I live well below my means.

I’m normally only spending a small fraction of my income in any given month.

As such, I don’t really find myself shopping at stores very often.

Or do I?

Funnily enough, I’m “shopping” nearly every single day, except it’s not at a typical “store”.

My kind of “shopping” is done at the stock market “store”.

Indeed, I invest far more than I spend.

My favorite “merchandise”?

Easy.

High-quality dividend growth stocks.

These stocks represent equity in world-class enterprises that pay reliable, rising dividends to their shareholders.

How can these businesses afford to pay reliable, rising dividends?

They must produce reliable, rising profits.

It’s that simple.

You can find hundreds of these stocks by checking out the Dividend Champions, Contenders, and Challengers list.

This list has gathered invaluable data on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I’ve been “shopping” for years now, routinely buying high-quality dividend growth stocks.

buying high-quality dividend growth stocks.

This behavior has culminated in the FIRE Fund.

That’s my real-money portfolio, which produces enough five-figure passive dividend income for me to live off of.

The dividend income produced by the Fund more than covers my bills.

This allowed me to retire in my early 30s.

I spell out the whole journey – going from in debt to financially independent – in my Early Retirement Blueprint.

Buying the “right” stock is always important.

Buying the “right” stock is always important.

But that’s not all.

It’s also about buying at the “right” valuation.

Price is what you pay, but value is what you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying high-quality dividend growth stock “merchandise” from the stock market “store”, and doing so when good deals are present, will surely serve one much better over the long run than buying typical merchandise from typical stores.

Of course, spotting those good deals first requires one to understand the basics of valuation.

Fear not.

Fellow contributor Dave Van Knapp has made this easier than ever before, via his Lesson 11: Valuation.

Part of a larger series of “lessons” on dividend growth investing as a whole, it deftly explains valuation and how to go about quickly valuing just about any dividend growth stock you’ll run across.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Intercontinental Exchange Inc. (ICE)

Intercontinental Exchange Inc. (ICE)

Intercontinental Exchange Inc. (ICE) is an operator of global financial exchanges and clearing houses, and also provides mortgage technology, data, and listing services.

Founded in 2000, but with certain roots dating back to the late 1700s, Intercontinental Exchange is now a $61 billion (by market cap) financial powerhouse that employs nearly 10,000 people.

The company reports results across the following three segments: Exchanges, 54% of FY 2021 revenue; Fixed Income and Data Services, 26%; and Mortgage Technology, 20%.

The company’s most well-known offering is the New York Stock Exchange, which is the largest stock exchange in the world.

I rarely shop at stores.

I actually rarely buy merchandise of any kind.

As a frugal guy who lives well below his means and loves investing, the only “store” I spend a lot of time in is the stock market.

Well, owning shares in Intercontinental Exchange allows you to own a slice of the world’s largest “store” for stocks.

But here’s the thing about this “store” versus a more typical store: Intercontinental Exchange runs its own miniature monopoly.

Whereas many different types of merchandise can be simultaneously found at many different competing stores, this company has a lock on what it sells.

If you want to buy any stock that is listed on the NYSE, for example, that leads you straight to this company.

And then you’ve got the futures contracts and clearing on top of it.

But wait.

There’s more.

While that’s already a great business model, Intercontinental Exchange has also bolted on high-margin data and technology services – leveraging their tremendous scale and built-in information.

The pending $13.1 billion offer to acquire Black Knight Inc. (BKI), a premier provider of integrated technology, data, and analytics in the mortgage industry, further adds to this story.

This company is just plain dominant.

And it’s becoming even more dominant.

That’s what sets up such a clear path toward higher revenue and profit, which should translate to a growing dividend for as far as the eye can see.

Dividend Growth, Growth Rate, Payout Ratio and Yield

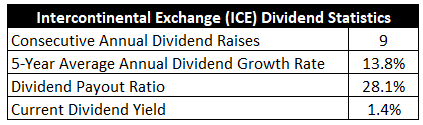

The company has increased its dividend for nine consecutive years already.

The five-year dividend growth rate of 13.8% shows what a dividend compounding machine this business is.

Better yet, there’s been an acceleration in dividend growth off of that already-lofty level.

The most recent dividend raise came in at an astounding 15.2%.

The most recent dividend raise came in at an astounding 15.2%.

On the other hand, the stock yields only 1.4%.

While that is 20 basis points higher than its own five-year average, it does trail the broader market slightly.

These metrics are suitable for younger dividend growth investors who are more concerned with compounding than income.

And with a payout ratio of only 28.1%, based on TTM adjusted EPS, I see the continuation of a high rate of dividend compounding ahead.

Revenue and Earnings Growth

As attractive as this compounding picture might look, it’s mostly based on backward-looking information.

However, investors must risk today’s capital for tomorrow’s returns.

That’s precisely why I’ll now build out a forward-looking growth trajectory for the business, which will later be instrumental during the valuation process.

I’ll first show you what this company has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should give us the ability to reasonably determine what the future growth path of the business might look like.

Intercontinental Exchange marched its revenue from $1.4 billion in FY 2012 to $7.1 billion in FY 2021.

That’s a compound annual growth rate of 19.8%.

Very impressive.

I usually look for a mid-single-digit top-line growth rate from a mature business like this.

We’re clearly well above that level.

However, the company has been aggressively acquisitive over the last decade, which means a lot of this growth wasn’t organic in nature.

Looking at per-share profit growth should give us a better idea of the true growth profile of the business.

Earnings per share grew from $1.50 to $7.18 over this period, which is a CAGR of 19%.

Extraordinary.

We can see the top-line growth largely dropping down to the bottom line.

And we can also see how the company has been able to afford the generous dividend raises – the funding has come from spectacular profit growth.

Looking forward, CFRA believes that Intercontinental Exchange will grow its EPS at a compound annual rate of 8% over the next three years.

If this manifests itself, it would represent a material slowdown in comparison to what the business has produced over the last decade.

Realistic?

I think so.

The exchange portion of the company is firmly entrenched and protected.

Of that, there is no doubt.

Seeing as how that’s the largest portion of the company, I’m quite sanguine about the overall long-term prospects of the entire enterprise.

But Intercontinental Exchange also has pretty decent exposure to the US housing market.

That once-red-hot market has cooled way down as a result of unsustainable prices and rising interest rates.

This translates to less demand for a lot of services from Intercontinental Exchange.

The bifurcation in the prospects for different elements of the company is summed up by CFRA with this passage: “Results should benefit from strength in the Exchange and Fixed Income segments, while the Mortgage segment will likely contract given a steep decline in industry wide mortgage activity as mortgage rates rip higher.”

All that said, high-single-digit near-term EPS growth is nothing to shake one’s fist at.

Many companies would be quite pleased with that kind of growth.

And seeing as how the payout ratio is so low, 8% EPS growth could actually support moderately higher dividend growth until the company is back to its high-growth ways.

Meantime, the worst-case scenario might be high-single-digit dividend raises for a bit.

The compounding machine could spit out slightly less money over the next few years, but the long-term picture looks extremely bright.

Financial Position

Moving over to the balance sheet, Intercontinental Exchange has a solid financial position.

The long-term debt/equity ratio is 0.5, while the interest coverage ratio is over 14.

Profitability is highly robust.

Over the last five years, the firm has averaged annual net margin of 33.9% and annual return on equity of 13.7%.

Margins are somewhat lumpy from year to year, but there has been a general upward trend over the last decade.

This is a terrific company with monopolistic economics that is growing at a very impressive rate.

And with proprietary assets, exclusive data ownership, and nearly infinite scalability of markets, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

The very business model lends itself to extra regulatory pressure.

And the exchanges are very competitive with another for new listings.

The company is exposed to currency exchange rates.

If the Black Knight deal closes, the balance sheet will take a hit.

The company’s acquisitive nature exposes it to integration and execution risks.

Any broad slowdown in the US housing market reduces demand for the company’s mortgage offerings.

A global economic slowdown would also negatively impact volumes across the exchanges, although the economics of the exchanges induces a lot of recurring revenue that is stable.

I see these risks as really quite manageable, especially when viewed against the overall quality and growth of the business.

The valuation, which looks attractive after a 20%+ drop in the stock price from its 52-week high, only adds to the appeal…

Stock Price Valuation

The stock’s P/E ratio is 19.7, based on TTM adjusted EPS.

For this kind of growth, that’s actually a low earnings multiple.

The P/CF ratio of 17.3 compares favorably to its own five-year average of 20.2.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 10-year dividend growth rate of 12%, and a long-term dividend growth rate of 8%.

The two stages of growth are designed to account for the unusually high rate of recent dividend growth, which is something that cannot persist indefinitely.

Now, the last dividend raise came in at over 15%.

And we’ve got a very low payout ratio here.

I believe that the company is perfectly capable of handing out low-double-digit dividend increases for the foreseeable future.

There’s nothing to strongly indicate otherwise.

However, it’s only prudent to downshift the expectation when looking out over a longer period of time.

It may not be perfectly smooth, but I think this is a reasonable assumption of the long-term dividend growth path.

The DDM analysis gives me a fair value of $115.09.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

My model was quite fair, yet the pricing looks low anyway.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates ICE as a 4-star stock, with a fair value estimate of $130.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates ICE as a 4-star “BUY”, with a 12-month target price of $115.00.

I landed almost dead on the nose with CFRA’s number. Averaging the three numbers out gives us a final valuation of $120.03, which would indicate the stock is possibly 11% undervalued.

Bottom line: Intercontinental Exchange Inc. (ICE) is a terrific business with monopolistic economics. If you want to traffic in certain securities, you will have no choice but to work with Intercontinental Exchange. With a very high rate of dividend growth, a low payout ratio, a market-like yield, nearly 10 consecutive years of dividend increases, and the potential that shares are 11% undervalued, this is a desirable candidate for dividend growth investors looking for a high-quality compounder on sale.

Bottom line: Intercontinental Exchange Inc. (ICE) is a terrific business with monopolistic economics. If you want to traffic in certain securities, you will have no choice but to work with Intercontinental Exchange. With a very high rate of dividend growth, a low payout ratio, a market-like yield, nearly 10 consecutive years of dividend increases, and the potential that shares are 11% undervalued, this is a desirable candidate for dividend growth investors looking for a high-quality compounder on sale.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is ICE’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 89. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, ICE’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income