We’re nearing the end of 2022 now. For many people, the end can’t come fast enough. It’s been a crazy year.

At one point, this was one of the worst years ever for the S&P 500. Painful, right?

Well, just as one man’s trash is another man’s treasure, one man’s pain is another man’s pleasure. I was thoroughly enjoying – and taking advantage of – the extreme volatility all year long. Turmoil that leads to cheaper stocks is a benefit for those accumulating shares in high-quality businesses.

All else equal, price and yield are inversely correlated. Lower prices? Higher yields.

If your goal, like mine, is to live off of passive dividend income, this gets you to the promised land that much faster. I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33. By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

As volatile as this year has been, not every stock is a good buy. Focusing on the very best long-term ideas right now is what this article is all about. Today, I want to tell you my top 5 dividend growth stocks for December 2022.

Ready? Let’s dig in.

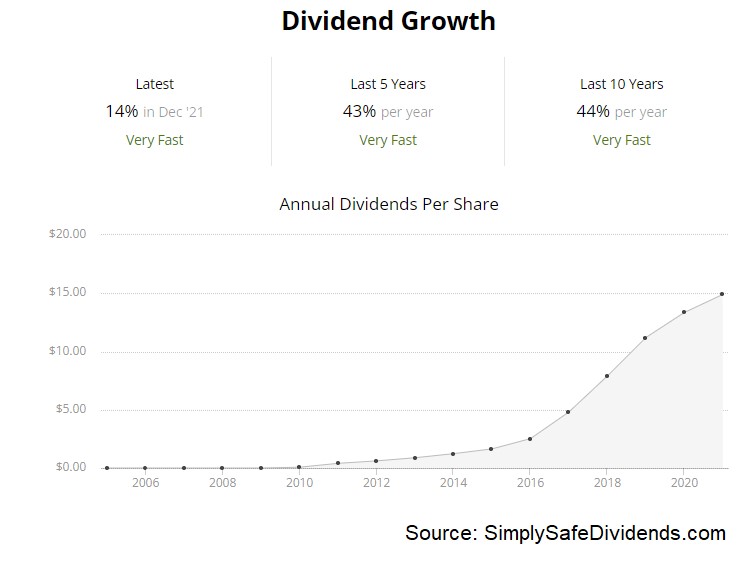

My first dividend growth stock pick for December 2022 is Broadcom (AVGO). Broadcom is a leading designer, developer, and supplier of analog and digital semiconductor devices. The days of long-term investors being able to shun tech because of the unknowns are over.

Even Warren Buffett, who famously avoided almost anything having to do with tech for decades, jumped into tech with both feet a number of years ago. If you want to make real money, you pretty much have to be in tech. Tech is shaping almost every facet of our world, changing the ways in which we live, work, and play.

Broadcom is one of the tech companies on the leading edge of this change. The company is exposed to exciting, high-growth areas like data centers, broadband, wireless connectivity, and automation. That’s what explains so much growth at the business, with a 31.1% CAGR for revenue and a 32.3% CAGR for EPS over the last decade.

If you think that’s impressive, wait until you see the dividend growth.

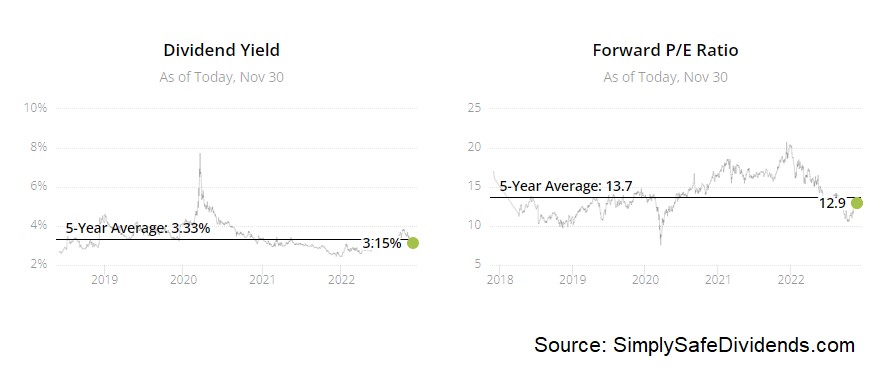

Broadcom has increased its dividend for 13 consecutive years. And get this: The 10-year dividend growth rate is a monstrous 40.2%. That’s incredible. Plus, you even get a compelling yield to go along with that. The stock yields 3.1% right now. Where else will you get a 3%+ yield with that kind of dividend growth rate? Oh, and with a payout ratio of 46.9%, based on TTM adjusted EPS, I suspect that Broadcom’s next dividend raise will be yet another sizable one. There’s certainly room for it.

Broadcom has increased its dividend for 13 consecutive years. And get this: The 10-year dividend growth rate is a monstrous 40.2%. That’s incredible. Plus, you even get a compelling yield to go along with that. The stock yields 3.1% right now. Where else will you get a 3%+ yield with that kind of dividend growth rate? Oh, and with a payout ratio of 46.9%, based on TTM adjusted EPS, I suspect that Broadcom’s next dividend raise will be yet another sizable one. There’s certainly room for it.

Who says you can’t have it all? Good yield. Sky-high growth. And even an attractive valuation.

That’s right. Broadcom seems to offer it all. The P/E ratio is below 15, based on TTM adjusted EPS. For a company growing this fast, that kind of low earnings multiple is almost unheard of. We recently put together a full analysis and valuation video on Broadcom, showing why the business could be worth just under $600/share. Shares are currently trading hands for about $530/each, so there could be a lot of upside here on a terrific business with amazing dividend metrics. It has to be at least on your radar.

That’s right. Broadcom seems to offer it all. The P/E ratio is below 15, based on TTM adjusted EPS. For a company growing this fast, that kind of low earnings multiple is almost unheard of. We recently put together a full analysis and valuation video on Broadcom, showing why the business could be worth just under $600/share. Shares are currently trading hands for about $530/each, so there could be a lot of upside here on a terrific business with amazing dividend metrics. It has to be at least on your radar.

My second dividend growth stock pick for December 2022 is Cisco Systems (CSCO).

Cisco is a leading designer, manufacturer, and supplier of data networking equipment and software. Another tech business. Shouldn’t be a surprise.

Like I said earlier, long-term dividend growth investors practically have to be in tech. What’s great about Cisco is that it’s in a lot of areas of tech that Broadcom isn’t, so you’re looking at nice diversification here when comparing these businesses. Cisco is the major supplier of switches, routers, firewalls, and supportive networking products. Cisco has long been a play on networking, which is morphing into a play on the Internet of Things.

Now, Cisco isn’t growing as fast as Broadcom. But it’s no slouch. Revenue has compounded at an annual rate of 0.7% over the last decade, while EPS has compounded at an annual rate of 6.8% over that time frame.

The dividend growth is also not slouching. Cisco’s dividend has been increased for 12 consecutive years, with a 10-year DGR of 18.3%. Recent dividend raises have been smaller, but I really do see things averaging out into a 6% to 7% dividend growth rate. And that kind of high-single-digit dividend growth is enough to get the job done.

The dividend growth is also not slouching. Cisco’s dividend has been increased for 12 consecutive years, with a 10-year DGR of 18.3%. Recent dividend raises have been smaller, but I really do see things averaging out into a 6% to 7% dividend growth rate. And that kind of high-single-digit dividend growth is enough to get the job done.

That’s because you’re starting off with the stock’s yield of 3.1%. The moderate payout ratio of 53.9% gives some flexibility to the dividend, keeping it safe and positioned to grow.

Cisco won’t knock you dead in any one area. Instead, it’s just the overall package that’s so appealing. That includes the valuation.

Take the earnings multiple, for instance. The forward P/E ratio is only 13.7, based on midpoint adjusted EPS guidance for FY 2023. There’s nothing demanding about that. Cisco simply doesn’t have to do much as a business in order to rationalize that.

Cisco isn’t growing as quickly as Broadcom. But Cisco does have a much better balance sheet. And Cisco isn’t as reliant on huge M&A deals, either. So I think there’s room for both in a portfolio. We’ll have a video coming out soon that will go over the entire business, and it’ll show why Cisco is potentially worth right about $56/share.

The stock is currently hovering around $48. So I do see it as an undervalued name here. Take a good look at Cisco, if you haven’t already.

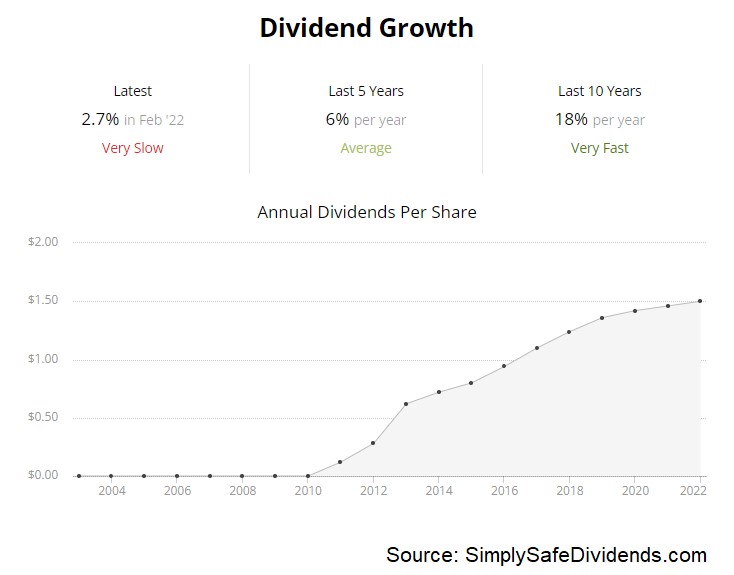

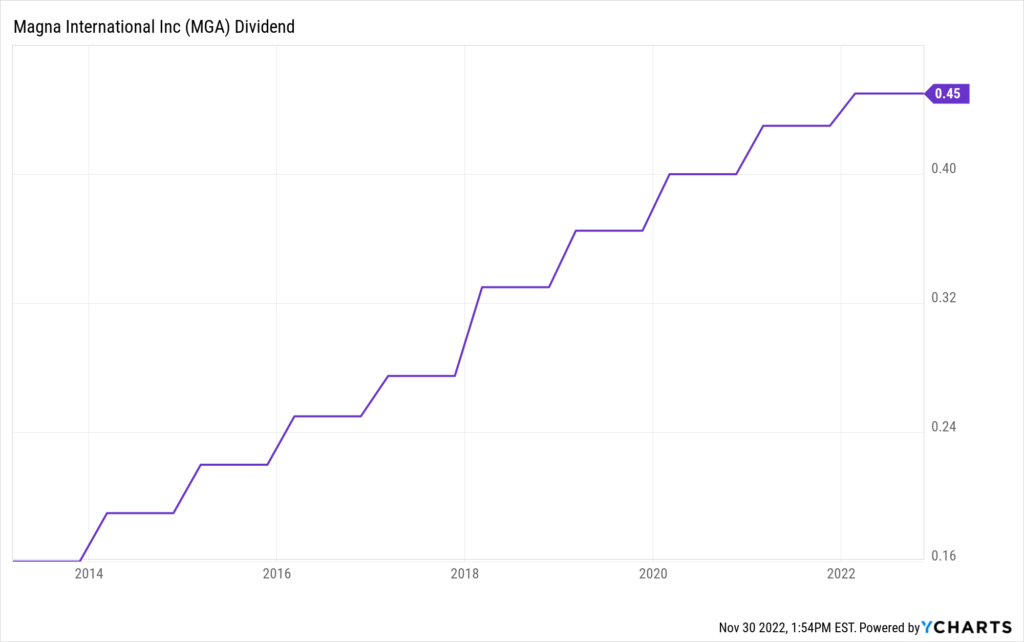

My third dividend growth stock pick for December 2022 is Magna International (MGA).

Magna is a multinational mobility solutions and technology company. Magna flies under the radar, despite being one of the world’s foremost manufacturers in the mobility space.

Magna manufactures OEM components for various automakers. It’s one of the largest such manufacturers. But it’s not just large. Magna’s capabilities are so comprehensive, it could practically be its own carmaker. But there’s no need. They’re making good money doing what they’re doing.

Indeed, revenue has compounded at an annual rate of 1.8% over the last decade, while EPS sports a CAGR of 5.7% over that time frame. And that’s after factoring in all of the supply chain challenges over the last two years. Not bad at all.

The dividend growth story isn’t bad, either. Magna has increased its dividend for 13 consecutive years. We have a really good start here, too. The 10-year DGR is 12.7%. And you’re pairing that double-digit dividend growth rate with the stock’s yield of 2.9%.

The dividend growth story isn’t bad, either. Magna has increased its dividend for 13 consecutive years. We have a really good start here, too. The 10-year DGR is 12.7%. And you’re pairing that double-digit dividend growth rate with the stock’s yield of 2.9%.

If you can get a yield near 3%, and then see that dividend compound exponentially at a double-digit rate, you’re going to be looking at substantial dividend income over the long run. A 12.7% DGR means the dividend is doubling roughly every five years. That adds up quickly.

Meantime, the payout ratio is 45.3%, based on TTM adjusted EPS. That indicates a rather safe dividend, even with so much uncertainty going on in the auto industry right now.

Meantime, the payout ratio is 45.3%, based on TTM adjusted EPS. That indicates a rather safe dividend, even with so much uncertainty going on in the auto industry right now.

All of that uncertainty has caused the market to trim this stock’s valuation, which I think has created a nice long-term opportunity. This stock was going for over $100 in the summer of 2021. We’re now at about $61. That’s a heck of a drop.

Of course, a sizable drop in price is in and of itself not necessarily evidence of undervaluation, if a business simply went from extremely overvalued to less overvalued. But I don’t think that really applies here. Magna did look overvalued at $100/share. But, at $61/share, it now looks undervalued.

The pendulum has swung too far, in my view. Our full analysis and valuation video on Magna, which came out only weeks ago, made the case as to why the business may be worth approximately $69/share. We potentially have some very respectable upside here on a world-class manufacturer. Magna is worth serious consideration right now.

My fourth dividend growth stock pick for December 2022 is Realty Income (O).

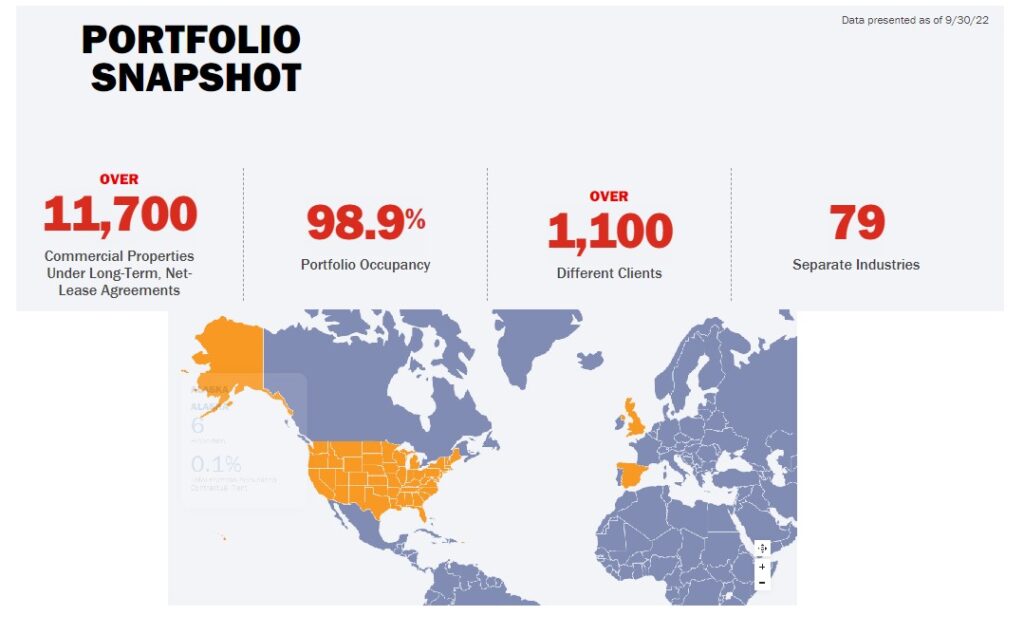

Realty Income is a triple-net-lease retail real estate investment trust. This is one of the largest REITs in the world, focusing on leasing freestanding, single tenant, triple-net-leased retail properties. We’re talking about a portfolio of over 11,700 properties that’s diversified across the US, Puerto Rico, Spain, and the UK.

Also diversified is the company’s industry exposure: Realty Income serves more than 1,100 clients operating across 79 different industries. And the occupancy rate here is excellent. As of the end of September 2022, the property portfolio has an occupancy rate of 98.9%.

Also diversified is the company’s industry exposure: Realty Income serves more than 1,100 clients operating across 79 different industries. And the occupancy rate here is excellent. As of the end of September 2022, the property portfolio has an occupancy rate of 98.9%.

If you love real estate but would rather let a wonderful REIT like Realty Income do all of the hard work for you, buying its shares could be a great arrangement. The REIT has compounded its revenue at an annual rate of 17.7% over the last 10 years, while funds from operations per share has compounded at an annual rate of 5.9% over that period.

The beauty of this company is right in its name. It’s all about income. And not just income, by the way. Monthly income. Realty Income pays its dividend monthly. Collecting that monthly dividend is a lot like collecting monthly rent, except it’s far easier. Realty Income takes the monthly dividend so seriously, it actually trademarked its moniker: The Monthly Dividend Company®.

You can see further evidence of the commitment to the monthly dividend in the lengthy track record of dividend raises, which stands at 28 consecutive years. Yes. Realty Income is a Dividend Aristocrat. The 10-year DGR is 5.3%. And the stock yields 4.6%. Solid income. Solid growth. Doubtless commitment to shareholders. The payout ratio of 73.8%, which is really quite moderate for a REIT, should give you further confidence in the dividend.

This is one of the best REITs in the world, but you wouldn’t know that by the valuation. In spite of Realty Income’s size and quality, the valuation is pretty humble. The forward P/FFO ratio is 15.7, based on this fiscal year’s guidance.

This is one of the best REITs in the world, but you wouldn’t know that by the valuation. In spite of Realty Income’s size and quality, the valuation is pretty humble. The forward P/FFO ratio is 15.7, based on this fiscal year’s guidance.

Since this is analogous to a P/E ratio on a normal stock, we can see just how undemanding the valuation is. There’s also the P/CF ratio, which, at 16.2, compares quite favorably to its own five-year average of 19.7. There’s almost nothing to dislike here about the business, and the valuation makes it even more likable.

We analyzed the REIT not long ago, showing why Realty Income’s shares have an estimated intrinsic value of $72.62/each. Those shares are currently trading hands for about $65/each. That looks like a favorable disconnect to me. And it’s one you ought to consider taking advantage of.

My fifth dividend growth stock pick for December 2022 is Texas Instruments (TXN).

Texas Instruments is a designer and manufacturer of semiconductors and various integrated circuits. Yet another tech company? Well, the tech-heavy Nasdaq is down more than the broader market in 2022. And, like I already mentioned, I see short-term volatility as a long-term opportunity.

So it’s clear that one should think about jumping on that tech weakness by focusing on the highest-quality tech companies. Texas Instruments is one such company. This is a preeminent analog chip operation. We can spot evidence of that preeminence in the company’s consistent and high growth: Texas Instruments has grown its revenue at a CAGR of 4.1% and its EPS at a CAGR of 20.8% over the last decade.

Strong, consistent business growth has led to strong, consistent dividend growth. This is a company that has increased its dividend for 19 consecutive years. Despite the perceived uncertainty around tech, Texas Instruments has been anything but uncertain when it comes to paying a safe, growing dividend.

The 10-year DGR is 21.1%, which is right in line with EPS growth over that period. And the stock offers a pretty compelling yield of 2.9% to go with that. With a payout ratio of 52%, which is almost a perfect balance between retaining earnings for growth against returning cash to shareholders, this looks like a very healthy dividend that has a lot more growth ahead.

The 10-year DGR is 21.1%, which is right in line with EPS growth over that period. And the stock offers a pretty compelling yield of 2.9% to go with that. With a payout ratio of 52%, which is almost a perfect balance between retaining earnings for growth against returning cash to shareholders, this looks like a very healthy dividend that has a lot more growth ahead.

This is a wonderful business. But the valuation doesn’t seem to be properly reflecting that. This is a stock that usually gets a healthy premium. But we’re now looking at a discount.

For perspective, its five-year average P/E ratio is a rather lofty 23.9. The current P/E ratio is 18.1. That’s below the broader market’s earnings multiple. What I think we have here is an above-average business being sold for a below-average valuation. As a long-term dividend growth investor actively accumulating shares in world-class businesses, that kind of relationship between quality and value gets me very excited. Texas Instruments is at least worth a closer inspection here.

— Jason Fieber

Source: Dividends & Income