Is there anything better than dividend growth investing? I don’t think so.

Here’s how it goes. You buy shares in a high-quality business that’s paying safe, growing dividends. You then, potentially, collect increasing passive income for the rest of your life.

It’s like a personal ATM machine that just keeps spitting out ever-more cash. And you really do need to make sure that your income is rising over time.

Why? Well, inflation will definitely make sure that your expenses are rising over time.

Today, I want to tell you about 6 dividend growth stocks that just increased their dividends.

Ready? Let’s dig in.

The first dividend increase I want to bring to your attention is the one that was announced by Archer-Daniels-Midland (ADM).

Archer-Daniels-Midland just increased its dividend by 12.5%. Boy, you’ve gotta love that. I don’t believe I ever got a 12.5% annual pay raise back when I still had a day job. Certainly not for doing nothing at all. Yet, that’s exactly what happened here. ADM shareholders did nothing other than hold shares, and their passive income went up by 12.5%. That’s about as good as it gets.

This is the 48th consecutive year of dividend increases for the multinational food processing and commodities trading corporation. Nearly 50 straight years of ever-higher cash payments to shareholders. That’s an incredible amount of consistency from this Dividend Aristocrat.

This is the 48th consecutive year of dividend increases for the multinational food processing and commodities trading corporation. Nearly 50 straight years of ever-higher cash payments to shareholders. That’s an incredible amount of consistency from this Dividend Aristocrat.

The 10-year DGR is 8.6%, which is already strong, but this most recent dividend increase blows that trend away. Now, the stock’s yield is 2.2%. Not a heavy hitter when it comes to income, but this has been a fantastic long-term compounder. The stock is up by more than 100% over the last five years alone, so focusing too much on the yield is missing the forest for the trees. With the payout ratio at only 21.4%, based on TTM adjusted EPS, we’re almost guaranteed to see ADM continue to aggressively increase the dividend for years to come.

As I recently said in a video, I love this business. And I love the stock. But the valuation is hard to love.

Indeed, we recently covered ADM in a video going over five of my best-performing stocks over the course of 2022. I went over each of those names, their performance, and what I think of them today.

Well, ADM was in that video – it returned nearly 40% last year. But that kind of stellar performance has, in my view, led to a stretched valuation based on an unusually high earnings base. For current shareholders, you’re sitting pretty. But for those looking to buy in? I’d really prefer to see either a sizable correction or solidification of earnings. Either way, keeping this Dividend Aristocrat on your radar is a great idea.

The second dividend increase we have to quickly discuss today is the one that came in from Air Products & Chemicals (APD).

Air Products & Chemicals just increased its dividend by 8%. Another high-quality company. Another inflation-beating dividend increase. This is dividend growth investing in action. You commit to one action – buying those shares – and then you, potentially, get rewarded – and increasingly so – forever.

This marks the 41st consecutive year of dividend increases for the global producer and supplier of industrial gases. This is another Dividend Aristocrat doing Dividend Aristocrat things.

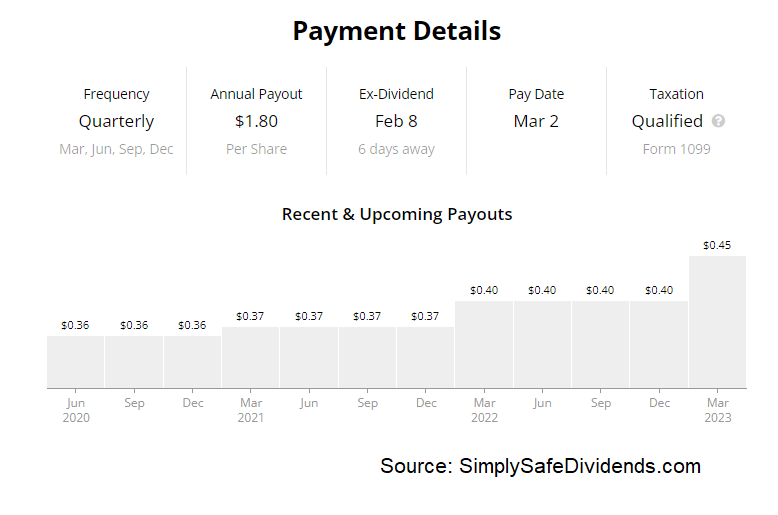

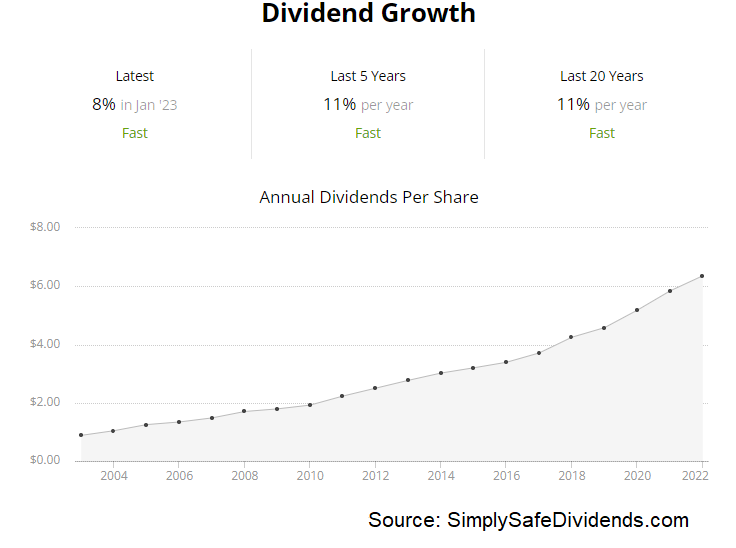

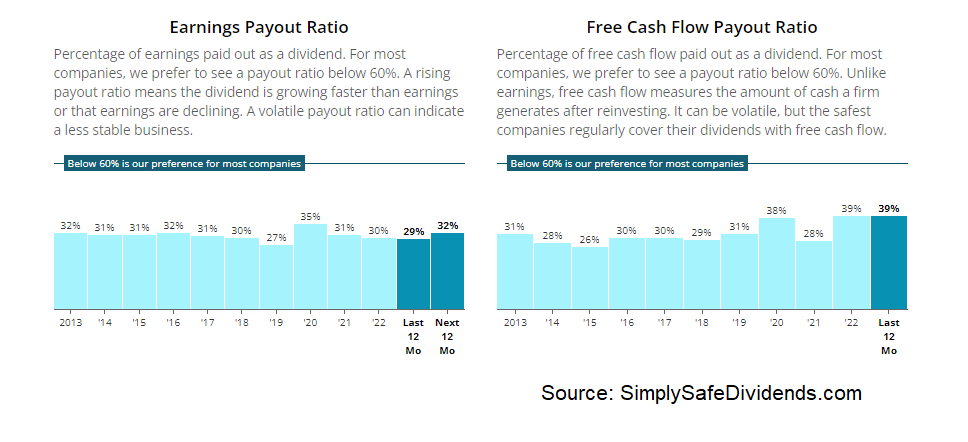

The 10-year DGR is 9.8%. We are a bit below that long-term trend with this most recent dividend raise, but it’s also exactly the kind of dividend boost that I’d expect from this business. And you’re able to pair that high-single-digit dividend growth rate with the stock’s market-beating yield of 2.2%. Not a bad combination at all. Based on midpoint guidance for FY 2023 adjusted EPS, the payout ratio is 61.7%. So there’s no trouble whatsoever with the dividend.

The 10-year DGR is 9.8%. We are a bit below that long-term trend with this most recent dividend raise, but it’s also exactly the kind of dividend boost that I’d expect from this business. And you’re able to pair that high-single-digit dividend growth rate with the stock’s market-beating yield of 2.2%. Not a bad combination at all. Based on midpoint guidance for FY 2023 adjusted EPS, the payout ratio is 61.7%. So there’s no trouble whatsoever with the dividend.

The stock has gone on a huge run, but I still see some decent value here. Now, it’s not as cheap as it was when we highlighted it back in August as an undervalued high-quality dividend growth stock to consider buying. However, in that video, we did estimate fair value for the business at right about $330/share. The stock is currently selling for about $314.

I’m not saying it’s the best deal in the whole market. And it’s not as appealing as it was when we made that video, back when the stock was priced at about $258. But if you’re in it for the next, you know, 20 or 30 years, I think you’re going to do very, very well with this business. A pullback would be nice, but it’s just a terrific business to have working for you over the long term.

Next up, let’s discuss the dividend increase that came courtesy of Comcast Corporation (CMCSA).

Comcast just increased its dividend by 7.4%. This might be my favorite dividend raise in today’s group. Not because it’s the biggest but because it totally goes against the narrative that Comcast is some dying cable company. The business isn’t dying. And neither is the dividend. When both are growing, that’s the opposite of dying.

The media and entertainment conglomerate has now increased its dividend for 16 consecutive years. It’s been said that the safest dividend is the one that just got raised. Well, Comcast just keeps on raising that dividend and proving what a durable business it has.

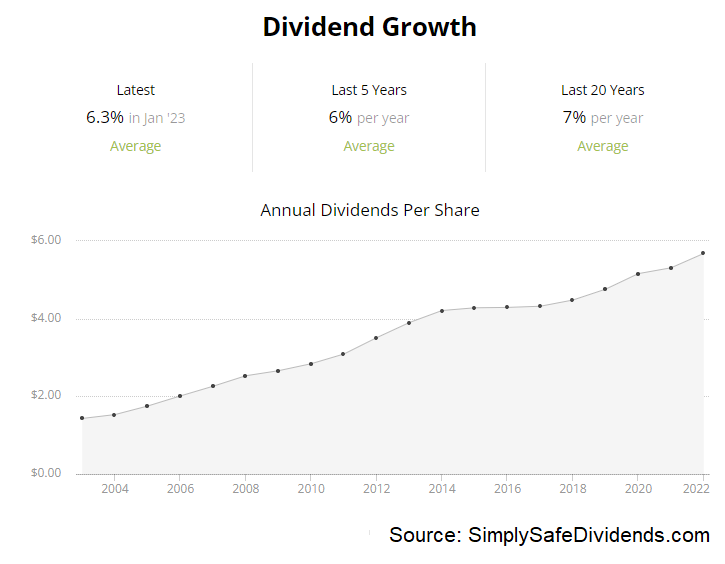

The 10-year DGR is 13.3%. Now, there has been some deceleration in that dividend growth rate. It was over 14% just recently. Then last year’s dividend increase came in at 8%. And this one here is obviously a bit below 8%. Still, I expect Comcast to continue increasing the dividend at a high-single-digit rate for the foreseeable future, which is an expectation that’s backed by a payout ratio of 31.9%, based on FY 2022 adjusted EPS. And you’re also getting a 2.9% yield from the stock to start off with. Not bad at all.

I think this stock is materially undervalued. Comcast has been cheap for a while now. It’s been shunned by a market that fears it’s dying, despite numbers that indicate the total opposite. And that disconnect is precisely where the long-term opportunity might lie.

I think this stock is materially undervalued. Comcast has been cheap for a while now. It’s been shunned by a market that fears it’s dying, despite numbers that indicate the total opposite. And that disconnect is precisely where the long-term opportunity might lie.

We just put together a full analysis and valuation video on Comcast, estimating intrinsic value for the firm at slightly over $56 per share. With shares currently trading hands for less than $40/each, I see immense value here. This most recent dividend raise was almost right on target in terms of the dividend discount model analysis I used to value the business. If your portfolio has room for it, Comcast is very much worth taking a close look at here.

The fourth dividend increase we have to go over today is the one that came through from Chevron Corporation (CVX).

Chevron just increased its dividend by 6.3%. So you can look at this in one of two ways. On one hand, it’s more money. And 6.3% more, at that. For doing nothing other than not selling shares you already bought.

On the other hand, some might be disappointed that it wasn’t a bigger dividend increase, considering how strong the business has been. But I like the prudence here. Shows how thoughtful management is in the current energy environment and political climate.

The multinational energy corporation has now increased its dividend for 36 consecutive years. Yet another Dividend Aristocrat doing what they do best – reliably increasing their dividends through thick and thin.

What’s notable here about Chevron’s dividend raise is that it came along with the announcement that the company also authorized a new $75 billion buyback program – about 20% of the entire company’s market cap. Astounding.

Getting back to the dividend, we’ve got a 10-year DGR of 4.9%, which means this most recent dividend raise was actually an outsized one. The stock yields 3.4%. Nice income for sure. And the payout ratio is a lowly 33%. With that kind of payout ratio, and with the outstanding share count falling so dramatically, this dividend is headed higher.

Getting back to the dividend, we’ve got a 10-year DGR of 4.9%, which means this most recent dividend raise was actually an outsized one. The stock yields 3.4%. Nice income for sure. And the payout ratio is a lowly 33%. With that kind of payout ratio, and with the outstanding share count falling so dramatically, this dividend is headed higher.

I’d like to see Chevron at a cheaper level, but the paradigm has shifted in its favor. Not long ago, Chevron was being completely vilified. But the social and political stance has become more favorable after an energy shock, which has created a renewed appreciation for reliable energy. That said, the stock has already reacted to this.

Chevron was featured in a recent video where I went over some of my personal big winners from 2022, and I did note in that video that I’d be cautious here. Chevron’s stock returned over 50% last year. That’s a huge move. However, if the stock comes down a bit from here, you’ve got that new, larger dividend and the massive buyback program working for you.

The fifth dividend increase I want to bring to your attention is the one that was announced by Home BancShares (HOMB).

Home BancShares just increased its dividend by 9.1%. Home BancShares is operating as Centennial Bank. Centennial flies under the radar. But this bank keeps on delivering the goods, as evidenced by yet another dividend raise for its shareholders. Hold shares. Get paid ever-more money. A pretty good deal, if you ask me.

This is the 13th consecutive year in which the bank holding company has increased its dividend. That’s a fairly lengthy track record for a bank that few people have ever heard of. Now, the dividend growth is a bit lumpy. Some years are amazing. Some less so. And there’s been a deceleration in dividend growth here.

Consider the 10-year DGR of 19.4% against this sub-10% dividend raise. Still, this is nearly 10% more income. For doing nothing. Hard to complain. And the stock also yields 3.2%. That might be the best combination of yield and dividend growth out of the six dividend growth stocks we’re going over today. And the payout ratio is 50%, which I consider to be a “perfect” balance between retaining earnings for growth and returning capital to shareholders. Good stuff.

This small, under-the-radar bank looks like a fair deal at these levels. Now, the bank has a market cap of less than $5 billion. And there are unique risks when you’re dealing with such a small bank. But you’re getting a 3%+ yield, strong dividend growth, and what I consider to be a “perfect” payout ratio.

Regarding the valuation, every basic valuation metric I look at is basically right in line with its own respective recent historical average. The P/B ratio is 1.3. Its five-year average is 1.4. The P/E ratio of 14.6 lines up almost exactly with its own five-year average of 14.5. What I really like here is the bank’s exposure to Florida and Texas, which are markets that are growing quickly. If you like smaller financial institutions, this one has an interesting setup for sure.

Regarding the valuation, every basic valuation metric I look at is basically right in line with its own respective recent historical average. The P/B ratio is 1.3. Its five-year average is 1.4. The P/E ratio of 14.6 lines up almost exactly with its own five-year average of 14.5. What I really like here is the bank’s exposure to Florida and Texas, which are markets that are growing quickly. If you like smaller financial institutions, this one has an interesting setup for sure.

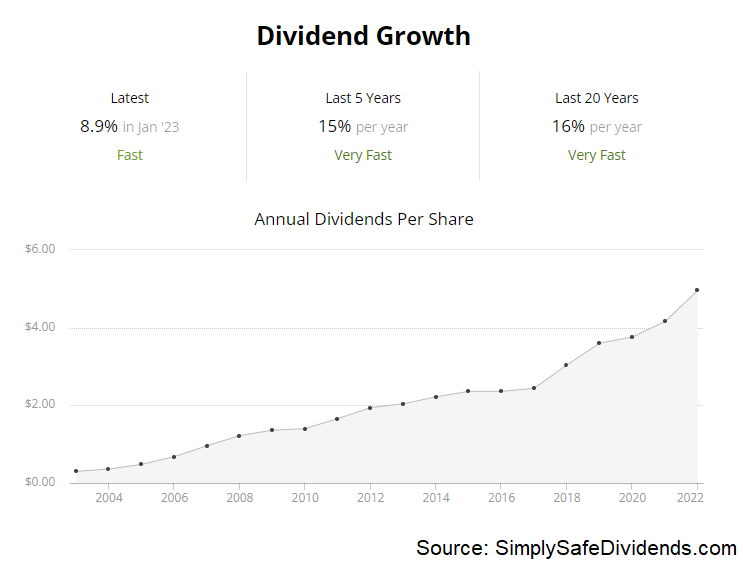

Last but not least, I have to highlight the dividend increase that came from Norfolk Southern (NSC).

Norfolk Southern just increased its dividend by 8.9%. Choo-choo. All aboard this dividend increase. Norfolk Southern did go through a stretch from 2015 to 2016 where the dividend was held unchanged, but the dividend growth has come steaming back since 2017. This dividend raise is more evidence that this dividend train is operating at full speed.

The railroad company has now increased its dividend for seven consecutive years. Now, this short track record really does belie this company’s impressive overall credentials and significant dividend growth potential. And that’s only because the company did have a short stretch that broke a nice streak.

The railroad company has now increased its dividend for seven consecutive years. Now, this short track record really does belie this company’s impressive overall credentials and significant dividend growth potential. And that’s only because the company did have a short stretch that broke a nice streak.

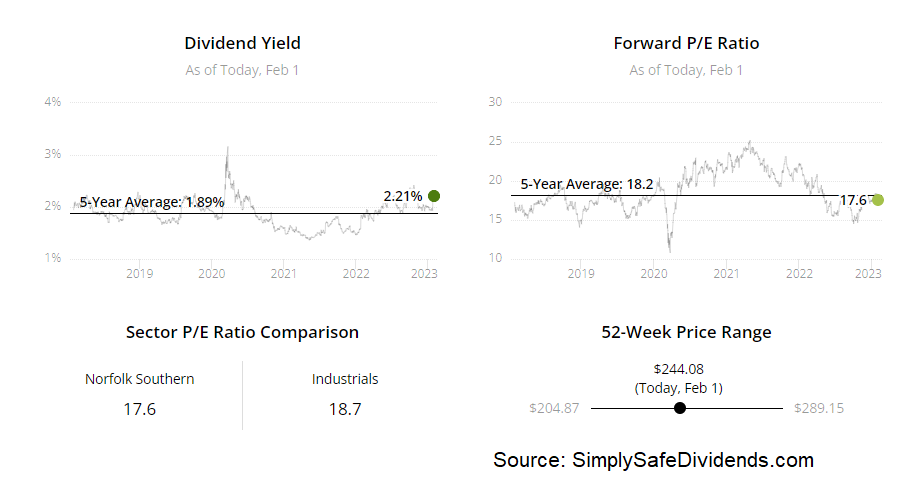

But things are back on course. The five-year DGR is 15.2%. And the stock yields 2.3%, which is 50 basis points higher than its own five-year average. Plus, the payout ratio is only 38.9%. Terrific dividend metrics here.

Terrific dividend metrics. Terrific business. The valuation isn’t so terrific, but I also think it’s quite reasonable.

Look, here’s the thing about a railroad like Norfolk Southern: We’re not building these anymore. The railroads that currently exist are all that will ever exist. You don’t get a higher barrier to entry than this. Getting into the valuation, I see nothing unreasonable at all here.

We’ve got a P/E ratio of 17.2. Its own five-year average is 19.4. The cash flow multiple of 13.3 is also showing a disconnect in comparison to its own five-year average of 14.4. I really love the railroads. And this is a rare moment in time in which there’s something buyable here, especially after a near-9% dividend boost. If you haven’t boarded this one yet, consider changing that.

We’ve got a P/E ratio of 17.2. Its own five-year average is 19.4. The cash flow multiple of 13.3 is also showing a disconnect in comparison to its own five-year average of 14.4. I really love the railroads. And this is a rare moment in time in which there’s something buyable here, especially after a near-9% dividend boost. If you haven’t boarded this one yet, consider changing that.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income