The S&P 500 is off to a great start in 2023. We’re up about 5% on the year. For only one month, that’s obviously stellar, especially when you consider that on an annualized basis.

Despite the jump, though, we remain well off of recent highs. Now, maybe some of those prior highs weren’t deserved in the first place. We had lower interest rates, different trends, companies that temporarily overearned, etc.

Things change fast. But we have to remember one thing.

Price is what you pay, but value is what you get. And if market volatility brings price to a level that’s well below value, that’s your moment.

Price and yield are inversely correlated. All else equal, lower prices result in higher yields, which makes the dream of living off of safe, growing dividend income come true that much faster.

This is why it’s so important to jump in when volatility takes hold, sends pricing lower, and compresses valuation. I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

All that said, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for February 2023.

Ready? Let’s dig in.

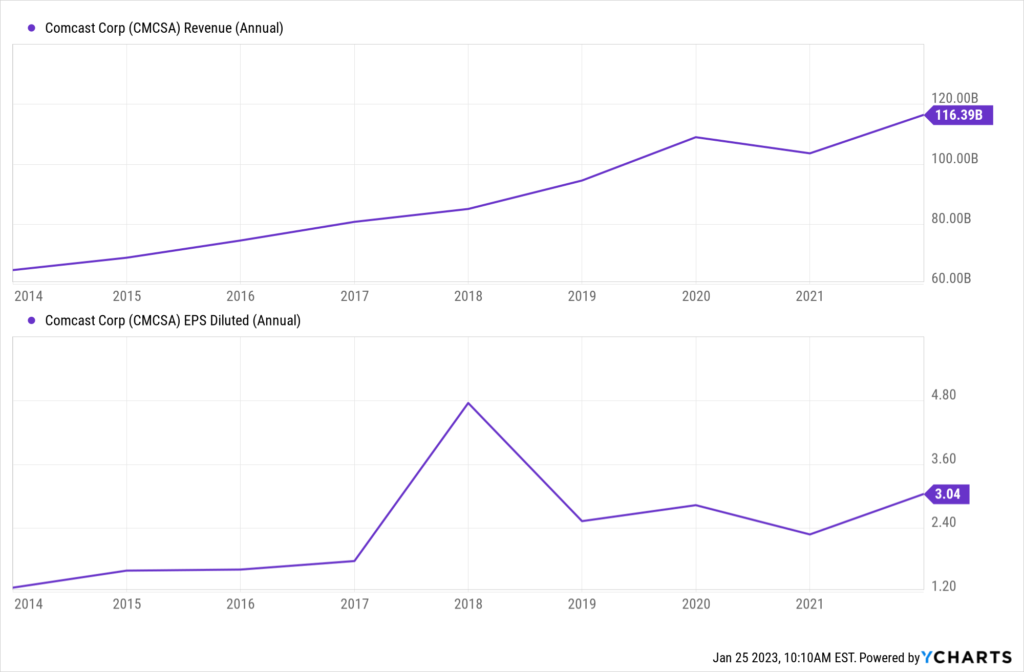

My first dividend growth stock pick for February 2023 is Comcast Corporation (CMCSA).

Comcast is a media and entertainment conglomerate. This is perhaps the oddest case of narrative versus reality that I have ever seen in business. The narrative is that it’s a dying cable company.

The reality is that it’s a growing conglomerate, with areas of the business, such as broadband, seeing increasing demand. Want proof of this disconnect? Okay. How about a compound annual growth rate of 7.1% for revenue over the last decade? How about a compound annual growth rate of 11.5% for EPS over that period?

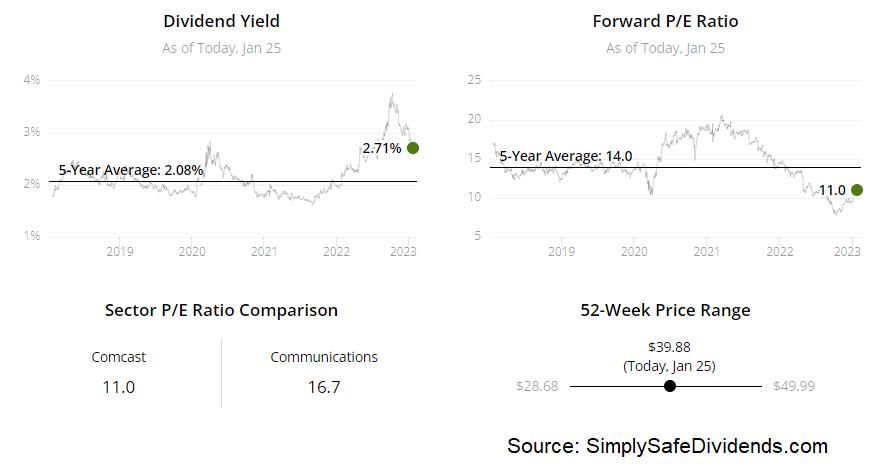

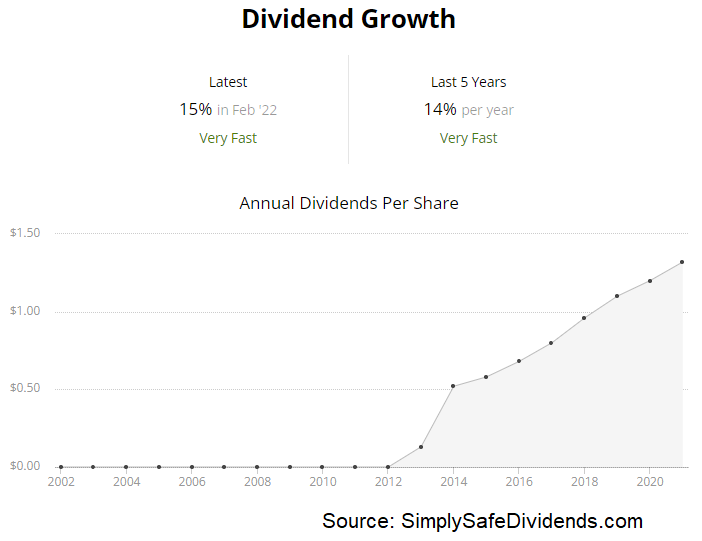

Want further proof? The dividend growth oughta satisfy. Comcast has increased its dividend for 14 consecutive years, with a 10-year dividend growth rate of 14.2%. Does that sound like a dying business… or a dying dividend? I don’t think so. The stock yields 2.7%, which is 60 basis points higher than its own five-year average. And the payout ratio is only 30%, based on TTM adjusted EPS. This is the opposite of a dying dividend. It’s a healthy dividend poised for much more growth.

Want further proof? The dividend growth oughta satisfy. Comcast has increased its dividend for 14 consecutive years, with a 10-year dividend growth rate of 14.2%. Does that sound like a dying business… or a dying dividend? I don’t think so. The stock yields 2.7%, which is 60 basis points higher than its own five-year average. And the payout ratio is only 30%, based on TTM adjusted EPS. This is the opposite of a dying dividend. It’s a healthy dividend poised for much more growth.

This stock has had a bounce off of its low, but it still looks very undervalued. This stock is up almost 40% from its 52-week low. Here’s the thing, though: Stock prices are constantly changing, but business value doesn’t change all that often. And regarding the latter, I think its number is still far higher than the former.

Indeed, while this stock is currently priced at around the $40 mark, we recently put together a full analysis and valuation video on Comcast, showing why the business could be worth $56.11/share. The business isn’t dying, nor is the dividend. However, if the stock continues its meteoric rebound, the opportunity to buy at a severe discount might die. Take a look at it.

Indeed, while this stock is currently priced at around the $40 mark, we recently put together a full analysis and valuation video on Comcast, showing why the business could be worth $56.11/share. The business isn’t dying, nor is the dividend. However, if the stock continues its meteoric rebound, the opportunity to buy at a severe discount might die. Take a look at it.

My second dividend growth stock pick for February 2023 is Intercontinental Exchange (ICE).

Intercontinental Exchange is a leading global provider of data, technology, and market infrastructure. You are familiar with this company, even if you think you’re not.

That’s because it owns the New York Stock Exchange. Yeah, that New York Stock Exchange. The one that lists many of the stocks that you’re likely buying. If the exchange business weren’t already good enough – and it is good enough – Intercontinental Exchange has also bolted on high-margin data businesses on top of it. This is why the company has compounded its revenue at an annual rate of 19.8% and its EPS at an annual rate of 19% over the last decade.

Double-digit business growth. Double-digit dividend growth. The company’s nine-year track record of an ever-higher dividend belies its true potential, as the company in its current format is quite new, despite the fact that many of its components are extremely old.

I mean, the NYSE dates back to the 1700s. Still, the five-year dividend growth rate is 13.8%. Even the most recent dividend raise came in at over 15%. And with a payout ratio of 28.1%, based on TTM adjusted EPS, this dividend is almost guaranteed to head higher. The only knock against the dividend is the stock’s yield – at 1.4%, there’s something to be desired. But this is really more of a compounder than an income play.

I mean, the NYSE dates back to the 1700s. Still, the five-year dividend growth rate is 13.8%. Even the most recent dividend raise came in at over 15%. And with a payout ratio of 28.1%, based on TTM adjusted EPS, this dividend is almost guaranteed to head higher. The only knock against the dividend is the stock’s yield – at 1.4%, there’s something to be desired. But this is really more of a compounder than an income play.

Want to own a slice of the NYSE? Here’s your chance. I rarely buy things. Most of my free cash flow is allocated toward stocks.

Stocks are my favorite “merchandise”. And the stock market is my favorite “store”. As such, owning a slice of a store I shop at frequently is quite a compelling idea. This high-quality compounder looks to be at least moderately undervalued. And I think that’s all you can really ask for.

The P/E ratio, based on adjusted EPS, is 20.1. I don’t think that’s an unreasonable earnings multiple for a name that is compounding at well into the double digits. We’ll have a full analysis and valuation video coming out soon for this one, so keep an eye out for that. Meanwhile, if you’re putting stocks in your shopping cart, consider putting the store itself in there.

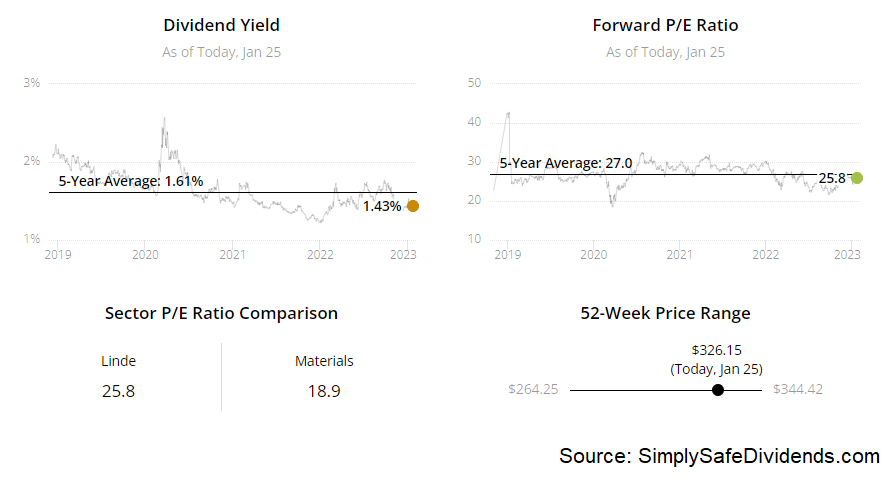

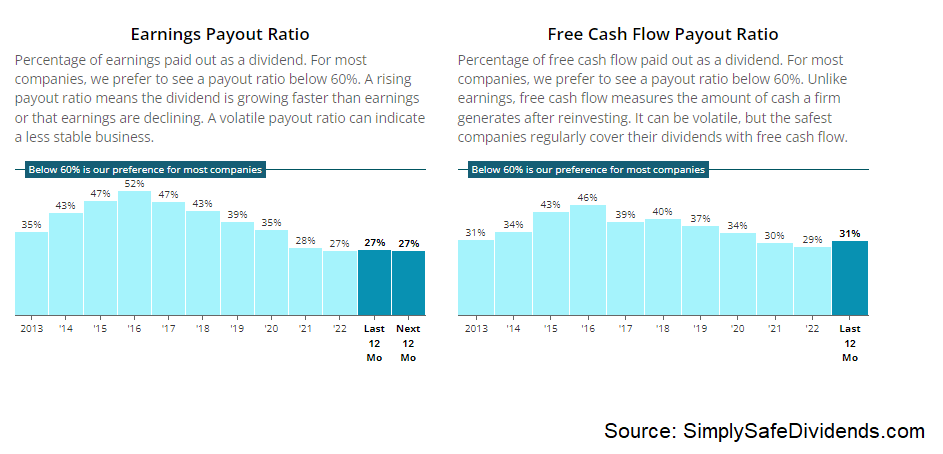

My third dividend growth stock pick for February 2023 is Linde PLC (LIN).

Linde is the world’s largest industrial gases company. Enjoy modern-day society where stuff gets manufactured? Well, that manufacturing process doesn’t really happen without the industrial gases that companies like Linde provide.

These gases are so critical that manufacturers will sign long-term contracts with reliable providers, and then they’ll have complex infrastructure get put on site. This creates an extremely visible revenue stream for Linde. And it’s only growing. The company’s revenue has compounded at an annual rate of 11.9% over the last 10 years, while EPS has compounded at an annual rate of 7.4% over that period.

Manufacturers need reliable providers of gases.

Manufacturers need reliable providers of gases.

Dividend growth investors need reliable providers of growing dividends. Linde suits both.

Yep, this is a Dividend Aristocrat, with 29 consecutive years of dividend increases.

The 10-year DGR is 7.8%, although this has shown some acceleration of late.

The stock only yields 1.4%, so that’s kind of a bummer.

However, the payout ratio is only 39.1%, based on this fiscal year’s EPS guidance.

So that recent acceleration in dividend growth looks set to continue for the foreseeable future. If you want a super high yield for income today, there are other choices out there. But if you want a high-quality Dividend Aristocrat to compound your wealth and income, making you rich over the long term, Linde is a great candidate.

This Dividend Aristocrat looks modestly undervalued right now. Warren Buffett said: “It’s far better to buy a wonderful company at a fair price, than a fair company at a wonderful price.” I couldn’t agree more.

After investing for more than a decade myself, and after seeing so many fair companies that looked cheap only become cheaper as they fall behind wonderful companies, I’ve come to take Buffett’s advice to heart.

Well, Linde definitely fits the wonderful company label. And I think the pricing is better than fair right now. We already put content together on Linde, analyzing the entire business and estimating its intrinsic value. That estimate shakes out to slightly over $350/share. The stock is currently priced at about $329. Significantly undervalued? I don’t think so. But better than fair.

Well, Linde definitely fits the wonderful company label. And I think the pricing is better than fair right now. We already put content together on Linde, analyzing the entire business and estimating its intrinsic value. That estimate shakes out to slightly over $350/share. The stock is currently priced at about $329. Significantly undervalued? I don’t think so. But better than fair.

My fourth dividend growth stock pick for February 2023 is Microsoft Corporation (MSFT).

Microsoft is a global technology company. I cannot imagine any future in which our collective global society is less reliant on technology. No. It’s quite the opposite – we are all becoming more and more reliant on all forms of technology. And it’s accelerating.

Back in 1900, we were still riding around on horses. But back when I was in high school, the Internet was still new. Things are moving very, very quickly. All of that bodes well for Microsoft, which is at the vanguard of all kinds of technology, including cloud, software, and even AI. This has propelled incredible growth – an 11% CAGR for revenue and a 15.8% CAGR for EPS over the last decade.

Microsoft is a beast. And that goes for the dividend, too. The company has increased its dividend for 20 consecutive years.

That’d be impressive for any industry. But in the tech world, where 20 years is a lifetime, it’s especially impressive. And I think it goes a long way toward showing how durable and resilient this business is. The 10-year DGR is 12%. And this is one of the healthiest dividends in the whole world, backed by a sterling balance sheet and a low, low 29.3% payout ratio.

However, the 1.2% yield does lend itself toward a preference by younger dividend growth investors who want to compound their wealth and income at a high rate over a long period of time.

However, the 1.2% yield does lend itself toward a preference by younger dividend growth investors who want to compound their wealth and income at a high rate over a long period of time.

This compounding machine actually appears to be buyable, which is a rare event. The stock is almost always expensive, as it probably should be.

You tend to get what you pay for. And if you want cheap prices, you get cheap stuff. If you want quality, you have to pay up. You don’t get a diamond for the price of a cubic zirconia. Simple as that. Well, this is a rare moment in time in which I actually think Microsoft shares are buyable.

We recently put together a full analysis and valuation video on Microsoft, showing why its shares could be worth almost $300/each. The stock is currently priced at around $240. Microsoft is one of the best businesses I’ve ever seen. This looks to be about as good as it gets in terms of opportunities to buy.

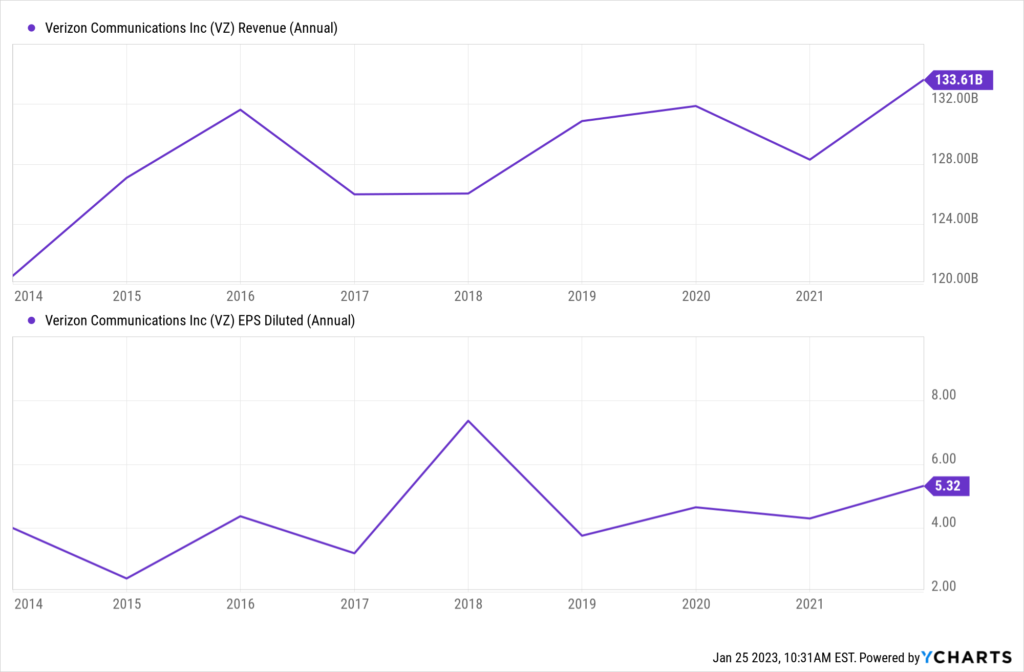

My fifth dividend growth stock pick for February 2023 is Verizon Communications (VZ).

Verizon is a multinational telecommunications conglomerate. Verizon is a very different business than Microsoft. But they do have something in common: They are both offering services that are ubiquitous at this point.

Try to find someone who doesn’t use mobile data. Look around. Everyone is on their smartphones. And these smartphones are connected.

Connected to what? To networks. Networks like the one that Verizon provides.

Otherwise, those smartphones are expensive bricks. Unlike Microsoft, Verizon isn’t growing at a super high rate. But it’s decent. We’re talking about revenue that has grown at a compound annual rate of 1.6% over the last 10 years, while EPS has compounded at an annual rate of 3.6% over the last nine years. I advanced that latter number due to an unsuitable GAAP result for FY 2012.

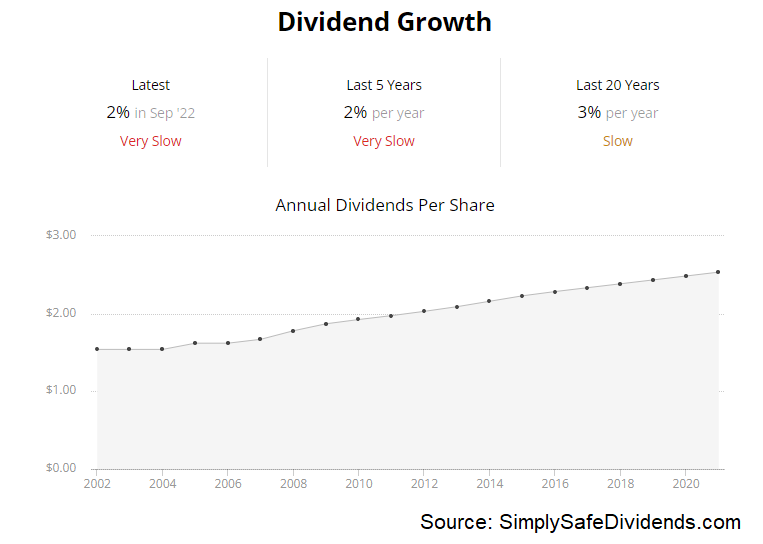

Also decent is the dividend growth. But what’s far better than decent is the yield. Verizon is a great choice for those who want yield.

Also decent is the dividend growth. But what’s far better than decent is the yield. Verizon is a great choice for those who want yield.

Why? The stock yields a monstrous 6.6% yield. So if you don’t like some of the other names on this list because of low yields, here’s yield. However, there’s no free lunch in life.

Always trade-offs.

In this case, you have to give up a lot of growth. While the dividend has been increased for 18 consecutive years, it’s been a snail’s pace. The 10-year DGR is only 2.5%. Still, it’s a big dividend that can be used to pay bills, or you can reinvest it. And there’s nothing wrong with that, especially if it’s used to balance the overall yield of a portfolio that also has those really high-quality compounders in it. With a payout ratio of 50.4%, based on FY 2022 adjusted EPS, this big dividend appears to be quite safe.

I’m not a fan of chasing yield. But I think Verizon’s big dividend is worth a go.

I’m not a fan of chasing yield. But I think Verizon’s big dividend is worth a go.

In fact, I recently added to my own Verizon position. I picked up shares back in December for $37.03/each, and I alerted my Patrons over at Patreon about that move when it happened. The stock is up modestly since then, but we’re not talking about a huge difference here.

The business is still priced at about $40/share. The P/E ratio, based on adjusted EPS, is only 7.8. Because of the low growth rate and high debt load, Verizon should command a low earnings multiple. But this is too low, in my view.

Its five-year average P/E ratio is 11.1, for perspective. This stock is nearly 30% lower than its 52-week high, so the market has really punished this one. I’m not a fan of chasing yield, but Verizon’s 6%+ yield is one of the few high yields that I do favor in this market. Take a look at it.

— Jason Fieber

Imagine having 12 new monthly income checks, carrying the potential of up to 21% yields.This is possible because of a tested strategy to get paid out regularly, like a paycheck. For over a decade, I have helped more than 26,000 investors secure 12 new monthly payouts. Meaning, you know exactly how much you'll make every month... Because of some stocks that pay us 8%,13.4%, and even 21.6% yields. See it for yourself here.

Source: Dividends & Income