On Thursday, Wedbush analyst Dan Ives reiterated his $215 target price for Salesforce (NYSE:CRM), re-crowning the software firm as the Dow Jones stock with the highest implied upside.

For many first-time investors, these target prices are often irresistible.

Walmart (NYSE:WMT) at $169… Intel (NASDAQ:INTC) at $55… Goldman Sachs (NYSE:GS) at $456…

These numbers provide a rare bit of clarity into uncertain markets. If 35 well-paid analysts agree on a favorite stock, then they can’t all be wrong… can they?

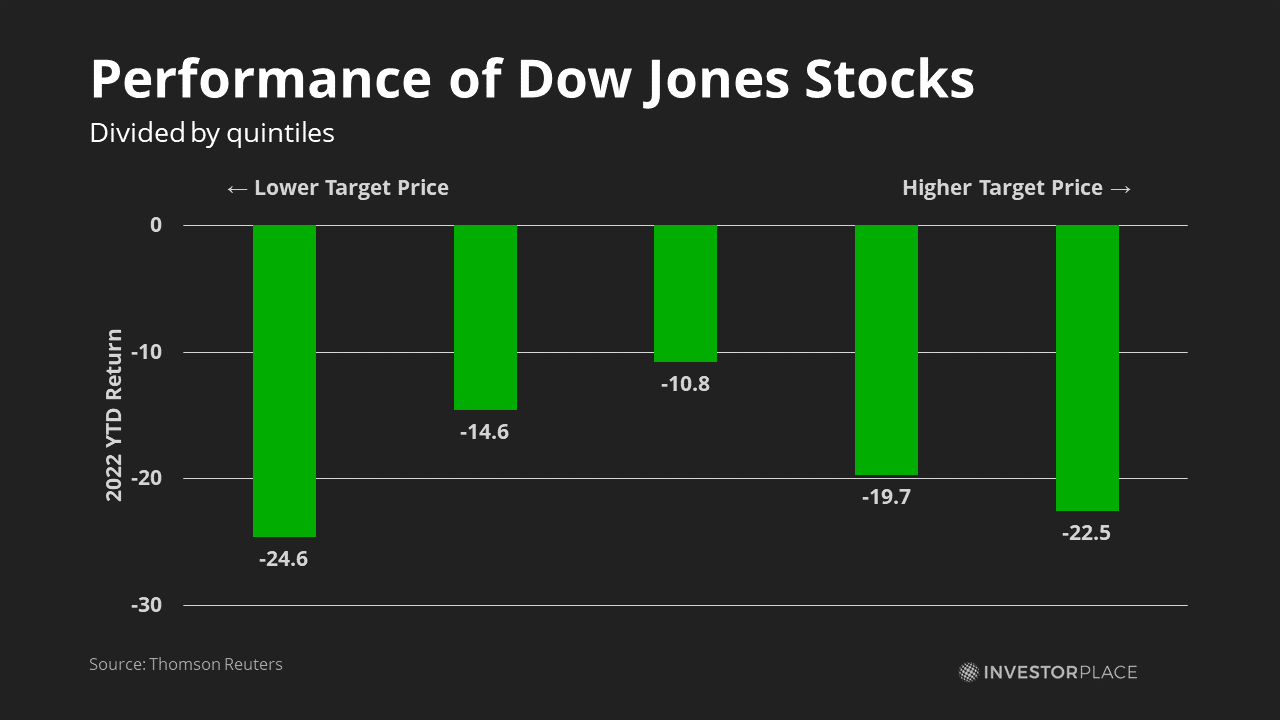

But my long-time readers will know that analyst price targets are poor predictors of company performance. Below, I’ve taken all stocks in the Dow Jones index and divided them into quintiles based on their broker-implied upsides in January 2022.

The results are much like watching a high school valedictorian fall off the stage. The stocks with the highest relative target prices in January, which included Boeing (NYSE:BA), Disney (NYSE:DIS) and Visa (NYSE:V), would drop 22.5% over the following 10 months. Meanwhile, ho-hum companies in the middle quintile would do far better.

The results are much like watching a high school valedictorian fall off the stage. The stocks with the highest relative target prices in January, which included Boeing (NYSE:BA), Disney (NYSE:DIS) and Visa (NYSE:V), would drop 22.5% over the following 10 months. Meanwhile, ho-hum companies in the middle quintile would do far better.

Historical data shows a similar pattern of coin-toss luck. Bullish analysts got things right in 2021 and 2019 and failed to outperform in 2020.

The 10 Best Dow Jones Stocks to Buy Before Markets Recover

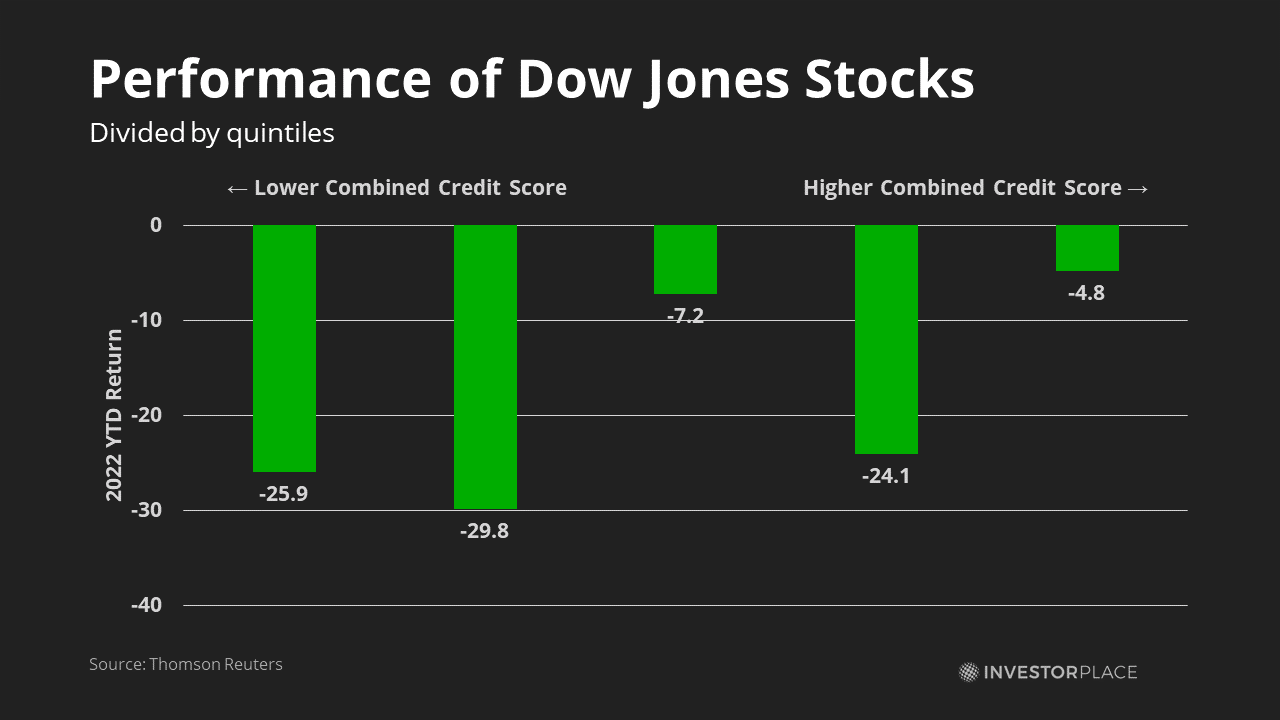

Instead, the best Dow Jones stocks to buy are often the ones that bond analysts like best. Rating agencies have little interest in pumping shares, since they’re not investment banks. And analysts are trained to remain disinterested in share prices, as you’ll quickly find if you ever meet one at a cocktail party.

This neutrality gives credit analysts an oddly powerful insight into stocks. It’s how I managed to pick out Hertz (NASDAQ:HTZ) shares for $2 before they rose 10X out of bankruptcy; when credit analysts start turning bullish on a near-bankrupt company, it’s a tell-tale sign that stock investors should pay attention.

Here’s the same analysis on Dow Jones stocks, using a standardized combined credit ranking. In 2022, the quintile of highest-credit Dow Jones companies outperformed the lowest quintile by 21.1%.

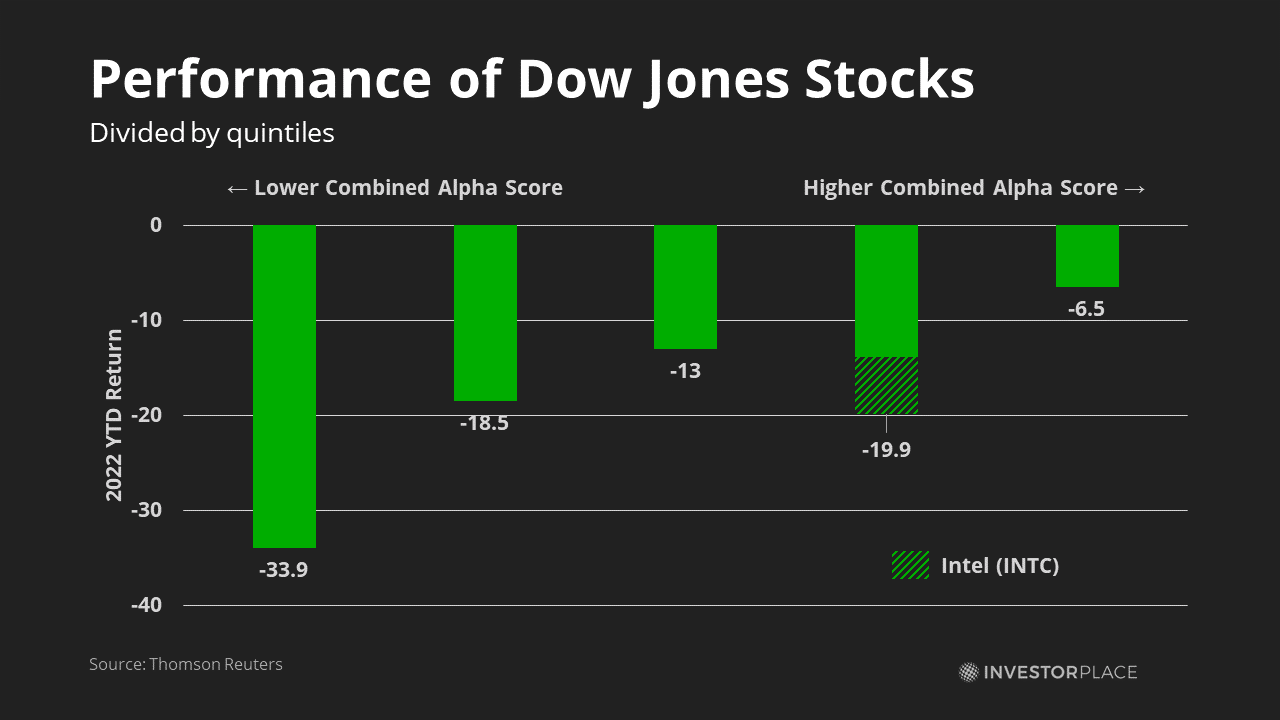

Investors can improve performance even further by overlaying an Alpha Model that also considers price momentum, revisions, valuations and earnings quality. Putting the massive losses at Intel aside for a moment (more on that later), stocks with high alpha scores have outperformed those with the lowest by 27.4% this year.

Investors can improve performance even further by overlaying an Alpha Model that also considers price momentum, revisions, valuations and earnings quality. Putting the massive losses at Intel aside for a moment (more on that later), stocks with high alpha scores have outperformed those with the lowest by 27.4% this year.

Alpha models, however, do have some drawbacks. Outliers like Intel can significantly underperform when non-financial factors are introduced. No quantitative model could have foreseen a $52.7 billion CHIPS Act or a semiconductor export ban — even though it’s perfectly clear to human investors. And quantitative models are only a starting point; these models can help tilt the odds 55-45 in our favor, and it’s up to us to get closer to 60-40.

Alpha models, however, do have some drawbacks. Outliers like Intel can significantly underperform when non-financial factors are introduced. No quantitative model could have foreseen a $52.7 billion CHIPS Act or a semiconductor export ban — even though it’s perfectly clear to human investors. And quantitative models are only a starting point; these models can help tilt the odds 55-45 in our favor, and it’s up to us to get closer to 60-40.

That brings us to a third element: Justified Value (JV). This is the output of a discounted cash flow (DCF) model, a powerful tool that calculates a company’s value based on its free cash flow.

Unlike target prices, justified values quickly incorporate information from credit markets. Downgrade International Business Machine’s (NYSE:IBM) shares to a B rating, for instance, and its JV immediately drops from $142 to $118 regardless of what Wall Street analysts say.

This makes justified value an integral element of analyzing stable stocks like those in the Dow Jones index. And by using a combination of alpha models, industry analysis and DCF modeling, we can quickly unearth the top Dow Jones stocks to buy before the market recovers.

Verizon (VZ)

- Justified Value: $112 (216% upside)

- Alpha Model Rank: 93

- Credit Rating: BBB+

The Dow Jones’ highest upside stock is Verizon (NYSE:VZ), a capital-intensive, low-return company that has underperformed the broader markets for the past two decades.

It’s also created an ultra-cheap stock with room to rise.

Net income at America’s largest telecom will likely stabilize in 2022 and grow by 7% next year from industry consolidation. If its recovery pattern continues as expected, Verizon’s justified fair value comes in at $112, a significant premium to the Street’s $50 target price. The company also scores a high Alpha model score.

Investors should obviously remain cautious. Verizon’s high justified value comes with the assumption that consolidation and 5G technologies will eventually transform the lackluster telecom sector into an average-performing one.

Credit markets are also only lukewarm about the sector’s historically poor performance. Yet, history tells us that turnaround industries are some of the top places to find high-performing stocks. If the telecom industry can follow the footsteps of rail, airlines, hotels and other recovering industries, it will be contrarian investors who will have the last laugh.

Dow Chemical (DOW)

- Justified Value: $94 (114% upside)

- Alpha Model Rank: 74

- Credit Rating: BBB+

The Michigan-based chemical manufacturer is a poster child for cheap stocks. Shares trade at 6.6X forward price-to-earnings (P/E), making it the least expensive company in the Dow Jones index by that metric. Its justified value of $94 suggests a 114% upside.

Dow’s high JV stems from its long history of profitability. The company has generated positive operating income in five of the past six years, and analysts are expecting EBIT to remain above $5 billion in 2023. Fitch Ratings awards the firm a “positive” outlook on its debt.

There are some reasons to stay cautious. Dow Chemical’s legal woes continue to hang heavily over the firm — in 2021, the company suffered another class-action lawsuit for its promotion of chlorpyrifos, a pesticide tied to brain damage. Thousands of Asbestos-related claims remain on Dow’s books; my DCF model assigns a 25% chance of a major financial hit within the next decade. But for investors seeking a gamble, Dow Chemical has the elements of a stock that historically performs.

Intel (INTC)

- Justified Value: $51.10 (101% upside)

- Alpha Model Rank: 63

- Credit Rating: P-1

Bearish sentiment has crushed Intel’s stock this year. The California-based semiconductor firm trades at a 12x price-to-earnings (P/E) ratio, giving it a 101% upside to its justified value.

The lofty justified value could take several years to achieve. Overinvestment in semiconductor manufacturing will leave the industry oversupplied through 2023, according to industry analysts. And Intel’s late start in GPU (graphics processing unit) chips leaves it at a significant disadvantage in AI (artificial intelligence) processing.

Nevertheless, Intel stands to receive between $10 billion to $15 billion from the CHIPS Act to reinvigorate its American manufacturing capacity. And as the firm catches up in GPUs and other niche technologies, investors will likely see this Dow Jones laggard as a winner again someday.

Walgreens Boots Alliance (WBA)

- Justified Value: $44.17 (38% upside)

- Alpha Model Rank: 67

- Credit Rating: Baa2

America’s second-largest drug retailer has a questionable financial history. In 2012 Walgreens bought U.K.-based Boots for $22 billion, creating a massive transatlantic headache for its managers. Analysts now reckon its U.K. assets are only worth around $8 billion. Its American business has also suffered severe margin compression.

These historical trends have turned Wall Street analysts into permanent bears. 17 analysts rate the company a hold, while another 3 rate it a sell.

Yet, these scorecards are often poor predictors of future performance. Walgreens has the second-highest free cash flow yield behind Dow Chemical; the firm could generate $4 billion FCF by 2024. Plugging in these figures into a 3-stage DCF model creates a justified value of $44.17, suggesting that Wall Street analysts are still too bearish about brick-and-mortar businesses.

Cisco (CSCO)

- Justified Value: $48.50 (24% upside)

- Alpha Model Rank: 94

- Credit Rating: A1+

Cisco is one of the Dow Jones Index’s most dependable stocks. The networking firm has managed to earn positive net income every year since 2000, notching an average 19.7% net margin.

Shares of the California-based firm have fallen 36% this year over a semiconductor slowdown. Last Friday, Advanced Micro Devices (NASDAQ:AMD) warned that revenue would come in at least $1 billion below forecasts, putting further pressure on Cisco’s battered stock.

Yet, the data suggests that Cisco’s shares have fallen too far. CSCO’s justified value remains at $48.50, a 24% upside, and credit analysts remain relatively positive about the company’s outlook.

International Business Machines (IBM)

- Justified Value: $142.15 (21% upside)

- Alpha Model Rank: 91

- Credit Rating: P-2

Financial models naturally assume that companies eventually revert to the mean. High-returning firms like Amazon (NASDAQ:AMZN) eventually come down to earth, just as Dow Chemical (NYSE:DOW) and General Electric (NYSE:GE) once did.

The reverse is also true: Struggling companies often become average over the long run.

And that’s how IBM makes the list.

Since 2012, the IT provider has seen operating income shrink from $22.5 billion to $4.8 billion and revenues decline by almost half. A botched transition from PCs to services and the slow adoption of cloud computing have left the once-dominant firm far behind.

Despite that, IBM’s management still has some fight left. Analysts now believe the New York-based firm will grow operating income in the mid-single-digits through 2024, reversing years of steep declines. Its justified value thus comes to $142.15 — a rare case where the Street’s target price lands within striking distance of its fundamental value.

3M (MMM)

- Justified Value: $124.4 (14.2% upside)

- Alpha Model Rank: 47

- Credit Rating: A+

The Minnesota-based firm scores relatively poorly on its Alpha model for middling price momentum, muted insider interest, and average earnings quality. Its 30x P/E ratio leaves little room for deep-value investors to buy.

The data tells a different story. 3M’s high earnings power translates into extremely high cash flows; the company should generate $6.6 billion of free cash flow in 2022 and $6.6 billion by 2024. Even if you fade these cash flows down to $3 billion by 2040, the company’s fair value still comes in at $124.4, a 14.2% upside.

Microsoft (MSFT)

- Justified Value: $247.80 (9.8% upside)

- Alpha Model Rank: 54

- Credit Rating: P-2

Microsoft’s (NASDAQ:MSFT) stock has fallen in lockstep with the tech-heavy Nasdaq this year, shedding 30% of its value since January. In September, these steep declines finally pushed the tech giant’s shares below its justified value for the first time since March 2020.

Investors should consider buying in if they’re seeking a conservative place to park cash. Microsoft generates $68 billion in free cash flow annually, a figure that’s expected to rise to $89 billion by 2024. And because the firm has relatively low capital requirements, its cash flow could potentially increase through 2040 even as returns on capital invested declines from current levels of 28% down to a more “average” level of 14%.

Chevron (CVX)

- Justified Value: $172.0 (9% upside)

- Alpha Model Rank: 75

- Credit Rating: AA

I’ll admit to being torn about energy stocks. On the one hand, analysts like InvestorPlace’s Louis Navellier are right that energy stocks have major tailwinds going into 2023. It’s one of his favorite sectors to buy right now. The stock also has a justified value of $172, a 9% upside to current prices.

But energy stocks also have a history of significant crashes. High capital expenditures and low margins mean that few oil majors perform well over more extended periods. Falling oil prices also leave “stranded assets” of oil in the ground that are no longer profitable to pump. Canada’s oil sands contain millions of barrels of oil that are only profitable to extract if prices remain above $70.

That’s why I’m only cautiously recommending Chevron (CVX) as a diversification play. It’s the only energy stock left in the Dow Jones index, and its relatively low correlation of 0.42 with other Dow Jones stocks makes it an ideal firm to keep as ballast.

Disney (DIS)

- Justified Value: $101 (8.7% upside)

- Alpha Model Rank: 24

- Credit Rating: P-2

Finally, Disney makes the list with a justified value of $101. The LA-based firm has seen shares decline by almost 40% this year as investors have retreated from media stocks. Rival Netflix (NASDAQ:NFLX) has fallen even further.

These declines have finally made Disney a stock to watch. The firm generates predictably high cash flows, driven in large part by its diversified revenue streams spanning theme parks, sports and movies. The firm now has 44.5 million U.S. subscribers to its Disney+ streaming service.

Conclusion: Why Target Prices Fail… And Quant-Based Investing Succeeds

Target prices are a historically poor predictor of stock performance.

Firstly, analyst target prices often resemble wishful thinking. My models suggest Walmart’s stock is worth closer to $129… not $169 as analysts seem to think. When an investment bank relies on fee income from corporations, there’s a strong incentive to give “buy” ratings to your clients. Only 1 company in the entire S&P 500 has an average “sell” rating by analysts.

Secondly, target prices are essentially negative momentum strategies. Falling share prices increase the expected upside of stocks, all else equal. And as I’ve long shown in my data, these negative-momentum strategies are losing ones; investors are better off buying winning companies.

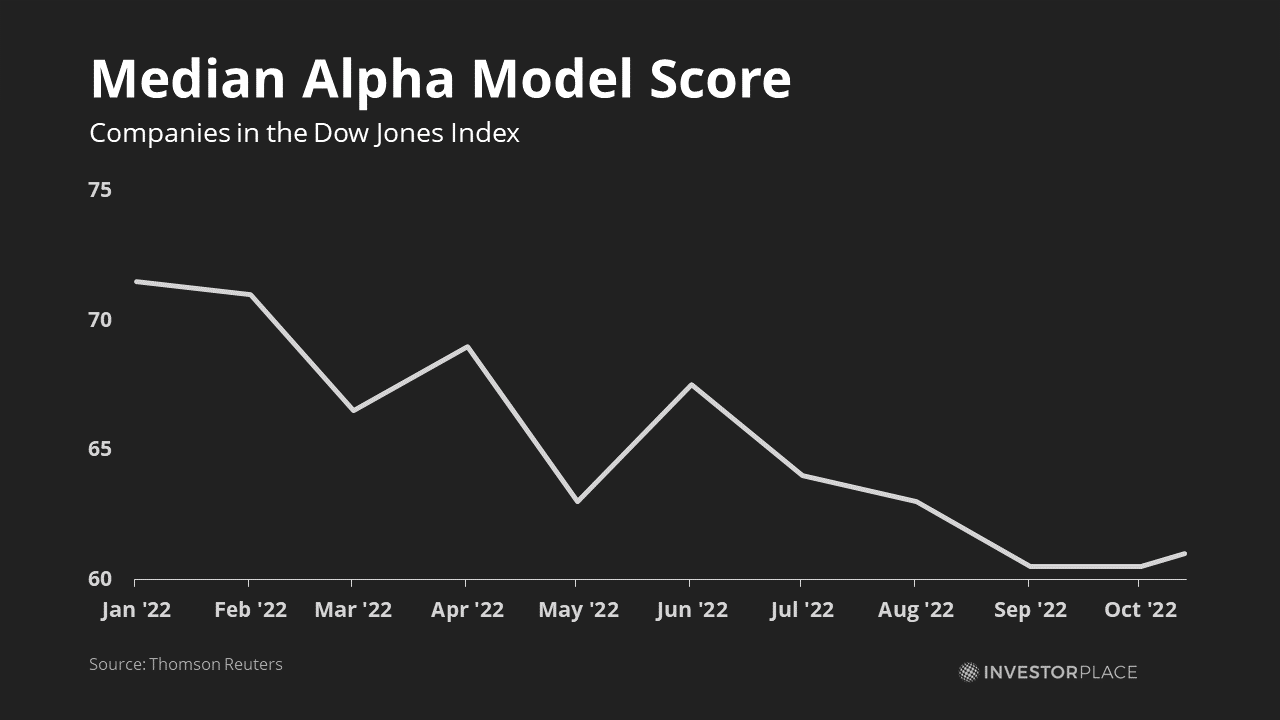

Meanwhile, quant-based investing has no qualms in cutting price targets the moment company outlooks deteriorate. The median Alpha model score for Dow Jones stocks has fallen from 72 to 62 this year.

As markets begin to recover, it’s these fast-moving strategies that should come out ahead.

As markets begin to recover, it’s these fast-moving strategies that should come out ahead.

— Tom Yeung

If you're buying rare earth or other critical mineral stocks, you're already one step behind - because we believe that political insiders in Washington are preparing to buy a whole new group of stocks, which could begin soaring 500%+ just days from now. The man once ranked in 2020 as America's #1 stock picker is doing something extraordinary and giving away the name and ticker of every single stock that could be next. Everything you need to know is here.

Source: Investor Place