There are a lot of differences between speculation and investing.

Speculation is more akin to pure gambling.

Investing is making informed decisions based on a rational interpretation of facts and circumstances.

These two concepts involve totally different risk profiles.

Whereas speculation is usually pinned on hopes and dreams, investors tend to allocate capital toward real businesses providing real products and/or services.

And providing real products and/or services often results producing real profits.

A lot of profits.

Providing real products and/or services, to more people, at higher prices?

That’s when you can end up with growing profits.

And growing profits are fertile ground for growing dividends.

This basic logic is at the heart of dividend growth investing.

This strategy is all about investing in high-quality businesses paying reliable, rising dividends to shareholders.

Want examples?

Want examples?

You can find hundreds by perusing the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I’ve been personally using this strategy for more than 10 years now, and it’s been positively transformational.

It’s helped me to build the FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

I’ve actually been living off of dividends for years.

I quit my job and retired in my early 30s.

I quit my job and retired in my early 30s.

I share in my Early Retirement Blueprint how I did that… and how you can, too.

Following the dividend growth investing strategy has been instrumental to my success.

But one can’t buy stocks blindly.

Valuation at the time of investment is critical.

Price is what you pay, but value is what you end up getting.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Avoiding speculation in favor of investing, and properly using dividend growth investing and valuation to your advantage, is nearly a surefire way to build significant and lasting wealth and passive income over the long run.

Now, doing this does require one to first have a basic understanding of valuation.

Fear not.

It’s not as difficult as you might think.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to greatly demystify the valuation process.

Part of an overarching series of “lessons” on dividend growth investing, it provides a valuation template that can be used on just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

NiSource Inc. (NI)

NiSource Inc. (NI)

NiSource Inc. (NI) is a fully regulated US utility company.

Founded in 1847, NiSource is now an $11 billion (by market cap) utility giant that employs over 7,000 people.

NiSource serves approximately 3.7 million natural gas customers and 500,000 electric customers across six states through its local Columbia Gas and NIPSCO brands.

The company reports results across the following two segments: Gas Distribution Operations, 65% of FY 2021 revenue; and Electric Operations, 35%.

What we have here is your basic regulated utility.

A utility benefits from providing a service (energy) that people quite literally cannot live without in a modern-day society.

That benefit is further reinforced by the fact that utilities are usually running local monopolies, where they are the only company providing the energy for a specific service area.

Having a captive customer base like this is obviously extremely advantageous to the business and its shareholders.

However, a utility is heavily regulated by the government in order to curtail just how advantageous this situation can be, in order to prevent a company from taking advantage of customers.

This ends up putting a limit on just how profitable the company can be.

It’s like a Ferrari that has a speed limiter installed.

The speed is capped, but it’s still a Ferrari.

Likewise, a utility business has its profit and upside capped, but there’s still plenty of money to be made from a service that sells itself.

Much of that money comes in the form of a large, growing dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

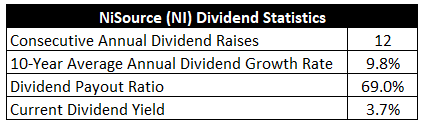

Indeed, NiSource has increased its dividend for 12 consecutive years.

The 10-year dividend growth rate is 9.8%, which is quite impressive for a utility.

However, more recent dividend raises have been in the 6%-7% range.

But I’d argue that’s really quite enough dividend growth when you consider the stock’s market-beating yield of 3.7%.

This yield, by the way, is 50 basis points higher than its own five-year average.

This yield, by the way, is 50 basis points higher than its own five-year average.

With the payout ratio at 69%, based on adjusted EPS guidance at the midpoint for FY 2022, this is a well-covered dividend.

I like dividend growth stocks in what I call the “sweet spot” – a yield of between 2.5% and 3.5%, paired with a high-single-digit (or higher) dividend growth rate.

This stock offers a relatively high yield, and yet you don’t have to sacrifice dividend growth on the other side of the coin.

These dividend metrics are very good and balanced.

Revenue and Earnings Growth

As good and balanced as they may be, they’re largely looking at what’s already transpired.

But investors must face the reality that they’re risking today’s capital for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will later be instrumental during the valuation process.

I’ll first show you what this company has done over the last decade in terms of top-line and bottom-line growth.

I’ll then divulge a professional prognostication for near-term profit growth.

Lining up the proven past against a future forecast in this way should give us what we need to design an extrapolation of what the future growth path might look like.

NiSource has seen its revenue go from $5 billion in FY 2012 to $4.9 billion in FY 2021.

Essentially flat.

Utilities tend to not grow very quickly, but I’d really like to see something better than a flatline here.

Meanwhile, earnings per share moved from $1.39 to $1.37 (adjusted) over this period.

Again, pretty much flat.

Based on these numbers only, this utility isn’t an exciting investment idea at all.

After all, who wants to invest in a business that isn’t growing?

Well, here’s the thing: We invest in where a business is going, not where it’s been.

In this regard, NiSource is a lot more interesting.

Looking forward, CFRA is projecting an 8% CAGR in EPS over the next three years for NiSource.

That’s a bit more like it.

I think CFRA sums up the thesis best with this passage: “We expect adjusted EPS growth near 5.8% in 2022 and 6.9% in 2023, followed by near 9.7% growth in 2024, accelerated by $2 [billion] in planned renewable spending from 2022 to 2024. We look favorably upon [NiSource’s] progress in accelerating renewable energy investments in Indiana, with 11 new projects across wind, solar, and storage expected between 2023 and 2025, as well as its commitment of exiting coal generation in the state by 2028. The company recently formalized its net zero emissions goal of 2040, ahead of many utility peers.”

CFRA’s view is backed by NiSource’s own guidance for FY 2022 that came out earlier in the year: “Non-GAAP diluted net operating earnings per share are expected to grow by 7 to 9 percent, from 2021’s full year results of $1.37 through 2024, on a compound annual growth rate basis, including near-term annual growth of 5 to 7 percent through 2023.”

If we look at more recent numbers, NiSource narrowed its adjusted EPS guidance for FY 2022 in the Q3 earnings print to $1.45 at the midpoint.

That would represent 5.8% YOY growth.

This is almost right in the middle of the 6%-8% near-term growth the company was guiding for at the outset of the year.

I’m willing to take these projections at face value, as NiSource has been making good on them thus far.

And this kind of underlying EPS growth would set the foundation for like dividend growth.

That is, we’re likely looking at mid-to-high-single-digit annual dividend growth over the foreseeable future.

Meantime, you’re starting off with a near-4% yield.

It’s not setting the world on fire, but it is a fairly large dividend growing at a nice clip.

And this is all coming from a very stable, predictable business.

Frankly, one could do a lot worse than that.

Financial Position

Moving over to the balance sheet, NiSource has a good financial position that’s fairly standard for a utility.

The long-term debt/equity ratio is 1.3, while the interest coverage ratio is just over 3.

Profitability is also par for the course.

Over the last five years, the firm has averaged annual net margin of 4.1% and annual return on equity of 4.2%.

These numbers do belie the true profitability of the business, as FY 2020 negatively and artificially skews things.

Net margin for the most recent fiscal year came in at 12.1%.

Overall, I think NiSource is a pretty good utility business that’s about to look even better.

And with economies of scale, a geographic monopoly, and a regulatory structure that nearly guarantees some level of profit, the company is protected by durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Regulation is a double-edged sword.

Regulators allow for utilities to make a reasonable profit, factoring in CapEx, which puts a profit floor under the business.

However, there’s also a ceiling, as regulators will limit the rates a utility can charge (in order to protect customers from getting fleeced).

Since a geographic monopoly is often in place, competition in the traditional sense is usually non-existent.

But customers could become competition in the future through the generation of power at the site of consumption (e.g., solar panels and batteries).

Because a utility lacks the ability to expand the service area very much, a utility has their fate largely tied to the geographic area they serve.

Rising interest rates are a two-pronged risk – rising rates cause higher interest expenses for the business, and the stock and its yield can also look less attractive on a relative basis.

I also see black swan risk here, primarily via explosions and natural disasters.

This is a solid, unassuming utility that could be nearing a serious acceleration in growth.

And with the stock down nearly 20% from its 52-week high, the valuation is also unassuming…

Stock Price Valuation

The stock’s P/E ratio is 18.5, based on midpoint adjusted EPS guidance for FY 2022.

I think that’s quite a sensible, even modest, earnings multiple for a staid utility that could soon become much less staid.

Now, the stock’s own five-year average P/E ratio is being skewed by the same FY 2020 that affects profitability metrics.

However, a lot of utilities that I track are commanding earnings multiples of around 20.

The P/CF ratio of 8.9 is below its own five-year average of 10.1.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 6.5%.

I’m basically extrapolating out recent dividend raises.

And that extrapolation is supported by the moderate payout ratio and anticipation for higher EPS growth over the near term.

If NiSource can deliver this kind of dividend growth with recent business growth, they can certainly do it with even better business growth in the years ahead.

The DDM analysis gives me a fair value of $30.43.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

My expectations are pretty modest, yet the stock still comes out looking undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates NI as a 4-star stock, with a fair value estimate of $32.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates NI as a 4-star “BUY”, with a 12-month target price of $31.00.

I did come out low, but we have a reasonably tight consensus here. Averaging the three numbers out gives us a final valuation of $31.14, which would indicate the stock is possibly 14% undervalued.

Bottom line: NiSource Inc. (NI) is a solid utility selling a service that people can’t live without. Recent growth isn’t super impressive, but the anticipated acceleration in growth is. And we always invest in where a business is going, not where it’s been. With a market-beating yield, inflation-beating dividend growth, a moderate payout ratio, 12 consecutive years of dividend increases, and the potential that shares are 14% undervalued, income-oriented dividend growth investors could have a strong long-term opportunity on their hands.

Bottom line: NiSource Inc. (NI) is a solid utility selling a service that people can’t live without. Recent growth isn’t super impressive, but the anticipated acceleration in growth is. And we always invest in where a business is going, not where it’s been. With a market-beating yield, inflation-beating dividend growth, a moderate payout ratio, 12 consecutive years of dividend increases, and the potential that shares are 14% undervalued, income-oriented dividend growth investors could have a strong long-term opportunity on their hands.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is NI’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 31. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, NI’s dividend appears Unsafe with a heightened risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income