Is 2023 gonna be the mirror opposite of 2022?

Backing up a bit, 2022 was one of the worst years ever for the market. It’s pretty rare to have even one year like that.

Two in a row? Almost unheard of. And so it’s not a total surprise to see 2023 start off with a rebound.

Indeed, the S&P 500 is up by 7% YTD. We’re not even two months into this thing.

Too late to buy the crash? I don’t think so. A lot of individual stocks are still down significantly. And if you’re young and still actively accumulating assets, that’s good news.

See, price and yield are inversely correlated. All else equal, lower prices result in higher yields.If your dream, like my dream, is to live off of dividend income, this helps to make the dream come true even faster.

Today, I want to tell you about five dividend growth stocks that are down more than 20% from their recent highs.

Ready? Let’s dig in.

The first dividend growth stock I want to highlight today is Bank of America (BAC).

Bank of America is a multinational investment bank and financial services holding company with a market cap of $285 billion.

I’m a big fan of the banking business model. Banks are literally in the business of money. If you want to make lots of money, money itself is probably a pretty good spot to be in. You know who else is a big fan of this business model? Warren Buffett. Not just that but he’s a big fan of this bank, in particular.

In the $340 billion common stock portfolio he oversees for his conglomerate Berkshire Hathaway Inc. – stock ticker BRK.B – Bank of America represents a $36 billion investment, which is the second-largest investment in the entire portfolio. That confidence is, I’m sure, based on the quality and growth of this bank. That quality and growth, by the way, extends over to the dividend.

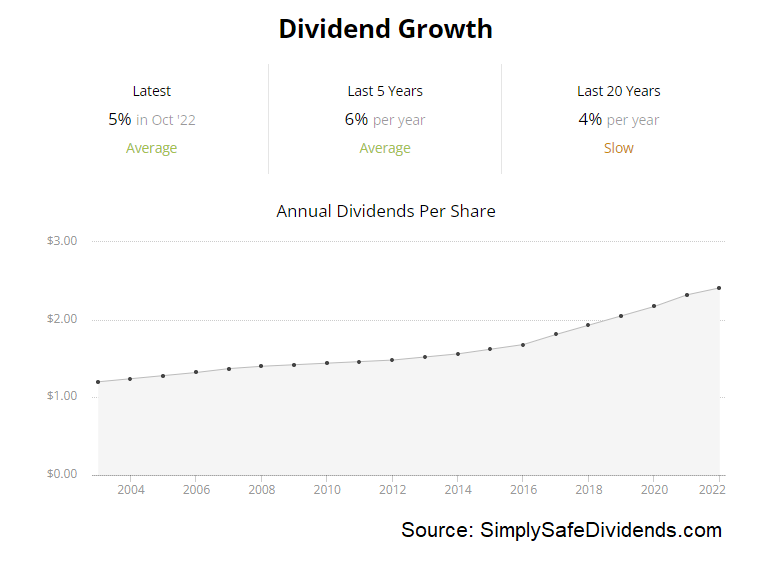

The bank has increased its dividend for nine consecutive years. Bank of America, like a lot of other banks, was disproportionately affected by the GFC, so its relatively short dividend growth track record belies its true potential.

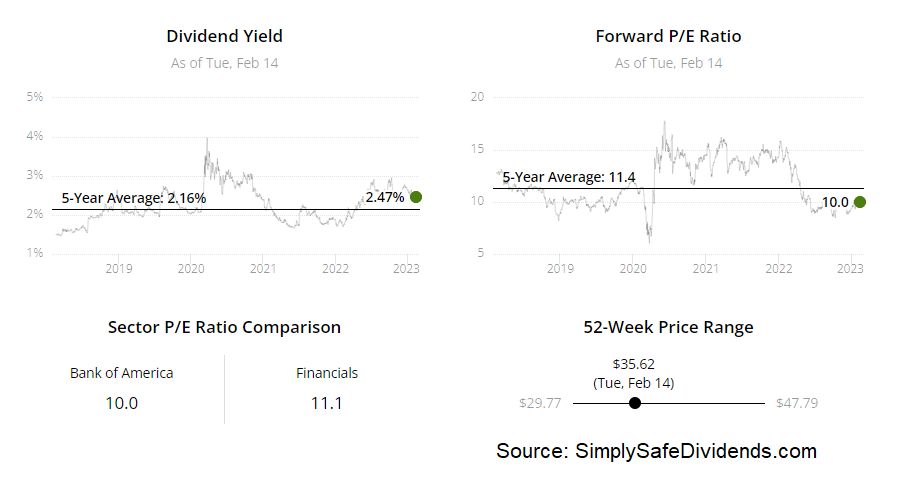

But the bank is making up for lost ground – the five-year dividend growth rate is a stout 17.1%. And you’re pairing that double-digit dividend growth with the stock’s market-beating yield of 2.5%. With a payout ratio of only 27.6%, this is a healthy, well-covered dividend.

This stock’s gotten pretty beat up. It’s down 28% from its 52-week high. And I think that’s an opportunity.

The stock’s current pricing of about $35.50 is well off of the 52-week high of $49.44. This is one of America’s biggest and best banks. Warren Buffett has staked a good chunk of his capital, as well as his reputation, on it. Could it go wrong? Sure. Anything can happen. But it does skew in the favor of the long-term investor.

The stock’s current pricing of about $35.50 is well off of the 52-week high of $49.44. This is one of America’s biggest and best banks. Warren Buffett has staked a good chunk of his capital, as well as his reputation, on it. Could it go wrong? Sure. Anything can happen. But it does skew in the favor of the long-term investor.

That viewpoint is, of course, reinforced by what I see as an attractive valuation. Soon, a full analysis video and valuation piece on Bank of America should be live. In that video, I show why the bank could be worth $39.28/share. Very decent upside potential on a Buffett-backed bank. Take a look.

The next dividend growth stock I want to quickly bring to your attention is Black Hills (BKH).

Black Hills is an electric and gas utility company with a market cap of $4 billion. Black Hills doesn’t get a lot of love or press, but maybe it should? Well, I’m doing my best to change that, covering it for you today. Why am I covering it?

It’s a very stable operation in the business of selling something that practically sells itself – reliable energy. If you want the lights to actually turn on when you flick the switch, you’ll need the kind of service that Black Hills provides to its customers across eight different US states. That’s why it’s been able to increase its revenue, profit, and dividend like clockwork.

This utility has increased its dividend for 52 consecutive years. Wow. A Dividend King. Like I said, this is a business that should probably get more attention than it does. There simply aren’t that many companies out there that have been able to manage this kind of track record, even in the utility space.

This utility has increased its dividend for 52 consecutive years. Wow. A Dividend King. Like I said, this is a business that should probably get more attention than it does. There simply aren’t that many companies out there that have been able to manage this kind of track record, even in the utility space.

Now, the 10-year DGR of 5% isn’t huge, but in normal, non-inflationary times, it’s pretty decent growth. However, this is more of an income play. And with a yield of 3.9%, it does get the income job done pretty well. Meantime, based on midpoint FY 2023 EPS guidance, the payout ratio is 66.7%. That’s not a high payout ratio at all for a utility like this. I see the impressively long dividend growth track record set to continue getting longer.

This stock got hammered on reduced guidance for FY 2023. It’s now down 21% from its 52-week high.

The 52-week high of $80.95 is gone. The stock is now priced at about $64. So what happened? Black Hills surprised the market by revising FY 2023 EPS guidance to be in the range of $3.65 to $3.85, down from $4.00 to $4.20 previously. Great? No. Terrible? Not really.

The business is still making plenty of money. Just not as much as was anticipated before. Meanwhile, it’s a Dividend King offering a near-4% yield. I think you can do much worse than that. The drop has created a more favorable valuation, with the P/E ratio of 16.1 being quite a bit below its own five-year average of 17.5. At the 52-week high, it looked expensive. But down here, near the 52-week low, it looks interesting.

Next up, let’s quickly discuss CME Group (CME).

CME Group is a global markets company with a market cap of $66 billion. This is a money machine. It runs the world’s largest financial derivatives exchange. Companies that own exchanges have miniature financial monopolies, as certain financial products can only be purchased on certain exchanges.

We’re talking about sky-high margins and durable competitive advantages. That’s probably why this company, which has roots dating back to 1848, has shown an ability to endure for nearly two centuries. You know what else is enduring? The dividend.

The financial markets company has increased its dividend for 12 consecutive years. A great business that has roots dating back more than two centuries, yet we’ve only got 12 consecutive years of dividend increases?

Well, a couple of things to keep in mind. CME Group, as it exists today, was formed in 2006 after a major merger. Second, the GFC occurred not long after the big merger. And the company decided to hold the dividend static for a period of time in order to err on the side of caution. I don’t hold that against them too much.

Well, a couple of things to keep in mind. CME Group, as it exists today, was formed in 2006 after a major merger. Second, the GFC occurred not long after the big merger. And the company decided to hold the dividend static for a period of time in order to err on the side of caution. I don’t hold that against them too much.

With a 10-year DGR of 8.4%, a yield of 2.4%, and a payout ratio of 59.4%, we’ve got solid dividend metrics across the board. But it gets better, because CME Group regularly declares special dividends. And they tend to be sizable. The last one was $4.50/share. That pretty much doubles the dividend and yield. Good stuff.

This stock’s 27% drop from its 52-week high looks overdone to me. I really like CME Group. In fact, I like it so much, I picked it as one of my top five dividend growth stocks for 2023. How are things going? Well, CME Group printed a solid Q4 report in early February, showing 15.7% YOY adjusted EPS growth.

Oh, and the company raised the dividend by 10% in early February. At the 52-week high of $251.99, the stock wasn’t on my radar. But down here around the $184 area? It’s very much on my radar. By the way, despite that difference, the stock is up by 9% on the year already.

Will it continue to beat the market all year? I don’t know. But I do know it’s a great business. And the valuation is reasonable. The P/E ratio of 24.9, for example, compares quite favorably to its own five-year average of 27.9. Don’t forget about CME Group.

The fourth dividend growth stock I need to bring to your attention is McCormick & Company (MKC).

McCormick is a spice and seasoning company with a market cap of $20 billion. McCormick often gets overshadowed by a range of other food companies. Truth be told, though, there really is no rival to McCormick. It’s the spice and seasoning company.

If you research spices, you’ll see a crazy and fascinating history here. I mean, wars used to be fought over spices. We can now just go down to the grocery store and buy what we need. Despite the economics around spices being far different than they were a few hundred years ago, there’s still a lot of money to be made in spices. And lots of money drops down into lots of dividends. Growing dividends.

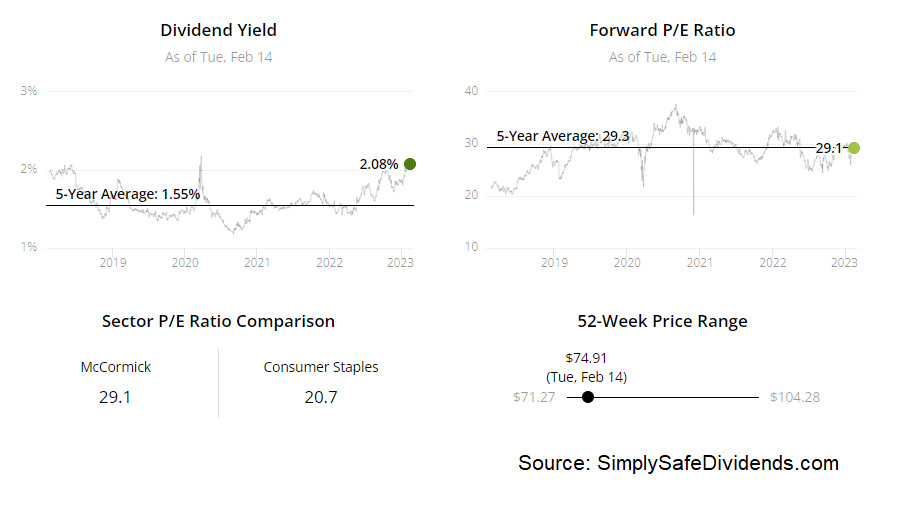

The spice company has increased its dividend for 36 consecutive years. Yep. This is an esteemed Dividend Aristocrat. The 10-year DGR is 9.1%. And until recently, with the pandemic and all, they’ve been remarkably consistent with that kind of dividend growth.

The flip side is the yield – at 2.1%, there’s something to be desired there. That said, this is 60 basis points higher than its own five-year average. That’s quite a spread. A 2.1% yield could be considered low, sure, but this is a stock that has typically yielded much less. The payout ratio is 63.9%, based on midpoint guidance for FY 2023 EPS. A touch high. I’d prefer to see it lower. But it’s not concerning. And it’s high because of temporary hits to EPS.

This Dividend Aristocrat is 30% off of its 52-week high. Wow. You simply do not often see McCormick drop like this. Rare to see a Dividend Aristocrat of this caliber stumble like this.

The 52-week high is $107.35. The stock’s current pricing is around $75.50. Now, this is a case where I don’t think the prior high was warranted. The stock probably shouldn’t have been priced at $107 in the first place. It looked extremely overvalued there. But, now, at around $75.50, I think the valuation has come down to a sensible level. Cheap? No. But sensible.

The 52-week high is $107.35. The stock’s current pricing is around $75.50. Now, this is a case where I don’t think the prior high was warranted. The stock probably shouldn’t have been priced at $107 in the first place. It looked extremely overvalued there. But, now, at around $75.50, I think the valuation has come down to a sensible level. Cheap? No. But sensible.

The P/E ratio is 30. That’s almost precisely in line with its own five-year average of 29.3. And, again, the business is under-earning right now. So I think it’s better than it looks. I wouldn’t back up the truck here, but McCormick is a jewel of a business and worth at least taking a look at after the fall.

Last but not least, let’s cover Prologis (PLD).

Prologis is an industrial real estate investment trust with a market cap of $119 billion. This is the largest industrial REIT in the world. Nearly 5,500 buildings across the portfolio racking up 1.2 billion square feet. None are bigger than Prologis. And you could very well argue that none are better.

Certain areas of real estate are struggling. Office would be a prime example. And shopping malls aren’t exactly lighting the world on fire. But the industrial side of real estate, because of the growing need for logistics, is doing very well. That obviously bodes well for Prologis and its ability to drive higher profits and grow its dividend.

The industrial REIT has increased its dividend for nine consecutive years. Prologis is off to a good start here. The five-year DGR is 12.4%. And you’re able to pair that double-digit dividend growth rate with the stock’s yield of 2.4%. That is an awfully compelling combination.

It’s not every day that you see a dividend growth rate that like that fused to a yield like this. You usually have to give up one to get the other. And with a payout ratio of 58%, based on midpoint Core FFO/share guidance for FY 2023, this dividend is likely to continue growing at a rapid clip.

The stock’s 26% drop from its 52-week high seems mostly warranted, and the valuation looks fair once again. I think the market got carried away with enthusiasm over Prologis when it sent the stock screaming up to its 52-week high of $174.54.

The stock’s 26% drop from its 52-week high seems mostly warranted, and the valuation looks fair once again. I think the market got carried away with enthusiasm over Prologis when it sent the stock screaming up to its 52-week high of $174.54.

However, what the market giveth, the market taketh away. And the stock is now priced at $129, as I write this. What this reversal in enthusiasm and pricing has done is, it’s also created a reversal in valuation. And that valuation looks fair again, which is about as much as you can ask for with a REIT of this quality.

Based on that aforementioned guidance, the forward price-to-core-funds-from-operations-per-share ratio is 23.7. In my view, that’s right about where it oughta be. Another way to look at it? The P/CF ratio of 27.7 lines up pretty well against its own five-year average of 27.5. The stock has had a recent bounce, but I think it’s still buyable for long-term dividend growth investors.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income