Being inspired by the masters of any given field is a great way to get started in that field.

For instance, I’ve personally found great inspiration from Warren Buffett in investing.

I’ve followed in his footsteps in many ways, in both life and investing.

When it comes to investing, I realized something pretty early on about Buffett.

![]() That realization is that he apparently loves high-quality dividend growth stocks.

That realization is that he apparently loves high-quality dividend growth stocks.

If you look at the common stock portfolio he oversees, it’s filled with these stocks.

First, what are these stocks?

Well, they represent equity in world-class businesses that pay reliable, rising dividends to their shareholders.

You can find many, many examples of these stocks by perusing the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Simply put, these are some of the best stocks in the world.

Simply put, these are some of the best stocks in the world.

That’s because they’re ownership slices of some of the best businesses in the world.

Now, I can understand that some people find it hard to relate to a billionaire.

But you can always scale things down in order to suit your own needs.

That’s what I’ve done as I’ve built out my own portfolio, which I call the FIRE Fund.

This real-money portfolio produces enough five-figure passive dividend income for me to live off of.

Indeed, I do live off of dividends.

Been doing so for years.

Been doing so for years.

I actually retired in my early 30s, thanks largely to dividends.

And I share in my Early Retirement Blueprint exactly how I was able to retire so early in life.

Of course, a key pillar to the Blueprint is the kind of stocks I’ve been buying.

But it’s also been about when and at what valuations I’ve been buying them at.

Whereas price is what you pay, value is what you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Following in the footsteps of many great investors by buying high-quality dividend growth stocks when they’re undervalued can serve you extremely well over the long run.

Of course, doing so does first require one to have a basic understanding of valuation.

But this isn’t as difficult as you might think.

My colleague Dave Van Knapp made it far easier with Lesson 11: Valuation.

A component of his overarching series of “lessons” designed to teach the ins and outs of dividend growth investing, it explicitly lays out a simple-to-follow valuation system that can be used on almost any dividend growth stock.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Bank of America Corp. (BAC)

Bank of America Corp. (BAC)

Bank of America Corp. (BAC) is a multinational investment bank and financial services holding company.

Founded in 1784, Bank of America is now a $284 billion (by market cap) banking behemoth that employs almost 220,000 people.

Operating as the second-largest American money center bank by assets, Bank of America has approximately 4,000 branches across the US (with representation in all 50 states).

Bank of America also has significant international exposure, with a global footprint that extends across 35 countries.

The bank reports results across the following four business segments: Consumer Banking, 46% of FY 2022 net income; Global Banking, 32%; Global Wealth and Investment Management, 15%; and Global Markets, 6%.

There’s a big reason why Warren Buffett is heavily invested in Bank of America.

With a market value of nearly $36 billion, Bank of America represents the second-largest position in the common stock portfolio that Buffett oversees for Berkshire Hathaway Inc. (BRK.B).

That reason?

The “float”.

The core banking business model is one where money is made from money.

And not just money but other people’s money.

Access to large sums of low-cost and low-risk capital, via deposits, provides a bank the ability to fund loans and other ventures that generate attractive returns.

This is why the business model is so lucrative.

It’s also an enduring business model – banking dates back to antiquity.

Our society has long been dependent on banking and the flow of capital.

And unless we want to go back to a hunter-gatherer existence, our society will continue to be dependent on banking and the flow of capital.

This basic framework is made to be even more powerful by the fact that the bank is situated inside of the world’s most powerful economy.

Bank of America’s roots date back centuries, almost right back to the founding of the USA.

And I see no reason why it can’t continue to prosper for centuries more, right alongside the USA, which gives excellent visibility into more revenue, profit, and dividend growth.

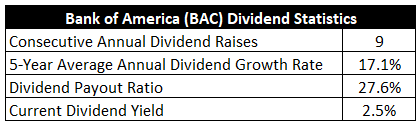

Dividend Growth, Growth Rate, Payout Ratio and Yield

To date, the company has increased its dividend for nine consecutive years.

Not the longest streak out there, as this bank, like many other banks, was severely impacted by the GFC.

But the five-year dividend growth rate of 17.1% shows atonement for past issues.

Now, some of that high growth rate has been propelled by the fact that the dividend was coming off of such a low base.

However, the current yield of 2.5% is high enough so as to not require double-digit dividend growth in order to make sense of the investment.

However, the current yield of 2.5% is high enough so as to not require double-digit dividend growth in order to make sense of the investment.

That market-beating yield, by the way, is 40 basis points higher than its own five-year average.

I imagine shareholders would be satisfied with high-single-digit dividend growth from here.

And with a payout ratio of only 27.6%, the dividend is healthy and easily positioned for a lot more growth ahead.

I like dividend growth stocks in what I call the “sweet spot” – a yield of between 2.5% and 3.5%, paired with high-single-digit (or higher) dividend growth.

The yield is on the low end of that range, but the high dividend growth rate compensates for this.

Very good dividend numbers.

Revenue and Earnings Growth

As good as these numbers are, they’re mostly looking in the rearview mirror.

But investors have to look through the windshield and invest today’s capital based on their assumption for tomorrow’s returns.

That’s why I’ll now build out a forward-looking growth trajectory for the company, which will later be of great help when the time comes to estimate intrinsic value.

I’ll first show you what the bank has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then unveil a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast should allow us to come to a reasonable conclusion about where the company may be going from here.

Bank of America raised its revenue from $89.8 billion in FY 2013 to $95 billion in FY 2022.

That’s a compound annual growth rate of 0.6%.

Not great.

I’d certainly like to see a higher number here.

However, it must be pointed out that the last decade was extremely challenging for banks.

Low interest rates, heavy-handed regulation, and a lumpy economy have conspired to constrain the growth of banks.

Meanwhile, earnings per share grew from $0.90 to $3.19 over this period, which is a CAGR of 15.1%.

Thanks to prolific buybacks and a general improvement in profitability metrics, there’s been plenty of excess bottom-line growth.

And this is what has fueled a lot of that big dividend growth.

Regarding the buybacks, Bank of America has reduced its outstanding share count by almost 30% over the last decade.

Looking forward, CFRA forecasts that Bank of America will compound its EPS at an annual rate of 6% over the next three years.

It’s an interesting forecast.

I say that because Bank of America compounded its EPS at over 15% annually during an extremely difficult decade.

With higher rates, a strong consumer, and the GFC far behind us, the future should look even brighter than the past.

But I actually like that CFRA is erring on the side of caution here.

There is good reason to be cautious.

CFRA sums it up best with this passage: “The bank does have exposure to an economic downturn, interest rate volatility, and weaker loan demand from both consumer and commercial customers.”

There are concerns that the US could be staring down a recession soon.

With the possibility of a downturn coming up, it makes a lot of sense to peel back the growth expectations from a bank.

After all, the collective banking industry is the spearhead of the economy.

Well, a large institution like Bank of America will likely feel the effects of a recession very directly.

However, a recession is definitely not a foregone conclusion, and I do consider myself cautiously optimistic on 2023 and beyond.

I believe that Bank of America can, and should, do better than CFRA is giving them credit for.

Besides, even if CFRA’s low number is what comes to pass, Bank of America can still grow its dividend at a high-single-digit rate for the foreseeable future.

The low payout ratio gives them some leeway on this front.

And if Bank of America grows the business at something closer to 10%, that sets the dividend up for like growth.

When you’re starting off with that 2.5% yield, that’s a compelling combination yield-and-growth combination.

Financial Position

Moving over to the balance sheet, I see nothing to indicate anything other than a rock-solid financial position.

The bank has $3.1 trillion in total assets against $2.8 trillion in total liabilities.

Bank of America’s long-term senior debt has investment-grade credit ratings: Standard & Poor’s, A-; Moody’s, A2; Fitch, AA-.

Profitability is robust, and there’s been consistent improvement across the board.

Over the last five years, the firm has averaged annual net margin of 26.6% and annual return on equity of 9.7%. Net interest margin came in at just under 2% last fiscal year.

Bank of America is a financial powerhouse headquartered in the world’s economic powerhouse.

And the company is protected by durable competitive advantages, such as massive economies of scale, high switching costs, unique financial expertise, and built-up relationships.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

I’d argue that all three of these risks are elevated for a large bank.

Banks are highly exposed to economic cycles.

A recession can hurt the bank’s income statement (reduced loan demand) and balance sheet (higher loan losses).

While the absolute size is an advantage, it also limits the relative growth that can be produced.

Ongoing changes in financial technology may make it easier for upstarts to take market share.

Bank of America’s international footprint exposes it to geopolitics and different currencies.

I see these risks as quite manageable, especially when weighed against the overall appeal of the enterprise.

That appeal is amplified by what I believe is a low valuation…

Stock Price Valuation

The P/E ratio is 11.3.

Banks usually command low earnings multiples.

But after the stock’s nearly 30% drop in pricing from its 52-week high, this seems unusually low.

The five-year average P/E ratio for this stock is 13.

We can see that the P/B ratio of 1.2 is also low, and is right in line with its own five-year average.

And the yield, as noted earlier, is substantially higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

With the long-term EPS and dividend growth rates, respectively, both being well over this rate, I don’t think I’m being overly aggressive with the model.

Keep in mind, the payout ratio is very low.

And even with CFRA’s cautious near-term EPS growth forecast, there’s no reason why Bank of America can’t afford a high-single-digit dividend growth rate straight through.

While I acknowledge that the next year or two may see modest dividend increases from a prudent management team, the long-term path ahead looks better than the one that’s already been traveled.

And I must say, that prior path looks really good in and of itself.

The DDM analysis gives me a fair value of $37.84.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think I was judicious with the model, yet the stock comes out looking noticeably undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates BAC as a 3-star stock stock, with a fair value estimate of $37.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates BAC as a 4-star “BUY”, with a 12-month target price of $43.00.

I came out very close to where Morningstar is at. Averaging the three numbers out gives us a final valuation of $39.28, which would indicate the stock is possibly 9% undervalued.

Bottom line: Bank of America Corp. (BAC) is a financial powerhouse headquartered in the world’s economic powerhouse. The last decade was surprisingly great for the bank. The next decade could be even better. With a market-beating yield, a double-digit dividend growth rate, a low payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 9% undervalued, long-term dividend growth investors ought to consider investing in this company alongside Warren Buffett.

Bottom line: Bank of America Corp. (BAC) is a financial powerhouse headquartered in the world’s economic powerhouse. The last decade was surprisingly great for the bank. The next decade could be even better. With a market-beating yield, a double-digit dividend growth rate, a low payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 9% undervalued, long-term dividend growth investors ought to consider investing in this company alongside Warren Buffett.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is BAC’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 55. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, BAC’s dividend appears Borderline Safe with a moderate risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income