Here’s the thing about cash. It’s not productive, and it’s slowly depreciating.

Whenever I have cash, beyond what’s there to be spent, I’m immediately thinking about how I can put it to work. Because if I don’t put it to work, it’s lazy and doesn’t do anything.

Fortunately, there are opportunities abound for cash to be put to work. The market has been very volatile, and many stocks are still well off of their highs.

This is a good thing.

Price and yield are inversely correlated. All else equal, lower prices result in higher yields, which makes the dream of living off of safe, growing dividend income come true that much faster. So volatility is an ally, not an enemy. I always see short-term volatility as a long-term opportunity.

That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

All that said, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for March 2023.

Ready? Let’s dig in.

My first dividend growth stock for March 2023 is Bank of America (BAC).

Bank of America is a multinational investment bank and financial services holding company. I have two big reasons why you should consider owning a slice of Bank of America.

The first reason is right in the name of the company – it’s a bank. And a very big one, at that. Banks are literally in the business of money. Want to make money? Well, you can’t get any closer to the stuff than a bank. The second reason is that Warren Buffett – arguably the greatest investor of all time – has about $36 billion invested in the bank.

Buffett isn’t doing that unless he’s supremely confident in the long-term prospects here. And why wouldn’t he be confident? Bank of America has compounded its revenue at 0.6% and its EPS at 15.1% over the last decade. Double-digit EPS growth. Double-digit dividend growth.

Hard to afford the latter without the former. Worry not. Bank of America is delivering on both counts. The five-year DGR is 17.1%, which is outstanding.

Bank of America has increased its dividend for nine consecutive years. And since we all know that Buffett loves his growing dividends, it’s no surprise that he’s all over this one. The stock also yields 2.5%, which is pretty decent current income while you wait for those dividend raises to pile up. And with a payout ratio of only 27.6%, I expect those dividends to continue piling up very nicely.

Bank of America has increased its dividend for nine consecutive years. And since we all know that Buffett loves his growing dividends, it’s no surprise that he’s all over this one. The stock also yields 2.5%, which is pretty decent current income while you wait for those dividend raises to pile up. And with a payout ratio of only 27.6%, I expect those dividends to continue piling up very nicely.

This stock isn’t super cheap. But it’s a great business. And I think there’s mild undervaluation present.

We recently put together a full analysis and valuation video on Bank of America, estimating fair value for the business at $39.28/share. The stock is currently priced at right about $35. Huge upside? No. But you’re looking at one of the biggest and best banks in the US – one backed by Warren Buffett’s capital and reputation.

I’d rather see it cheaper, certainly. But if one is investing for the next 20 or 30 years, getting in at $34 or $35 or whatever will make almost no difference two or three decades from now. I’d definitely consider joining Buffett on this one.

My second dividend growth stock pick for March 2023 is Cummins (CMI).

Cummins is is a multinational engine, filtration, and power generation company. Narrative versus reality. This often comes up in investing. People might conjure up an image of a company that’s not at all the reality.

The narrative of Cummins is that it’s some old-school engine company. The reality is that it’s a company providing a suite of products across mobility. And that distinction is important. It’s also a big part of why the company continues to put up solid growth. A 5.5% CAGR for revenue and a 7.5% CAGR for EPS over the last decade.

You’re also getting solid dividend growth here. Cummins has increased its dividend for 17 consecutive years. The 10-year DGR is 12.9%, although more recent dividend raises have been in the high-single-digit range. Pretty close to tracking EPS growth now. And you’re pairing that kind of dividend growth with the stock’s yield of 2.4%. Not bad at all. The payout ratio of 41.5% isn’t bad, either.

You’re also getting solid dividend growth here. Cummins has increased its dividend for 17 consecutive years. The 10-year DGR is 12.9%, although more recent dividend raises have been in the high-single-digit range. Pretty close to tracking EPS growth now. And you’re pairing that kind of dividend growth with the stock’s yield of 2.4%. Not bad at all. The payout ratio of 41.5% isn’t bad, either.

What else isn’t bad? The valuation. The valuation here is undemanding pretty much right across the board. Take the P/E ratio, for example. It’s 17. Now, that is pretty much right in line with its own five-year average.

However, I’d argue that Cummins just hasn’t been properly appreciated or valued by the market for a long time now. It’s a great business that’s been often valued like a more mediocre one. I’m not saying it should command an earnings multiple of 25 or anything, but a market multiple doesn’t seem egregious.

We’ll be putting out a full analysis and valuation video on Cummins soon, which will show why this American industrial titan looks at least modestly undervalued. Keep an eye out for that video. And keep Cummins on your radar.

My third dividend growth stock pick for March 2023 is CubeSmart (CUBE).

CubeSmart is a real estate investment trust focused on self-storage properties. Self-storage is a fantastic area of real estate. Low startup costs. Low fixed costs. Minimal employee needs. A sticky customer base on short, recurring, flexible leases.

There’s a lot of money to be made here. And that’s exactly what CubeSmart has been doing. We’re talking a tripling of revenue over the last decade and a 12.4% CAGR for AFFO/share over the last decade.

There’s a lot of money to be made here. And that’s exactly what CubeSmart has been doing. We’re talking a tripling of revenue over the last decade and a 12.4% CAGR for AFFO/share over the last decade.

With that kind of underlying business growth, you already know what the dividend growth is gonna look like. Yep. It looks spectacular.

The REIT has increased its dividend for 13 consecutive years, with a 10-year DGR of 18.3%. Wow. Plus, the stock offers a yield of 4.3%. How often do you see a 4%+ yield paired with that kind of dividend growth? Almost never. CubeSmart is guiding for $2.51 at the midpoint in AFFO/share for FY 2022, putting the payout ratio at 78.1%. A touch high. But not concerning.

Also unconcerning is the valuation, especially for the quality and growth. Using that aforementioned guidance, you’re looking at a forward price-to-adjusted-funds-from-operations ratio of 18.1.

Seeing as how that’s fairly analogous to a P/E ratio on a normal stock, I think that’s pretty compelling. I mean, this is a high-growth, high-yield REIT with an investment-grade credit rating that has run circles around the S&P 500 over the last decade. When you get yield, growth, and performance like this, I’d expect to pay up. But it’s not even necessary here. If you’re smart, you won’t underestimate CubeSmart.

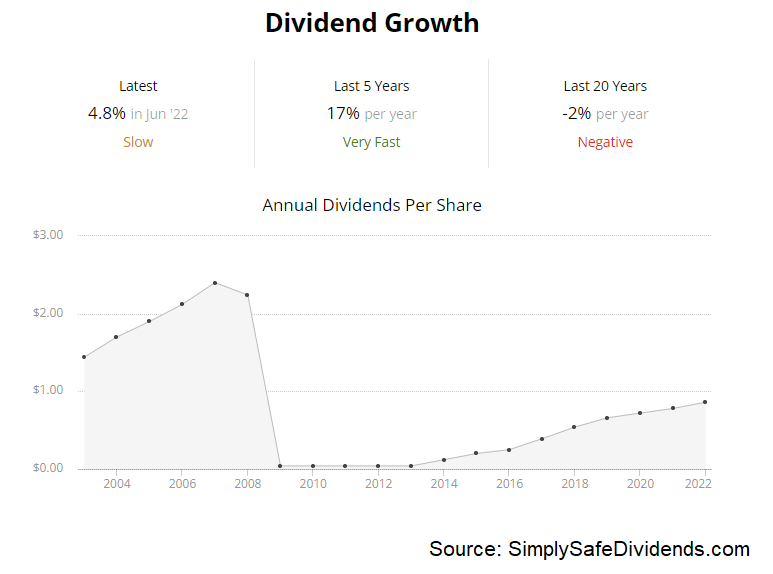

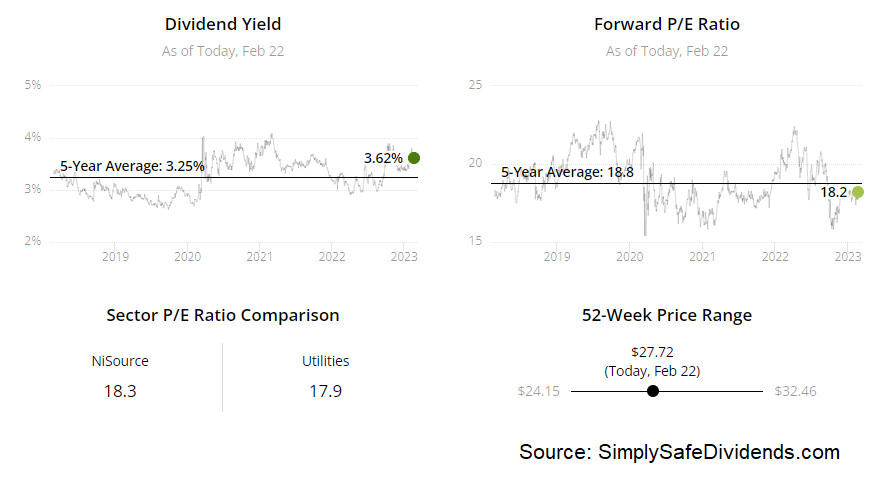

My fourth dividend growth stock pick for March 2023 is NiSource (NI).

NiSource is a fully regulated US utility company. NiSource provides electric and natural gas utilities. They serve millions of customers across six US States. Utilities are fertile ground for dividend growth investors.

Why? Because utilities are providing services that people quite literally can’t live without in a modern-day society. Try living without electricity for a day or two. Almost can’t do it. When you’re providing this kind of necessity, the money flows in. Of course, regulation caps the upside. But the downside is very limited, too. Speaking of a narrow range, revenue and EPS for NiSource has been basically flat over the last decade. But the good news is, there’s a big acceleration in business growth underway here.

That acceleration in business growth bodes well for dividend growth. Already, NiSource has increased its dividend for 12 consecutive years. The 10-year DGR is 9.8%, which is strong enough, although more recent dividend raises have been in the 6% to 7% range.

Still, that’s enough to get the job done when you see the stock’s yield of 3.7%. And that’s before factoring in the acceleration set to play out. Plus, the payout ratio is 69%, based on adjusted EPS guidance at the midpoint for FY 2022. That’s quite reasonable for a utility.

This strikes me as a suitable idea for a defensive investor looking to sleep well at night. It’s not the cheapest stock. It doesn’t offer the highest yield or the highest growth rate. Instead, I just see a nice balance across the board. And you’re talking about a business model that is very stable and defensive.

Meantime, the valuation that’s in place is reflecting the NiSource that’s grown at a slower rate, not the NiSource that could be growing a lot faster over the coming years. We’ll have a full analysis and valuation video coming out soon on this utility, and that video will show why the business is potentially worth just over $31/share. The stock is currently priced at about $27. Not a bad spread there.

Meantime, the valuation that’s in place is reflecting the NiSource that’s grown at a slower rate, not the NiSource that could be growing a lot faster over the coming years. We’ll have a full analysis and valuation video coming out soon on this utility, and that video will show why the business is potentially worth just over $31/share. The stock is currently priced at about $27. Not a bad spread there.

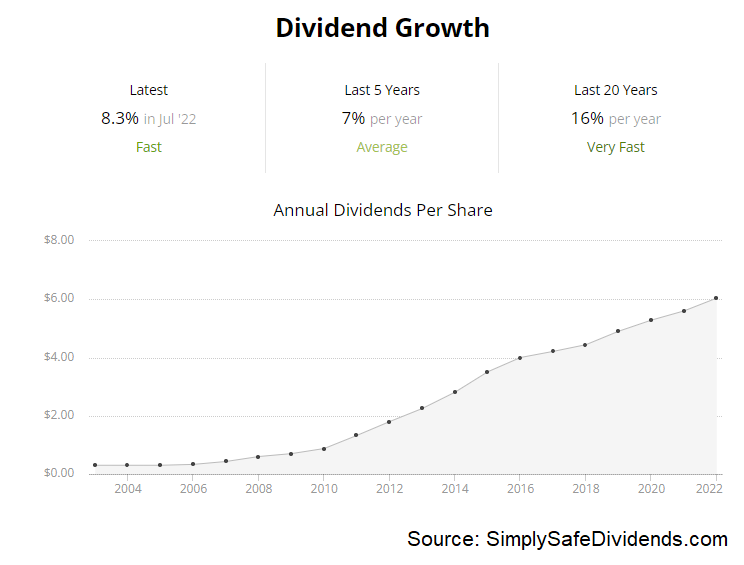

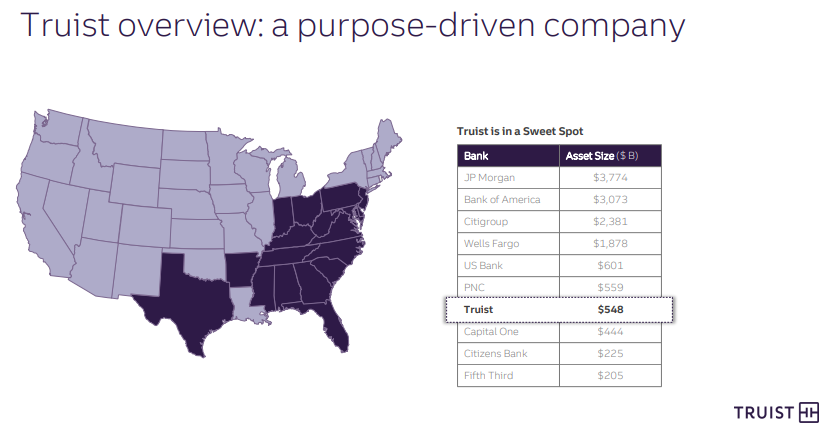

My fifth dividend growth stock pick for March 2023 is Truist Financial (TFC).

Truist is an American bank holding company. This is one of the largest commercial banks in the US. As I noted earlier, the banking business model is one of my favorite business models. But there are two things that differentiate Truist.

First, their geographic footprint – Truist is mostly focused on the Southeastern US. Their biggest market by deposits is Florida, which is one of the fastest-growing states in the US. Second, they have a fairly significant insurance brokerage business housed inside of the company. I think those two factors have helped growth. Truist has compounded its revenue at an annual rate of 10.6% and its EPS at an annual rate of 8.1% over the last decade.

First, their geographic footprint – Truist is mostly focused on the Southeastern US. Their biggest market by deposits is Florida, which is one of the fastest-growing states in the US. Second, they have a fairly significant insurance brokerage business housed inside of the company. I think those two factors have helped growth. Truist has compounded its revenue at an annual rate of 10.6% and its EPS at an annual rate of 8.1% over the last decade.

These dividend metrics are great. Check it out. The bank has increased its dividend for 12 consecutive years, with a 10-year DGR of 10.2%.

Along with that double-digit dividend growth, the stock offers a market-smashing 4.3% yield. That yield is in REIT territory. Wow. It’s not often you see a 4%+ yield and a 10%+ dividend growth rate paired together. And the payout ratio is a very healthy 47%, indicating a dividend that’s almost certainly headed a lot higher.

Along with that double-digit dividend growth, the stock offers a market-smashing 4.3% yield. That yield is in REIT territory. Wow. It’s not often you see a 4%+ yield and a 10%+ dividend growth rate paired together. And the payout ratio is a very healthy 47%, indicating a dividend that’s almost certainly headed a lot higher.

Truist flies under the radar. Despite the growth, the stock looks cheap. The P/E ratio is 11. That puts the PEG ratio at a bit over 1, based on the strong bottom-line growth rate. The P/B ratio is 1.2, which is on the low end for a quality bank like this.

In my view, Truist is low-hanging fruit. You get a nice yield, strong growth, and differentiating factors that set the bank up really well. And all of that comes in a package that looks reasonably valued. We’ll soon have a full video coming out that will analyze and value the bank, and that video will show why the estimate for intrinsic value comes out to slightly under $53/share.

The stock’s current pricing of $48 means there’s some decent upside. And you collect a 4%+ yield while you wait. If Truist isn’t on already on your shopping list, it should be.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income