2022 was supposed to be a great year for Blue Apron (NYSE:APRN) stock. In December 2021, the firm announced a deal with Amazon (NASDAQ:AMZN) to run on Alexa smart speakers. Analysts were projecting revenues of $535 million for the year and APRN stock was trading at over $6.

Fast forward 10 months and little has gone well for the meal delivery firm. Consumer belt-tightening, high inflation and declining meal delivery interest mean Blue Apron will struggle to produce even $500 million in revenue. And unless the firm’s cash generation improves, management will likely find themselves bankrupt by 2024.

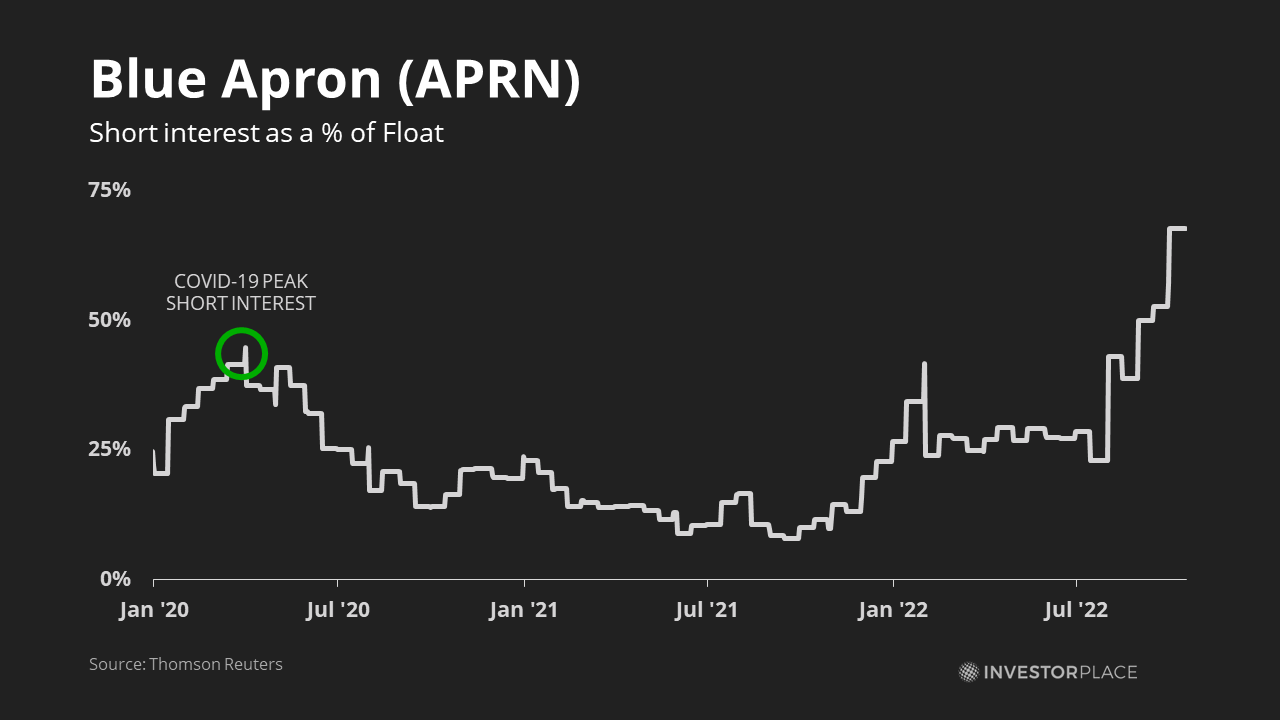

Yet, these factors have turned Blue Apron into a dangerous short bet. Short interest now sits at almost 70% of float — the highest of any major American stock. And collapsing value traded means that retail investors yelling “fire” could spark a panic for the exits.

APRN Stock: The Next Revlon?

Retail investors have squeezed bankrupt and near-bankrupt firms before. In June, shares of bankrupt cosmetics firm Revlon (NYSE:REV) jumped from $1.08 to over $8 as investors speculated about the 90-year-old firm’s residual value. And bankrupt Sears (OTCMKTS:SHLDQ) has seen its stock double at least eight times in the past five years before sinking back down again. When share prices border on zero, the slightest move can send shares soaring on a relative percentage basis.

Today, Blue Apron has fallen into the same category. Low profitability and high marketing expenses mean the company could burn up to $40 million in cash every quarter through 2023. That rate could deplete its cash on hand in less than three months. Only fundraising and share issuances have kept the firm alive.

Interest in meal delivery kits has also declined, with searches down 68% since 2018, according to tracking site ExplodingTopics. The number of Blue Apron customers has dropped 7% to 349,000 this year, compounding an 8% reduction in orders per customer.

APRN stock has collapsed as a result. The firm has lost two-thirds of its value this year and shares now trade for 0.16X forward price-to-sales. It’s now in the cheapest 2% of all U.S. stocks by that metric, according to data from Thomson Reuters.

But near-zero prices, high short interest and low float also set the stage for a short squeeze. Blue Apron now has 5.5 million shares sold short, according to SEC data. And though the firm technically has 34.8 million shares outstanding, in practice only around 8 million of those shares are available for trading. Majority stakeholders RJB Partners, DPH Holdings and the Salzberg family collectively own most of the rest.

How High Can Blue Apron Go?

How High Can Blue Apron Go?

Short-sellers are thus playing with fire. Shares of Blue Apron could theoretically rise 10X or more if large purchases trigger an avalanche of short covering since rising prices force short sellers to buy back shares to rebalance losing positions. That puts upward pressure on prices, forcing more short-sellers to cover, and so on.

These factors are magnified by a hyperactive market for APRN stock. Since September, an average of $37 million shares changes hands per day — a stunning amount for a company with only $20 million worth of freely floating shares. If the number of sellers suddenly dries up, the buying pressure alone could send APRN above $20 as it did in March 2020.

The company also scores an A+ on my quantitative scoring system for its cheap value and negative momentum — two factors that are associated with outperformance over the following months. The same system also flagged Bed, Bath & Beyond (NASDAQ:BBBY) in May before shares spiked 150% in a meme-fueled rally. APRN shares are primed to do the same.

Be warned: Shares of Blue Apron will still likely go to zero over the longer term. The company has failed to create a cash-generating business in the hyper-competitive meal delivery market, and potential buyers like Walmart (NYSE:WMT) and Amazon will more likely partner with an existing food distributor than saddle themselves with APRN’s high costs in an acquisition. The rise of food delivery businesses from Uber (NYSE:UBER) and DoorDash (NYSE:DASH) also makes a buyout less likely.

Nevertheless, short sellers are undeniably playing with fire. For those who truly want to bet on Blue Apron’s demise, it’s far safer to buy 2024 puts in the $3-$4 strike range and wait for the firm to eventually vanish from the stock market.

Because unless you have the appetite to blow up a trading account, shorting APRN’s shares today is risky at best.

— Thomas Yeung

Legendary fund manager Louis Navellier – a man Forbes calls "the king of quants" – is going "ALL-IN" on this game-changing AI technology. He says, "This is the culmination of everything you've been reading about AI for the last 60 years."Get the details...

Source: Investor Place