think is especially compelling about Cummins in this regard is the adaptation that’s underway: Cummins has a strong legacy business that’s also being positioned for the future of mobility.

Cummins has long been a go-to diesel engine brand, but it’s staking its future on being the go-to all-encompassing brand for mobility and power generation.

CFRA sums it up well with this passage: “Other positive trends we forecast for [Cummins] include trucking firms seeking relief from high fuel prices with more efficient engines, and a more dispersed population in the remote work era leading to truck freight covering greater distances. We think increasing anti-carbon regulation will also be a driver for [Cummins’] nascent New Power segment. We see these drivers allowing for [Cummins’] 2024 sales to grow 20% vs. 2022.”

That’s the kind of growth that can get an investor pretty excited about a stodgy industrial company.

CFRA adds this: “Further, we see [Cummins’] investments in technologies to eliminate fossil fuels from trucking and power generators paying off strongly over the long term, bolstered by developed governments incentivizing carbon reduction.”

And one more note from CFRA for good measure: “Short-term cyclical risk is partially offset by a strong long-term trend in profit growth for [Cummins], which we see continuing as the world globalizes, demanding larger, more efficient truck fleets to handle its good flows, as well as more power generation equipment, which [Cummins] also sells.”

If you want the best of today’s propulsion, that’s likely Cummins.

If you want the best of tomorrow’s propulsion, that’s likely Cummins.

An 8% bottom-line growth rate would make room for a similar dividend growth rate, which is pretty much what Cummins has been delivering for several years.

I see all of this continuing for the foreseeable future.

And investors buying in today are able to start walking that future path with a 2.5% yield in their pocket.

Not a bad setup at all.

Financial Position

Moving over to the balance sheet, Cummins maintains a great financial position.

The long-term debt/equity ratio is 0.5, while the interest coverage ratio is over 15.

Profitability is strong and surprisingly consistent, as the industry is cyclical.

Over the last five years, the firm has averaged annual net margin of 8.4% and annual return on equity of 25.1%.

Cummins is a terrific industrial company, and there’s a very good chance that it’ll be even better in 10 years.

And with economies of scale, switching costs, barriers to entry, IP, R&D, technological know-how, and brand power, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

The company’s competitive situation is unique, as Cummins is often competing against some of its most important customers (such as truck manufacturers).

There’s exposure to economic cycles here.

Cummins has customer concentration risk, with the top four customers accounting for for approximately 30% of annual sales.

Since propulsion technology could change faster than Cummins can adapt to, or in a way that’s unforeseen, there’s technological risk.

Any broad changes across trucking and/or commercial transportation, in general, would impact Cummins.

I see these risks as predictable and acceptable, but the long-term upside seems more than worth the stretch to me.

That viewpoint is reinforced by what appears to be a reasonably attractive valuation…

Stock Price Valuation

The stock’s P/E ratio is sitting at 16.5.

That’s basically right in line with its own five-year average of 16.6.

Most metrics are like this right now – close to their respective recent historical averages.

It’s just that there’s a case to be made that Cummins has been routinely underappreciated.

As noted earlier, the yield is also pretty close to its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

This seems like a very fair assumption of the long-term dividend growth path for Cummins.

It’s exactly in line with the company’s own EPS CAGR over the last decade.

It’s close to, but slightly below, where the last few dividend raises have come in at.

And it’s also a hair below where CFRA sees the company’s near-term bottom-line growth at.

Plus, the payout ratio remains at a moderate level.

I feel very comfortable with this kind of expectation from Cummins over the long run, and it’s quite possible that the realized dividend growth over the coming years outpaces my number.

The DDM analysis gives me a fair value of $270.04.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I believe I put together a fair and sensible valuation model for the business, yet its shares look at least modestly undervalued against that model.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates CMI as a 3-star stock, with a fair value estimate of $256.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates CMI as a 5-star “STRONG BUY”, with a 12-month target price of $282.00.

I’m somewhere in the middle here, albeit closer to where CFRA is at. Averaging the three numbers out gives us a final valuation of $269.35, which would indicate the stock is possibly 7% undervalued.

Bottom line: Cummins Inc. (CMI) is an industrial titan that is a vital part of the American industrial backbone. Not content to rest on its laurels, the company is seeing the curve ahead and adapting for the future of mobility. With a market-beating yield, a double-digit long-term dividend growth rate, a moderate payout ratio, nearly 20 consecutive years of dividend increases, and the potential that shares are 7% undervalued, this looks like a terrific long-term investment idea for dividend growth investors.

Bottom line: Cummins Inc. (CMI) is an industrial titan that is a vital part of the American industrial backbone. Not content to rest on its laurels, the company is seeing the curve ahead and adapting for the future of mobility. With a market-beating yield, a double-digit long-term dividend growth rate, a moderate payout ratio, nearly 20 consecutive years of dividend increases, and the potential that shares are 7% undervalued, this looks like a terrific long-term investment idea for dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is CMI’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 98. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, CMI’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income