Investing successfully over the long run is simple but difficult. It’s simple to say that you need to ignore the noise and take advantage of market volatility when it comes. But it’s difficult to actually do that in real life.

Well, I think dividend growth investing makes this a lot easier.

Dividend growth investing is a strategy whereby you buy and hold shares in world-class enterprises that pay reliable, rising dividends to their shareholders. We’re talking about some of the best businesses in the world here. And this combination of growing passive dividend income and business quality is what makes it easier to take advantage of volatility.

See, the growing dividends pay you through the volatility, making it easier to hold on. Plus, all else equal, price and yield are inversely correlated. So lower prices result in higher yields, which means more income on the same invested dollar.

Getting paid even more to hold? Yeah, that’ll help. And the quality of these businesses also helps to build confidence through market volatility.

If you’re highly confident a business will be just fine, because it’s been just fine time and time again over the course of decades prior, that makes it easier to jump in when things are getting crazy.

Today, I want to tell you about five dividend growth stocks that are down 20% or more from their recent highs.

Ready? Let’s dig in.

The first dividend growth stock I want to bring to your attention today is Fidelity National Financial (FNF).

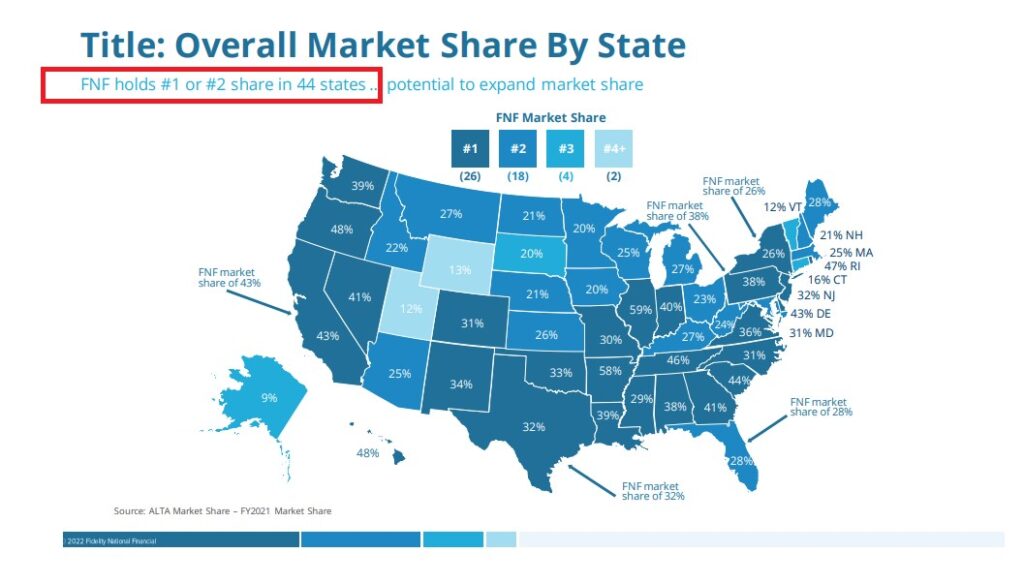

Fidelity National is a title insurance company with a market cap of $10 billion. Fidelity National isn’t just a title insurance company. It’s the largest title insurance provider in the United States. In a highly fragmented market, they’re the clear market leader. And what a market to be a leader in.

Most Americans want to own their own home. And guess what? They usually have to finance that house, because almost nobody can afford to buy a house in cash. Well, if you finance, you must have title insurance. Talk about a captive customer base.

Most Americans want to own their own home. And guess what? They usually have to finance that house, because almost nobody can afford to buy a house in cash. Well, if you finance, you must have title insurance. Talk about a captive customer base.

Plus, there are almost never any claims against the insurance. So the float just grows and grows and grows. This is why Fidelity National continues to do so well through the ups and downs of the housing market, increasing its dividend along the way.

The insurance company has increased its dividend for 11 consecutive years. The company’s 10-year DGR is 12.6%. That’s solid, in and of itself. But it’s made to look a lot better when you see that it’s paired with the stock’s market-smashing yield of 4.8%.

This yield, by the way, is 140 basis points higher than its own five-year average. What an incredible spread. And while the housing market is definitely cooling way down, Fidelity National has been here before – the company has been around for 175 years.

Meantime, with a payout ratio of 27.7%, based on TTM adjusted EPS, the dividend is protected – even in a challenging environment. In fact, the company increased the dividend, yet again, in November.

Talk about big time. This stock is down 31% from its 52-week high. The 52-week high of $54.25? Yeah, that’s long gone. Shares are now priced at roughly $37/each. What a difference a year can make. A lot of big drops in the market can be justified. That’s because many stocks were vastly overvalued before the drops occurred. I don’t think that’s the case here, though. In my view, this business went from reasonably valued to cheap.

Talk about big time. This stock is down 31% from its 52-week high. The 52-week high of $54.25? Yeah, that’s long gone. Shares are now priced at roughly $37/each. What a difference a year can make. A lot of big drops in the market can be justified. That’s because many stocks were vastly overvalued before the drops occurred. I don’t think that’s the case here, though. In my view, this business went from reasonably valued to cheap.

The P/E ratio, based on TTM adjusted EPS, is only 5.7. Whenever I see a single-digit P/E ratio, I know a lot of bad news is being priced in. The P/CF ratio of 2.3 is nearly 1/4 of its five-year average of 8.6. The stock’s price is similar to where it was in the summer of 2020 – when we were dealing with a global pandemic. Fidelity National is very, very interesting here. Take a look.

The second dividend growth stock I have to cover is Fortis (FTS).

Fortis is an international diversified electric utility holding company with a market cap of $19 billion. Utility businesses tend to be great for long-term dividend growth investors. That’s because you’re essentially betting on people’s continued demand for electricity. I’d say that’s a pretty easy bet to make. Not much of a gamble there.

Also, utility stocks tend to offer higher yields. When you combine the predictability of the business model, which often leads to smooth revenue, profit, and dividend growth, along with the higher-than-average yields, you’ve got something pretty compelling.

The utility company has increased its dividend for 49 consecutive years. What a track record. That’s one of the best dividend growth track records among all utilities.

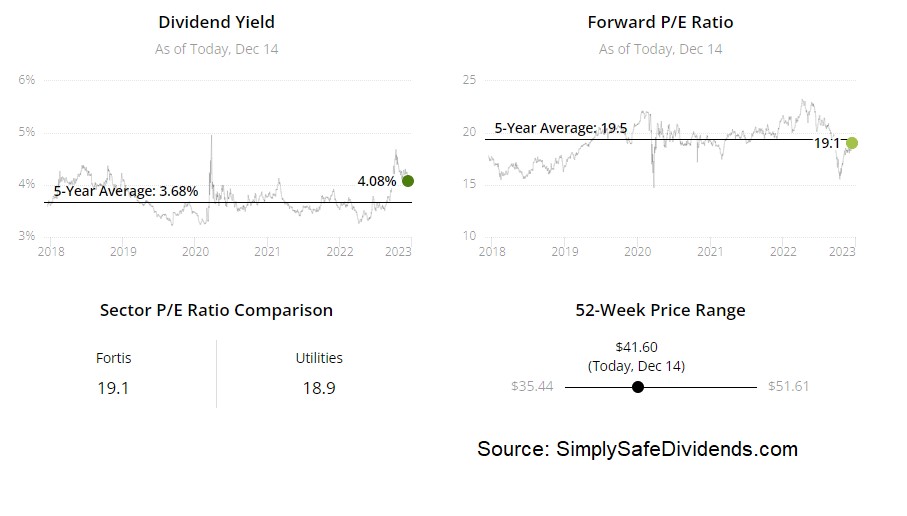

Now, that is in the native currency, which, in this case, is Canadian dollars. That’s because Fortis is based out of Canada. The currency exchange rate fluctuates, so the dividend paid in US dollars can fluctuate. Nonetheless, very impressive. The stock yields 4.1%. The dividend has compounded at an annual rate of nearly 6% over the last five years. And Fortis is guiding for 4% to 6% dividend growth to 2027.

Now, that is in the native currency, which, in this case, is Canadian dollars. That’s because Fortis is based out of Canada. The currency exchange rate fluctuates, so the dividend paid in US dollars can fluctuate. Nonetheless, very impressive. The stock yields 4.1%. The dividend has compounded at an annual rate of nearly 6% over the last five years. And Fortis is guiding for 4% to 6% dividend growth to 2027.

If they get to that upper end of guidance, you’re looking at a very nice mix of yield and growth here. The one knock here is the payout ratio. At 84%, based on TTM adjusted EPS, that’s a bit high for my liking.

This stock is down 22% from its 52-week high, and it now looks more attractive than it has in years. The stock’s price of right about $40 is way off of its 52-week high of $51.66. This was a $44 stock before the pandemic hit. So we’re about 10% lower than even that, despite the fact that Fortis has grown the business and dividend since then.

The reason I’m familiar with Fortis is because they acquired two businesses I was previously invested in – UNS Energy Corporation, and ITC Holdings Corp. I know those were both great assets, which gives me further confidence in Fortis as a whole.

Most basic valuation metrics here are basically right in line with their respective recent historical averages. The revenue multiple of 2.5, for example, is barely lower than its own five-year average of 2.6. To be honest, Fortis has almost always looked too expensive to me. But this is a rare moment in time in which it doesn’t. Keep an eye on this one.

Most basic valuation metrics here are basically right in line with their respective recent historical averages. The revenue multiple of 2.5, for example, is barely lower than its own five-year average of 2.6. To be honest, Fortis has almost always looked too expensive to me. But this is a rare moment in time in which it doesn’t. Keep an eye on this one.

The third dividend growth stock I have to bring up is Home Depot (HD). Home Depot is a multinational home improvement retailer with a market cap of $327 billion.

Home Depot is the world’s largest home improvement company. So we have yet another market leader, and yet another housing play. Why not? Anything touching housing has been trounced this year. But here’s the truth of the matter: People always need a roof over their heads. Shelter is a basic need in life.

Going beyond just basic needs, though, most people like to own that shelter and call it home. What does that involve? Plenty of maintenance, repairs, and upgrades, which is where Home Depot and its growing revenue, profit, and dividend come in.

The retailer has increased its dividend for 13 consecutive years. Like I’ve said before, I tend to think of Home Depot as the dividend depot. This company is that good at depositing ever-larger dividends straight into investor’s brokerage accounts. The 10-year DGR is 20.3%.

Even the most recent dividend raise came in at a stunning 15.2%. And the stock yields 2.4%, so you don’t need to sacrifice a lot of yield in order to access that monstrous dividend growth rate. With the payout ratio sitting at 45.8%, Home Depot has plenty of room for future dividend raises.

Even the most recent dividend raise came in at a stunning 15.2%. And the stock yields 2.4%, so you don’t need to sacrifice a lot of yield in order to access that monstrous dividend growth rate. With the payout ratio sitting at 45.8%, Home Depot has plenty of room for future dividend raises.

This stock’s 23% slide has created what I think is an appealing valuation on a wonderful business. Home Depot just screams “quality” across the board. Despite that, the market has been ruthless. This stock was $417.84 at its 52-week high? Now? It’s sitting at right about $320.

Our recent full analysis and valuation video on Home Depot showed why the business is estimated to be worth nearly $350/share. This is one of the best retailers on the planet. And if your portfolio doesn’t already have shares in it, consider changing that.

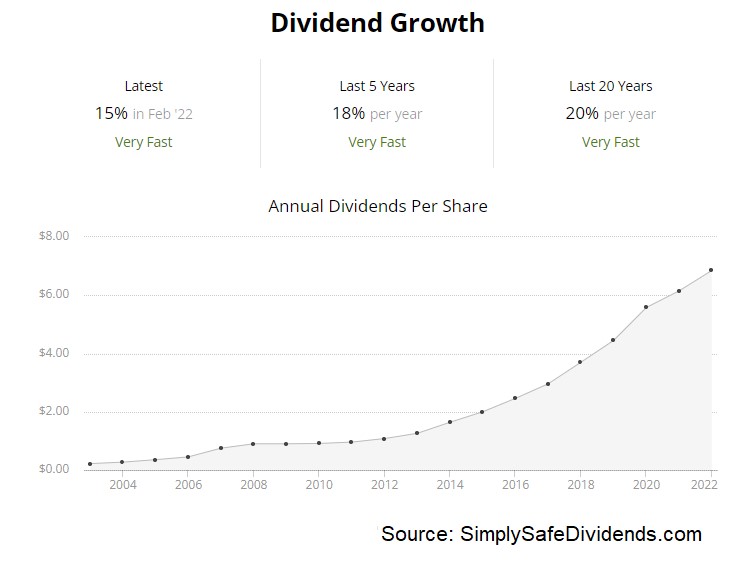

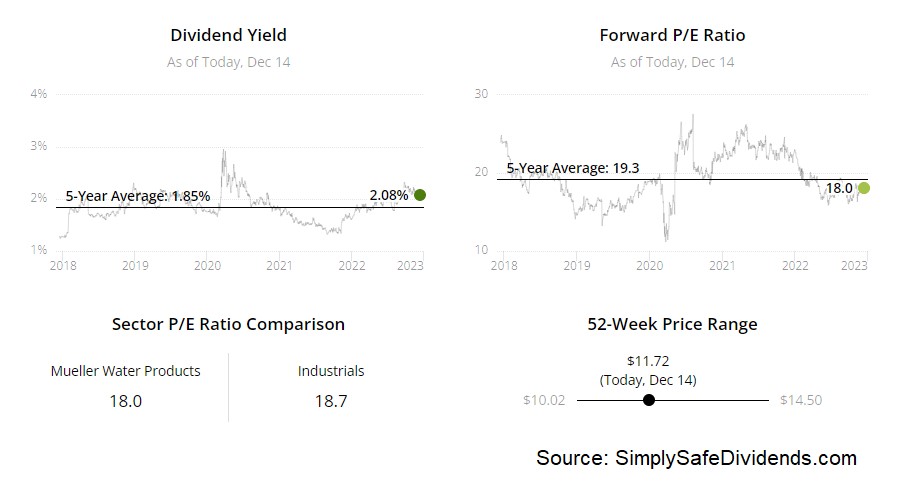

The fourth dividend growth stock to cover today is Mueller Water Products (MWA).

Mueller is a water infrastructure products company with a market cap of $2 billion. This small-cap company flies under the radar. It doesn’t get a lot of press. But it’s in a space that I have been personally very active in – water. I’ve said a number of times now that I think water will be the “liquid gold” of this century, just as oil was the “liquid gold” of the last century.

That’s based on both its importance to life and the increasing difficulties and costs to access it for a lot of people. Demand isn’t going anywhere. But supply is starting to become constrained. That sets up almost any water-related company to do well and increase its revenue, profit, and dividend for years to come.

The water infrastructure company has increased its dividend for eight consecutive years. Now, Mueller doesn’t really “wow” me in any one area. The five-year DGR is 9.1%, but recent dividend raises have been in the 5% range.

The stock’s yield of 2.1% is good, but it’s not great. And the payout ratio of 50.8% is nearly perfectly balanced between retaining earnings against rewarding shareholders, so I do like that, but it’s also not some super low payout ratio. I guess what I like here is the total dividend package, which comes wrapped inside of a business total package that doesn’t really have a lot of downside risks that I see.

The stock’s 22% drop from its 52-week high may have created a nice entry point here. The business is not growing super quickly, nor is the stock’s yield super high. So you want to gain your edge on the valuation side of things, trying to capture that potential upside. This is the kind of business where valuation becomes even more important than normal.

The stock’s 52-week high of $14.62? Expensive. But down here at below $12? I think it makes a lot more sense, keeping in mind that we’re talking about boring, but necessary, stuff like valves, fire hydrants, pipe connections, and metering products. The P/E ratio of 23.5 still isn’t exactly a mouth-watering number, but it is quite a bit below its own five-year average of 27.1. The sales multiple of 1.4, which compares favorably to its own five-year average of 1.9, tells a similar story. Back up the truck? No. But it’s at least worth having on the radar.

The stock’s 52-week high of $14.62? Expensive. But down here at below $12? I think it makes a lot more sense, keeping in mind that we’re talking about boring, but necessary, stuff like valves, fire hydrants, pipe connections, and metering products. The P/E ratio of 23.5 still isn’t exactly a mouth-watering number, but it is quite a bit below its own five-year average of 27.1. The sales multiple of 1.4, which compares favorably to its own five-year average of 1.9, tells a similar story. Back up the truck? No. But it’s at least worth having on the radar.

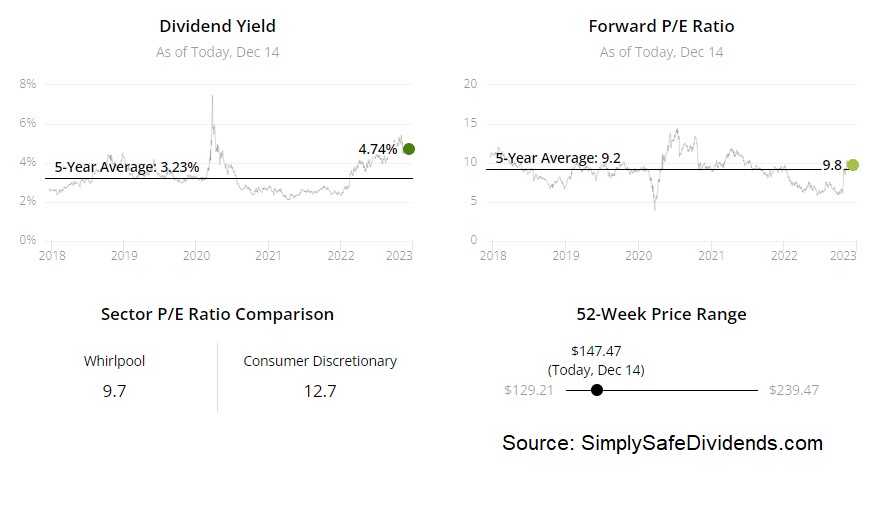

The fifth dividend growth stock we have to quickly talk about today is Whirlpool Corporation (WHR).

Whirlpool is a multinational manufacturer and marketer of home appliances with a market cap of $8 billion. This is one of those business models that even a child can understand. We’re talking about home appliances such as refrigerators and washing machines. While a lot of people like to lose money in things they don’t understand, I’d rather make money in things I do understand.

Of course, there’s more to successful investing than just understanding what you’re buying. And now isn’t a really great time for an appliance maker. But that’s why we’re talking about it here. If everything were unicorns and rainbows, the stock wouldn’t be down so much. That said, Whirlpool is still a dividend machine.

The appliance company has increased its dividend for 12 consecutive years. Some of Whirlpool’s dividend metrics are out of this world. The 10-year DGR is 12.8%. If that weren’t impressive enough, the company’s most recent dividend increase came in at 25%!

The appliance company has increased its dividend for 12 consecutive years. Some of Whirlpool’s dividend metrics are out of this world. The 10-year DGR is 12.8%. If that weren’t impressive enough, the company’s most recent dividend increase came in at 25%!

Plus, the stock yields 4.8%. How often do you see a near-5% yield paired with a double-digit dividend growth rate like this? Almost never. Based on the company’s most recent non-GAAP EPS guidance, the payout ratio is 36.8%. The one thing to be aware of here, though, is that GAAP EPS and non-GAAP EPS diverge more wildly than I’m used to seeing. That’s a bit of a red flag to me. Otherwise, outstanding dividend metrics.

This stock is down nearly 40% this year. It’s been absolutely crushed. Is that an opportunity? That’s a good question. The stock’s 52-week high of $245.44 has completely evaporated. Shares are now trading hands for about $147/each. This drop has encouraged me to bring up this name for the first time ever on the channel. Every basic valuation metric here is trailing its respective recent historical average. And by large margins, at that.

The forward P/E ratio, based on that non-GAAP guidance, is only 7.8. That’s cheeeeap. But sales and earnings are falling. Personally, I’d wait for the business to show real signs of stabilizing before jumping in. The stock could certainly rebound before that happens. But I’d rather be a bit late than way too early. Either way, I do think Whirlpool is at least worth looking at for the first time in nearly three years.

The forward P/E ratio, based on that non-GAAP guidance, is only 7.8. That’s cheeeeap. But sales and earnings are falling. Personally, I’d wait for the business to show real signs of stabilizing before jumping in. The stock could certainly rebound before that happens. But I’d rather be a bit late than way too early. Either way, I do think Whirlpool is at least worth looking at for the first time in nearly three years.

— Jason Fieber

Imagine having 12 new monthly income checks, carrying the potential of up to 21% yields.This is possible because of a tested strategy to get paid out regularly, like a paycheck. For over a decade, I have helped more than 26,000 investors secure 12 new monthly payouts. Meaning, you know exactly how much you'll make every month... Because of some stocks that pay us 8%,13.4%, and even 21.6% yields. See it for yourself here.

Source: Dividends & Income