Simple is beautiful.

This is true in many aspects of life, from one’s lifestyle to one’s investments.

Regarding that latter point, complexity isn’t only confusing but possibly harmful.

The more complex an investment is, the more likely I am to stay away from it.

Here’s sage advice from the great Peter Lynch: “Never invest in any idea you can’t illustrate with a crayon.”

A whole new generation of investors are learning this valuable lesson after recently getting burned in areas like NFTs, SPACs, innovation tech, and cryptocurrency.

I apply this advice by sticking to high-quality dividend growth stocks.

These stocks represent equity in world-class enterprises paying reliable, rising dividends to their shareholders.

We’re talking about some of the best businesses in the world.

And more often than not, they’re based on simple-to-understand business models.

You can see for yourself by perusing the Dividend Champions, Contenders, and Challengers list.

This list contains pertinent data on 700+ US-listed stocks that have raised dividends each year for at least the last five consecutive years.

A growing dividend is a very good initial litmus test for business quality.

A growing dividend is a very good initial litmus test for business quality.

After all, growing profit is what ultimately funds a growing dividend.

And it takes a high-quality business to consistently grow profit.

I believe in this so much, I’ve been personally investing in these businesses for more than 10 years now.

The FIRE Fund is the result of that consistent, focused investment activity.

It’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I do, indeed, live off of dividends.

Been doing so for years, actually.

I quit my job and retired in my early 30s, in favor of living off of dividends.

My Early Retirement Blueprint explains how I was able to do that.

It should be obvious by now that routinely buying high-quality dividend growth stocks is a major component of the Blueprint.

But that’s not all.

But that’s not all.

It’s not about just investing in the right businesses.

It’s also about investing at the right valuations.

Whereas price tells you what you pay, value tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Channeling Peter Lynch’s advice into buying undervalued high-quality dividend growth stocks could be the ultimate recipe for building impressive wealth and passive dividend income over the long term, all while sleeping well at night.

Now, this idea does require some base knowledge around valuation.

But it’s not super difficult to build this knowledge.

My colleague Dave Van Knapp has made it easier to do just that with Lesson 11: Valuation.

One of his many “lessons” that are designed to teach the ins and outs of the dividend growth investing strategy, it provides an easy-to-understand valuation model that can be applied toward almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Ingredion Inc. (INGR)

Ingredion Inc. (INGR)

Ingredion Inc. (INGR) is a leading worldwide ingredients solutions provider.

Founded in 1906, Ingredion is now a $6 billion (by market cap) ingredients powerhouse that employs 12,000 people.

FY 2021 sales are geographically segmented as follows: North America, 60%; South America, 15%; Asia-Pacific, 15%; and Europe, Middle East, and Africa, 10%.

Product categories are as follows: Starch Products, 45% of FY 2021 sales; Sweetener Products, 33%; and Co-products and others, 22%.

Ingredion turns raw materials like grains, fruits, and vegetables into value-added ingredients and biomaterials for various industries.

Ingredion also provides products for the animal feed and corn oil markets.

Examples of their products include industrial starches, high-fructose corn syrup, dextrose, and refined corn oil.

All in all, Ingredion supplies a variety of customers in over 60 industries across the world.

The food industry is their most important industry, representing about 54% of FY 2021 sales.

What I really like about Ingredion is the simple-to-understand business model.

While some investors just can’t help themselves from chasing after shiny objects they don’t fully understand, Ingredion is supplying the world with simple, yet critical, ingredients.

And the company is making a lot of money by doing so.

More and more money, in fact.

So are shareholders.

And I don’t see that changing, as the world’s population continues to grow and demand more of the end products Ingredion’s ingredients are necessary for.

That should translate to growth across the company’s revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

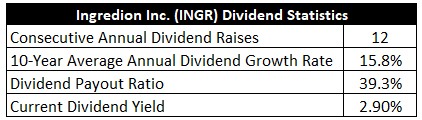

Already, Ingredion has increased its dividend for 12 consecutive years.

The company’s 10-year dividend growth rate is 15.8%.

That’s quite strong, although the size of dividend raises have been slightly lumpy along the way.

Zooming in on that, the most recent dividend raise was 9.2%.

Zooming in on that, the most recent dividend raise was 9.2%.

Either way, shareholders have likely been very happy with the dividend and the growth of it.

Along with the strong rate of dividend growth, the stock yields a market-beating 2.9%.

That yield is 10 basis points higher than its own five-year average, giving investors a bit more of an income kicker than they’re used to getting here.

And with the payout ratio at 39.3%, based on midpoint guidance for this fiscal year’s adjusted EPS, I see a healthy dividend with headroom for more growth ahead.

I always like dividend growth stocks in what I call the “sweet spot” – that’s a yield of between 2.5% and 3.5%, paired with high-single-digit (or better) dividend growth.

This stock is clearly right in the sweet spot.

Revenue and Earnings Growth

As sweet as the dividend metrics may be, these are mostly backward-looking numbers.

However, investors must face the fact that they’re risking today’s dollars for tomorrow’s rewards.

Thus, I’ll now attempt to create a forward-looking growth trajectory for the business, which will later serve as very helpful reference when it comes time to estimate intrinsic value.

I’ll first show you what this company has done in terms of top-line and bottom-line growth over the last decade.

I’ll then uncover a professional prognostication for near-term profit growth.

Comparing the proven past up against a future forecast in this way should shed light on where the business might be going from here.

Ingredion advanced its revenue from $6.5 billion in FY 2012 to $6.9 billion in FY 2021.

That’s a compound annual growth rate of 0.7%.

I’d prefer to see a higher number here, but a great business can pull multiple levers in order to drive better bottom-line growth.

To that point, earnings per share grew from $5.47 to $6.67 (adjusted) over this period, which is a CAGR of 2.2%.

I used adjusted EPS for FY 2021 because of significant one-time items that artificially skewed GAAP EPS.

One of the aforementioned levers that a business can pull is, of course, buybacks.

Ingredion did reduce its outstanding share count by approximately 12% over the last decade, which is respectable.

Like the dividend growth, EPS growth has been somewhat inconsistent over the last decade.

And so the impressiveness (or lack thereof) does depend on the starting and ending points you’re using when drawing a line and looking at growth.

But I think there’s an important point to make here.

If we look at more recent results, Ingredion has shown an acceleration in top-line and bottom-line growth.

And that acceleration in growth could be just warming up.

FY 2021 was a record year for the business in many ways, with past efforts by management finally bearing fruit (pun not intended).

The company’s “Cost Smart” cost-cutting program is restructuring the business and taking out costs.

Meantime, the “Driving Growth Roadmap” growth/investment initiative is all about creating more value by investing in core competencies and better serving customers.

Lowering costs while simultaneously increasing sales is a recipe for higher earnings power.

Ultimately, we invest in where a business is going, not where it’s been.

And the business’s path forward appears to be more exciting than the path already traveled.

CFRA believes that Ingredion will compound its EPS at an annual rate of 10% over the next three years.

This speaks on the acceleration in growth that I was just pointing out.

CFRA’s prediction can be largely backed up by Ingredion’s own adjusted EPS guidance for FY 2022, which was increased in the Q3 print to $7.23 at the midpoint.

That would represent 8.4% YOY growth.

CFRA adds this: “We see [Ingredion] as well positioned to capitalize on new consumer trends, as the company has invested millions of dollars over the past several years in areas like plant-based foods, sugar reduction, and specialty starches. In 2023, we see solid sales growth and strong margin recovery, particularly as [Ingredion] passes on more cost-justified price increases.”

Ingredion is right-sizing an improved business with increased capacity for right-sizing prices.

I personally see more benefits than drawbacks here.

On one hand, the business is looking at the secular decline of high-fructose corn syrup, and the commodity-like nature of the core business model is a negative.

On the other hand, natural sweeteners should see an increase in demand, the company’s growing portfolio of specialty ingredients offer greater pricing power, and investments in plant-based proteins position the company for growth.

Regarding the last point, Ingredion recently acquired the remaining stake of Verdient Foods Inc. that it didn’t already own, giving Ingredion the ability to produce concentrates and flours from peas, lentils, and faba beans.

This business is situated much better in 2022 than it was a decade ago.

And that bodes well for the next decade.

We can see that the company’s 10-year dividend growth rate is quite a bit higher than the demonstrated 10-year EPS growth rate.

If CFRA’s forecast is realized, that will go a long way toward rationalizing management’s behavior and fixing this gap.

It also sets the company up for at least high-single-digit dividend raises over the foreseeable future.

And stacking that on top of the near-3% starting yield is a solid setup.

Financial Position

Moving over to the balance sheet, Ingredion has a good financial position.

The long-term debt/equity ratio is 0.6, while the interest coverage ratio is nearly 9.

Profitability is quite acceptable.

Over the last five years, the firm has averaged annual net margin of 5.7% and annual return on equity of 13.2%.

These averages would be higher if not for the anomalous FY 2020 throwing them off.

Overall, I see a really good business here that’s on the cusp of greatness.

And with economies of scale, switching costs, and pricing power in a growing portion of the portfolio, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

The company is exposed to volatile input costs.

Currency exchange rates affect the international side of the business.

High-fructose corn syrup, which comprises about 10% of sales, has faced concerns over its possible links to certain health issues like diabetes.

There has been a consumer movement toward simpler foods with less ingredients, which does not work to Ingredion’s advantage.

Also, the balance sheet is not excellent, limiting future M&A opportunities.

I do see the risks here as quite manageable, especially when viewed against the quality of the business.

And with an attractive valuation, the case for investment is made to be even more compelling…

Stock Price Valuation

The stock is trading hands for a P/E ratio of 14.6.

This is a very reasonable earnings multiple, particularly with the way in which underlying growth seems to be accelerating.

It’s well below the broader market’s earnings multiple, even after the severe compression of the broader market’s P/E ratio this year.

We can also see a P/S ratio of 0.8 that compares favorably to its own five-year average of 1.

And the yield, as noted earlier, is slightly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

This dividend growth rate looks aggressive in the face of the demonstrated EPS growth over the last decade.

But it looks conservative against the demonstrated dividend growth over the last decade.

I’m splitting the difference here, and I also have CFRA’s near-term EPS growth forecast in mind.

With the payout ratio being where it’s at, and with recent earnings reports validating CFRA’s stance, I don’t see why Ingredion can’t produce high-single-digit dividend growth over the years to come.

The DDM analysis gives me a fair value of $122.12.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I don’t believe that my valuation was aggressive, yet the stock still comes out looking cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates INGR as a 4-star stock, with a fair value estimate of $120.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates INGR as a 4-star “BUY”, with a 12-month target price of $113.00.

We have a fairly tight consensus this time around, and I came out very close to where Morningstar is at. Averaging the three numbers out gives us a final valuation of $118.37, which would indicate the stock is possibly 22% undervalued.

Bottom line: Ingredion Inc. (INGR) is a really good business that appears to be on the cusp of greatness. It looks to be in the midst of turning a corner, and investors jumping on now could be in for a profitable ride. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 22% undervalued, long-term dividend growth investors ought to consider buying a slice of this business before the market reprices it higher.

Bottom line: Ingredion Inc. (INGR) is a really good business that appears to be on the cusp of greatness. It looks to be in the midst of turning a corner, and investors jumping on now could be in for a profitable ride. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 22% undervalued, long-term dividend growth investors ought to consider buying a slice of this business before the market reprices it higher.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is INGR’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, INGR’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Imagine having 12 new monthly income checks, carrying the potential of up to 21% yields.This is possible because of a tested strategy to get paid out regularly, like a paycheck. For over a decade, I have helped more than 26,000 investors secure 12 new monthly payouts. Meaning, you know exactly how much you'll make every month... Because of some stocks that pay us 8%,13.4%, and even 21.6% yields. See it for yourself here.

Source: Dividends & Income