Warren Buffett would tell you that being born in the USA is akin to winning the “genetic lottery”.

I concur.

There are many reasons for this.

One of the big reasons for this is, of course, direct access to, and benefits from, American capitalism.

Better yet, you can take this lottery to the next level.

Simply being born in the US is a head start.

But taking advantage of this by investing in great businesses can put you in the upper echelons of humanity.

Well, I’d argue that some of the greatest businesses you’ll find are those that pay reliable, rising dividends to their shareholders.

I’m talking about high-quality dividend growth stocks.

You can find hundreds of these stocks by perusing the Dividend Champions, Contenders, and Challengers list.

This list has compiled important data on US-stocks that have raised dividends each year for at least the last five consecutive years.

A high-quality dividend growth stock represents equity in a world-class business that produces the reliable, rising profit necessary to pay reliable, rising dividends.

After all, it’s hard to afford the latter without the former.

After all, it’s hard to afford the latter without the former.

I was born in the USA in 1982.

And I started investing in high-quality dividend growth stocks in my late 20s, building my FIRE Fund in the process.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

When I started investing, I was actually worth a negative amount of money (due to debt).

But these businesses are so great, and American capitalism is so powerful, I was propelled into financial independence only a few years later.

Indeed, I was able to quit my job and retire in my early 30s.

And that’s after starting out in my late 20s below the $0 mark.

My Early Retirement Blueprint shares how I was able to turn things around so quickly.

Now, investing in the right stocks has been key to my success.

Now, investing in the right stocks has been key to my success.

But doing so at the right valuations has also been crucial.

Price only tells you what you pay, but value tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Taking advantage of one’s “genetic lottery” by buying high-quality dividend growth stocks when they’re undervalued can parlay a head start into life-changing wealth and passive income over time.

Now, this does require one to first understand how valuation works.

But it’s not as complex as you might initially think.

Fellow contributor Dave Van Knapp simplified the entire concept with the introduction of Lesson 11: Valuation.

Part of an overarching series of “lessons” on dividend growth investing, it breaks down valuation into a template that can then be applied to almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Masco Corp. (MAS)

Masco Corp. (MAS)

Masco Corp. (MAS) is a manufacturer of products for the home improvement and new home construction markets.

Founded in 1929, Masco is now a $12 billion manufacturing might that employs 20,000 people.

The company reports results across the following two segments: Plumbing Products, 61% of FY 2021 sales; and Decorative Architectural Products, 39%.

Nearly 80% of FY 2021 sales were derived from North America.

What is the American Dream?

It’s a complicated question.

And I’m not sure that you can break it down into one simple answer.

But I would argue that homeownership is part of the ethos.

Homeownership is an aspiration that most Americans share.

Well, Masco is, in some ways, an adjacent bet on the American Dream.

That’s because many of the products it makes and sells are used in the manufacture and/or repair of homes.

Many of these products are integral to modern-day shelter.

Think faucets, toilets, plumbing valves, shower enclosures, and paints.

Boring?

Perhaps.

But try living without indoor plumbing for a few days.

And, quite frankly, even if Americans were to suddenly stop wishing to own their own homes, we’ve all gotta live somewhere.

Whether you own or rent your abode, Masco’s products are necessary for that abode to work.

As long as people continue to enjoy running water and painted walls, Masco should continue to prosper.

That means growth across revenue, profit, and the dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

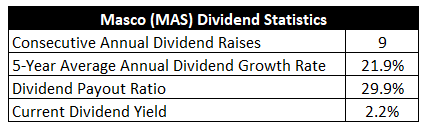

Masco has already increased its dividend for nine consecutive years.

The five-year dividend growth rate of 21.9% shows what a start Masco is off to here.

Notably, there hasn’t been a meaningful deceleration in dividend growth, either – the most recent dividend raise was 19.1%.

And you get to layer that on top of the stock’s market-beating yield of 2.2%.

And you get to layer that on top of the stock’s market-beating yield of 2.2%.

By the way, this yield is 90 basis points higher than its own five-year average.

And with the payout ratio sitting at 29.9%, based on midpoint adjusted EPS guidance for this fiscal year, the dividend appears to be very healthy.

This does lean toward growth instead of yield.

But the yield is quite a bit higher than it usually is, even though the growth hasn’t slowed.

It’s super interesting that you get the type of growth profile often reserved for tech, yet you also get a decent yield.

Revenue and Earnings Growth

As interesting as this is, these dividend metrics are largely looking in the rearview mirror.

However, investors have to accept that they’re risking today’s capital for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will later be of great use when it comes time to estimate intrinsic value.

I’ll first show you what this business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then uncover a professional prognostication for near-term profit growth.

Lining up the proven past against a future forecast in this manner should give us what we need in order to paint a picture of where the business might be going from here.

Masco increased its revenue from $7.5 billion in FY 2012 to $8.4 billion in FY 2021.

That’s a compound annual growth rate of 1.3%.

Slightly disappointing.

I’d prefer to see a higher number here.

Meantime, earnings per share grew from $0.80 in FY 2013 to $1.62 in FY 2021, which is a CAGR of 9.2%.

I did advance the starting point by one year, as FY 2012 showed a GAAP loss.

This bottom-line growth is a bit more like it, and it was aided by a combination of margin expansion and share buybacks.

Regarding the latter point, the outstanding share count is down by approximately 28% over the last decade.

Looking forward, CFRA believes that Masco will compound its EPS at an annual rate of 5% over the next three years.

This kind of growth would represent a pretty serious slowdown relative to what Masco has been enjoying.

I see this as a disconnect between the short term and long term.

Over the long term, Masco appears to be a well-positioned business that should perform really well.

Over the short term, however, Masco does have some headwinds to navigate.

I think CFRA does a good job of delineating that with this passage: “We believe demand trends will remain strong in paint and plumbing; however, we anticipate raw material/freight inflation and supply chain challenges to persist in the first half of 2022. We also expect additional investment in innovation, advertising, and marketing.”

That’s the crux of the matter.

Masco has to overcome some short-term challenges around costs.

But the long-term demand runway appears to stretch out well into the horizon.

While the next few years could be a bit of a slog, the market is a forward-looking mechanism and has already punished the stock in advance.

The realignment in pricing, which has compressed valuation multiples, is exactly why I’m covering this name in this format for the very first time.

Masco should be able to increase its dividend at a high-single-digit rate through this short-term slog, as the payout ratio is so low.

Once this “air pocket” is overcome, a rebound in bottom-line growth should propel the dividend growth back to its lofty heights.

Long-term dividend growth investors who have the patience to let that process play out could be richly rewarded with plenty of cumulative dividend income and a high rate of total return.

Financial Position

Moving over to the balance sheet, Masco has a good financial position.

The long-term debt/equity ratio isn’t meaningful because of almost no common equity, while the interest coverage ratio is over 8.

I’d like to see a better balance sheet, but it’s certainly not a deal-breaker.

Profitability is solid and improving.

Over the last five years, the firm has averaged annual net margin of 10.4%.

The margin expansion is notable, as Masco was routinely printing net margin in the mid-single-digit range a decade ago.

ROE is obviously N/A because of the non-existent common equity.

I see Masco as an interesting, adjacent way to play the US housing market.

And with economies of scale, brand recognition, and pricing power, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

The company exclusively sells its Behr paint products through Home Depot Inc. (HD), which allows Masco to avoid a lot of overhead, but it creates customer concentration (nearly 40% of FY 2021 sales).

The housing market is cyclical, which can cause volatile demand for Masco’s home construction products.

Masco has exposure to interest rates, as interest rates have a direct impact on the US housing market.

There is some minor currency exchange exposure here.

I view the balance sheet as a weakness for the business.

Masco benefited from certain pandemic-related trends, including a flight to larger homes in the suburbs, and it’s very possible that consumers revert back to pre-pandemic spending on experiences.

The state of the broader economy can affect demand for home improvement products.

These risks should be carefully thought over, but the valuation deserves the same careful attention.

And with the stock down more than 20% from its recent high, the valuation has become pretty attractive…

Stock Price Valuation

The P/E ratio is 13.8.

Even in this environment, that’s a low earnings multiple.

It compares extremely favorably to its own five-year average of 21.1.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

I’m looking at this as something that will average out nicely over the long run.

I already pointed out the likelihood of high-single-digit dividend growth over the very near term, due to the circumstances that Masco is finding itself in currently.

But as time elapses and the headwinds dissipate, I suspect that Masco will be able to return to its more recent behavior around dividend raises.

Meanwhile, the payout ratio is low.

And, other than the balance sheet chink in the armor, this is a fine, fine business.

The DDM analysis gives me a fair value of $60.48.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I believe we have a good amount of undervaluation present.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates MAS as a 5-star stock, with a fair value estimate of $74.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates MAS as a 3-star “HOLD”, with a 12-month target price of $54.00.

I came out somewhere in the middle, although I am surprised by how sanguine Morningstar is on this one. Averaging the three numbers out gives us a final valuation of $62.83, which would indicate the stock is possibly 19% undervalued.

Bottom line: Masco Corp. (MAS) is an adjacent play on the American Dream. Americans crave homeownership, which requires a lot of the products that this company provides. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 19% undervalued, dividend growth investors looking for an under-the-radar bet on the US housing market should take a good look at this one.

Bottom line: Masco Corp. (MAS) is an adjacent play on the American Dream. Americans crave homeownership, which requires a lot of the products that this company provides. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 19% undervalued, dividend growth investors looking for an under-the-radar bet on the US housing market should take a good look at this one.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is MAS’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 63. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, MAS’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income