It’s been nearly three years since the onset of the global pandemic.

But it might not seem that way.

Why?

Well, some stocks are still behaving as if we’re in the middle of the crisis.

Their prices are well below where they were in early 2020, which could be leading to incredible opportunities.

There’s a simple question to ask: Has this business been permanently impaired by the pandemic?

If the answer is no, the pricing shouldn’t be compressed as if the answer were yes.

And if there’s a decoupling between business performance and stock performance, that’s your chance to take advantage.

This favorable decoupling can be powerful under ordinary circumstances.

But it can be especially powerful when dealing with high-quality dividend growth stocks.

These stocks represent equity in world-class enterprises paying reliable, rising dividends to their shareholders.

We’re talking about some of the best businesses on the planet.

Hundreds of examples can be found on the Dividend Champions, Contenders, and Challengers list.

This list contains invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

There’s a virtuous circle at play here.

There’s a virtuous circle at play here.

Shareholders expect their reliable, rising dividends.

Reliable, rising dividends require reliable, rising profits for funding.

And reliable, rising profits are the result of running great businesses.

This is why I’ve been buying high-quality dividend growth stocks for years, being extra aggressive when those favorable decouplings were present.

In doing so, I built my FIRE Fund.

This real-money portfolio produces enough five-figure passive dividend income for me to live off of.

I actually started living off of dividends years ago.

In fact, I retired in my early 30s.

In fact, I retired in my early 30s.

And my Early Retirement Blueprint shares exactly how I was able to do that.

A major aspect of my success relates to buying the right stocks at the right moments.

And that comes down to buying high-quality dividend growth stocks when valuations are attractive.

See, price is what you pay, but it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Taking advantage of favorable decouplings between price and value on high-quality dividend growth stocks positions an investor for tremendous success, wealth, and passive dividend income over the long haul.

Of course, this would require one to first be able to spot such decouplings.

And that would mean one understands valuation.

But it’s not all that difficult.

My colleague Dave Van Knapp penned Lesson 11: Valuation in order to help you with this.

Part of an overarching series of “lessons” on the dividend growth investing strategy, it lays out a valuation template that can be easily applied to almost any dividend growth stock.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Realty Income Corp. (O)

Realty Income Corp. (O)

Realty Income Corp. (O) is a real estate investment trust that leases freestanding, single tenant, triple-net-leased retail properties.

Founded in 1969, it’s now a $39 billion (by market cap) real estate titan that employs nearly 400 people.

Their portfolio of over 11,700 properties is diversified across the US, Puerto Rico, Spain, and the UK.

The company serves more than 1,100 clients operating across 79 different industries.

As of the end of September 2022, the property portfolio has an occupancy rate of 98.9%.

Real estate is great.

Like the old saying about land goes, “They’re not making it anymore.”

Other than small reclamation projects, the usable land we have now is all we’ll ever have.

And those who can leverage this situation by putting up highly profitable properties on the limited land set themselves up to prosper.

If you can secure well-located properties, then rent them out to willing and able tenants, you’ve got yourself a cash cow.

However, this is easier said than done.

Real estate isn’t so great in the sense that it’s extremely difficult, expensive, and time consuming to actually do this.

Becoming your own landlord involves scouting, lining up financing, studying comps, closing, leverage, finding tenants, managing properties, etc.

And that’s not even getting into how hard and risky it is to scale this on your own.

Enter Realty Income.

When you buy shares in Realty Income, you instantly own a slice of a heavily diversified portfolio of commercial properties that already have paying tenants installed.

You get to become a scaled-up landlord… without doing any of the heavy lifting.

None of the “broken toilet” phone calls at midnight; Realty Income handles it for you, all while sending you your dividend check every month, which is steadily rising every year.

What’s great about Realty Income’s business model is the nature of a commercial triple-net lease – it’s a lease agreement on a property whereby the tenant agrees to pay all of the expenses of the property, most notably including real estate taxes, building insurance, and maintenance.

This greatly reduces Realty Income’s overhead.

Moreover, Realty Income leases its properties to some of most well-capitalized and successful tenants a landlord could possibly hope for.

Their top tenants include the likes of Dollar General Corp. (DG) and FedEx Corporation (FDX).

Diversification across tenants, industries, and geographies, and maintaining a high level of quality, sets Realty Income up for continued prosperity.

That means growth across its revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

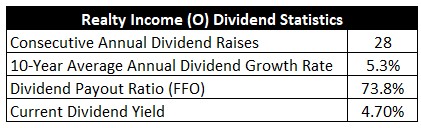

To date, the company has increased its dividend for 28 consecutive years.

Yes, Realty Income is an esteemed Dividend Aristocrat.

In fact, it’s one of the few Dividend Aristocrats that’s a REIT.

The 10-year dividend growth rate is 5.3%.

The 10-year dividend growth rate is 5.3%.

Not huge growth.

But the reason to own a slice of this business is right in its name.

It’s all about income.

Indeed, the stock yields 4.7%.

And it’s not just income but monthly income – Realty Income pays its dividend monthly, which is akin to collecting a monthly rent check.

Realty Income is so known for this, it’s actually trademarked its moniker: The Monthly Dividend Company®.

This yield, by the way, is 40 basis points higher than its own five-year average.

With a payout ratio of 73.8%, which is quite reasonable for a REIT, we have what appears to be a well-covered dividend.

A Dividend Aristocrat that’s paying a large, monthly dividend is something that’s hard to not love.

Revenue and Earnings Growth

As lovable as all of this might be, these dividend metrics are mostly looking backward.

However, investors must risk today’s capital for tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will later be instrumental when it comes time to estimate intrinsic value.

I’ll first show you what this company has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then uncover a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this manner should give us the ability to draw reasonable conclusions about where the business might be going from here.

Realty Income moved its revenue from $485 million in FY 2012 to $2.1 billion in FY 2021.

That’s a compound annual growth rate of 17.7%.

This is obviously very impressive at first glance; however, we have to remember that REITs fund growth via debt and equity issuances.

Furthermore, Realty Income’s recent merger with VEREIT moved up revenue in a meaningful way.

With a REIT, you really have to look at profit growth on a per-share basis.

And when assessing profit for a REIT, it’s imperative to look at funds from operations instead of normal earnings.

FFO is a measure of cash generated by a REIT, which adds depreciation and amortization expenses back to earnings.

Realty Income grew its FFO/share from $2.02 to $3.39 over this period, which is a CAGR of 5.9%.

This number, which is certainly very solid, is a more accurate reflection of Realty Income’s growth profile.

Noticeably, we can see that dividend growth and FFO/share growth lined up really well over the last decade, showing just how prudent and thoughtful management has been.

Looking forward, CFRA currently has no projection for Realty Income’s FFO/share growth over the next three years.

This is a shame, as I do like to compare the proven past up against a future forecast.

That said, we can draw some reasonable conclusions in other ways.

CFRA does estimate FY 2022 FFO/share to come in at $4.04, and their estimate for FY 2023 FFO/share is at $4.13.

This is supported by Realty Income’s own FY 2022 guidance, which calls for $4.03 in FFO/share at the midpoint.

This kind of bottom-line growth would represent a very nice acceleration in growth off of the historical mid-single-digit level.

Some of this does have to do with the sizable VEREIT acquisition, which should improve Realty Income’s growth and resiliency.

Regarding this, CFRA notes the following: “We also think [Realty Income’s] resiliency to a slowdown in consumer spending (possible given current high inflation, rising interest rates, and geopolitical risks) is underestimated by investors. The company has a long history of high occupancy rates, along with stable, growing dividend payments. We believe the recently completed VEREIT merger, increasing [Realty Income’s] enterprise value to $57 billion, will help to increase economies of scale while further reducing its exposure to theaters.”

The broadening out of the property portfolio is an important point, which CFRA notes again: “[Realty Income’s] tenant diversification has also improved, with their top 10 clients accounting for 27.6% of annualized rent in Q3 2022, down from 28.1% in Q2 2022 and 29.4% in Q4 2021.”

And this improvement has also bled down into occupancy, which CFRA illuminates: “Occupancy remained strong in Q3, but flat Q/Q at 98.9% – still the highest occupancy in 10 years – while [Realty Income’s] releasing recapture rate was a healthy 108.5%. We forecast occupancy will remain above its historical average of 98% into 2023 due to the company’s desirable property locations and high non-discretionary retailer demand.”

I want to expand on this occupancy point a bit.

Realty Income ended FY 2019 with 98.6% portfolio occupancy.

Realty Income’s current occupancy rate is 98.9%.

The stock was ~$80 in early 2020.

The stock is now ~$63.

Realty Income has gotten better in almost every possible way over the last 2.5 years, with higher occupancy being another key piece of evidence of this, but the stock has fallen by 20% over that period anyway.

If that kind of disconnect isn’t advantageous, I’m not sure what is.

Currently, interest rates are rising in an effort to curb demand and fight inflation.

While rising rates harm the firm, many of the long-term contracts have rent escalators built in.

Plus, inflation makes the existing real estate portfolio that much more valuable and difficult to replicate.

I believe Realty Income is still quite capable of producing its 5%+ annual dividend growth rate, with some higher-than-average dividend raises quite possible over the next few years.

With the stock’s starting yield at nearly 5%, this kind of setup should be especially compelling for income-oriented dividend growth investors.

Financial Position

Moving over to the balance sheet, Realty Income has a rock-solid financial position.

The REIT has $43.1 billion in total assets against $18 billion in total liabilities.

Realty Income’s credit ratings are well into investment-grade territory: A3, Moody’s; A-, S&P Global.

Moreover, many of the company’s top tenants have their own investment-grade credit ratings.

Realty Income’s combination of triple-net leases and a diversified roster of top tenants has led to one of the best track records in all of commercial real estate.

And the company’s deep expertise, long-term contracts, and massive scale give it durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Real estate demand is cyclical, and the financial health of its tenants could sour in a prolonged recession.

A REIT’s capital structure relies on external funding for growth, which exposes the company to volatile capital markets and interest rates.

Higher interest rates can hurt the company twice over: Debt becomes more expensive, and equity can become more expensive (because income-sensitive investors have alternatives, which pressures the stock).

A recession can also hurt the company twice over: Demand for real estate can cool, and equity issuances after a drop in the stock’s price would come at a higher cost.

Any wholesale changes in physical retail could hamper long-term growth.

The company’s scale is an advantage, but it also introduces questions around growth and the law of large numbers.

I see appreciable risks here, but I see those risks as part of a very attractive total package.

And the stock’s 16% drop from its recent high has made this total package look even more attractive by virtue of the valuation…

Stock Price Valuation

The stock is trading hands for a forward P/FFO ratio of 15.7, based on this fiscal year’s guidance.

This is analogous to a P/E ratio on a normal stock, showing just how low the valuation has become.

Also, the P/CF ratio of 16.2 is well off of its own five-year average of 19.7.

And the yield, as noted earlier, is noticeably higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 5.5%.

This kind of growth is at the low end of what I ordinarily allow for.

But this kind of expectation is quite reasonable, in my view.

The company’s demonstrated bottom-line and dividend growth over the last decade have both been in excess of 5% annually.

Recent guidance indicates an acceleration in bottom-line growth off of its base.

And the payout ratio remains flexible enough to allow for dividend growth to at least track bottom-line growth.

However, the company’s size may start to work against them, interest rates are on the rise, and a US recession could be in the offing.

Overall, I do believe Realty Income is highly capable of growing the business and the dividend at this undemanding mid-single-digit rate over the years to come.

The DDM analysis gives me a fair value of $69.86.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I don’t see my valuation model as aggressive at all, yet the stock looks undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates O as a 5-star stock, with a fair value estimate of $78.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates O as a 4-star “BUY”, with a 12-month target price of $70.00.

I landed within pennies of where CFRA is at on this one. Averaging the three numbers out gives us a final valuation of $72.62, which would indicate the stock is possibly 15% undervalued.

Bottom line: Realty Income Corp. (O) has built up a high-quality real estate empire with impressive scale and diversification. Its structure reduces both overhead and risk, and it positions shareholders very favorably. With a market-smashing yield, mid-single-digit dividend growth, nearly 30 consecutive years of dividend increases, a flexible payout ratio, and the potential that shares are 15% undervalued, long-term dividend growth investors looking for a monthly dividend from a reliable Dividend Aristocrat should definitely have this name on their radar.

Bottom line: Realty Income Corp. (O) has built up a high-quality real estate empire with impressive scale and diversification. Its structure reduces both overhead and risk, and it positions shareholders very favorably. With a market-smashing yield, mid-single-digit dividend growth, nearly 30 consecutive years of dividend increases, a flexible payout ratio, and the potential that shares are 15% undervalued, long-term dividend growth investors looking for a monthly dividend from a reliable Dividend Aristocrat should definitely have this name on their radar.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is O’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 70. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, O’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income