The S&P 500 is down 23% YTD as I write this. But it’s been anything but a straight line down.

It’s been a total roller coaster. Except the stock market roller coaster isn’t quite as fun as a real roller coaster. Or is it?

If you have the proper temperament, and if you maintain a long-term perspective, this kind of volatility is fantastic. Why?

Well, it allows you to buy high-quality dividend growth stocks for lower prices. And, all else equal, lower prices result in higher yields. That means more passive dividend income on the same invested dollar.

As someone who lives off of dividend income, I can tell you that every dividend dollar counts. Look, lower prices and lower valuations serve you in every way possible. Not just on the dividend income front, either – you’re also typically looking at greater long-term total return prospects. It’s more for less.

Seeing short-term volatility as a long-term opportunity is something that helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint. If you’re interested, you can download a free copy of my Early Retirement Blueprint.

As great as this volatility is, though, not every business and not every stock is the same. Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for October 2022.

Ready? Let’s dig in.

My first dividend growth stock pick for October 2022 is Home Depot Inc. (HD).

Home Depot is the world’s largest home improvement retailer. Home Depot is a great play on the American Dream. After all, a big aspect of the American Dream is homeownership. And what do we know about houses? They’re physical structures that slowly deteriorate and need constant repairs and upkeep.

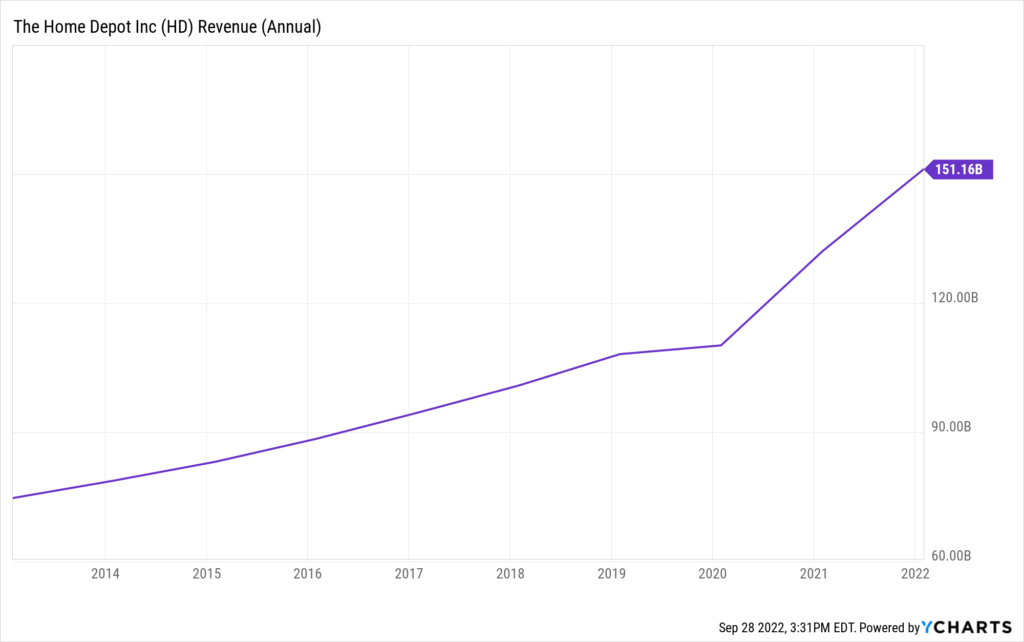

Well, that’s where Home Depot comes in, providing the products homeowners need in order to maintain and upgrade their homes. What makes Home Depot special in this regard is the way in which they disproportionately benefit from this, as they’re the clear leader within a powerful duopoly. This explains why Home Depot was able to compound its revenue at an 8.1% rate and its EPS at an annual rate of 20% over the last decade.

Home Depot oughta be called “Dividend Depot”.

Home Depot oughta be called “Dividend Depot”.

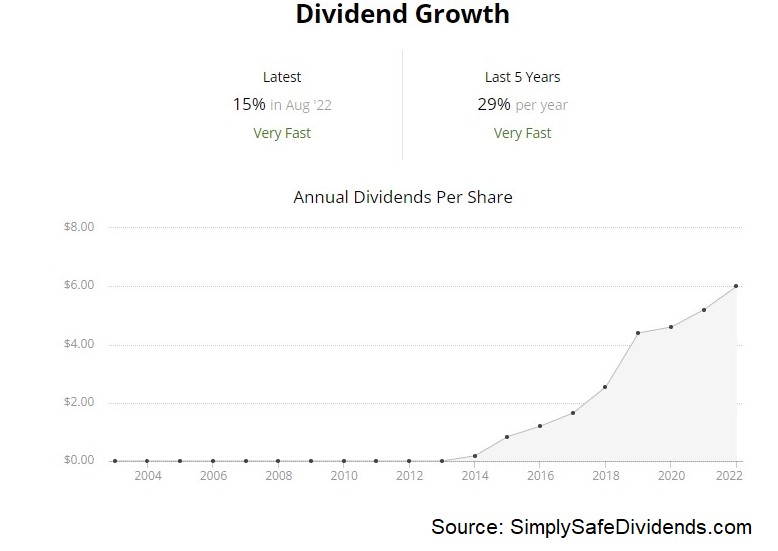

This company is money when it comes to depositing growing dividends right into its shareholders’ depots. The company has increased its dividend for 13 consecutive years. The 10-year dividend growth rate is a monstrous 20.3%, which lines up almost perfectly with EPS growth, showing incredible control from management.

That kind of high dividend growth rate usually means you have to sacrifice yield. But not in this case. The stock yields a market-beating 2.8%, which is 60 basis points higher than its own five-year average. And with a payout ratio of 46.7%, I suspect this dividend is headed a lot higher over the years to come.

That kind of high dividend growth rate usually means you have to sacrifice yield. But not in this case. The stock yields a market-beating 2.8%, which is 60 basis points higher than its own five-year average. And with a payout ratio of 46.7%, I suspect this dividend is headed a lot higher over the years to come.

Big growth, great dividend, and an attractive valuation.

That’s right. From every possible angle, this stock looks materially undervalued to me. The stock’s P/E ratio of 16.7, which is substantially lower than its own five-year average of 22.9, is Exhibit A. We will have a video coming out very soon that will fully analyze the business, and this article today shows why the estimate for the firm’s intrinsic value comes out to almost $350/share. Shares are currently trading hands for about $270/each. That’s a lot of possible upside on one of the best and most well-known retailers on the planet. I think it’s a good time to consider putting Home Depot shares in your depot.

My second dividend growth stock pick for October 2022 is Lam Research Corporation (LRCX).

Lam Research is is a major manufacturer of equipment used in the fabrication of semiconductors. It’s not hard to understand why Lam Research has been so successful. Semiconductors – you know, the chips we need to power almost everything in our lives at this point – cannot be manufactured without the equipment that Lam Research provides.

There are only a few companies in the world that are manufacturing the highly specialized equipment used in the fabrication of semiconductors. That combination of necessity and rarity has catapulted Lam Research’s growth into the stratosphere – we’re talking about a 19% CAGR for revenue and a 54.3% CAGR for EPS over the last 10 years.

Massive business growth has led to massive dividend growth.

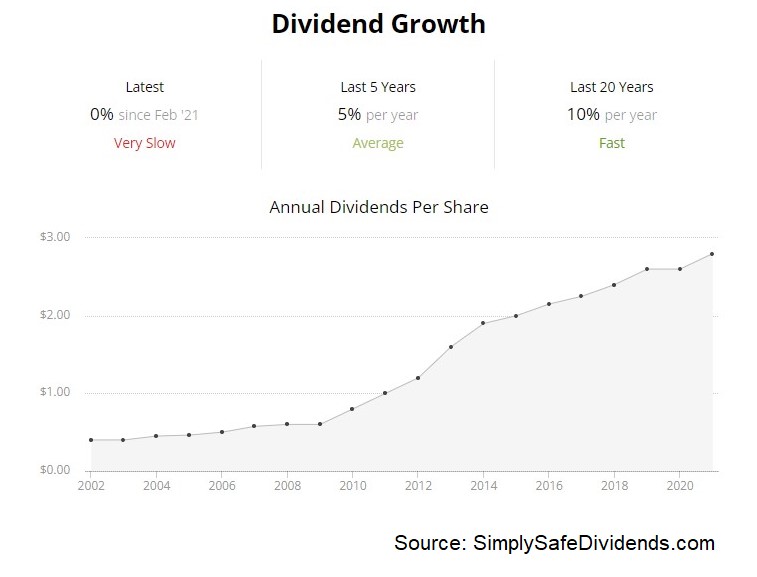

Lam Research’s dividend growth track record of eight consecutive years is still relatively short. But what a start they’re off to. The five-year dividend growth rate is an eye-popping 35.1%. Now, you’re pretty much never going to get a super high yield when a growth rate is off the charts like this.

Lam Research’s dividend growth track record of eight consecutive years is still relatively short. But what a start they’re off to. The five-year dividend growth rate is an eye-popping 35.1%. Now, you’re pretty much never going to get a super high yield when a growth rate is off the charts like this.

The stock’s lowish yield of 1.8% isn’t surprising. But this is compounder, not an income play. A super low payout ratio of only 21.1% indicates to me that a lot more compounding is in the cards for Lam Research and its shareholders.

This is a stock that’s rarely cheap. But I think it has dipped into cheap territory. And, you know, the word “dipped” – it’s an understatement. The stock is down nearly 50% this year. If you’re an older investor who’s trying to sell stock to live off of, that’s probably a bummer.

But if you’re a younger dividend growth investor who’s still accumulating stock and looking to live only off of the growing dividends your shares provide for you, this could be a fantastic opportunity to buy in for the long term. Our recent full analysis and valuation video on Lam Research showed why the business could be worth just under $600/share. The stock is currently sitting at about $380. I’d argue we have a huge gap between price and value here. Don’t forget about Lam Research.

But if you’re a younger dividend growth investor who’s still accumulating stock and looking to live only off of the growing dividends your shares provide for you, this could be a fantastic opportunity to buy in for the long term. Our recent full analysis and valuation video on Lam Research showed why the business could be worth just under $600/share. The stock is currently sitting at about $380. I’d argue we have a huge gap between price and value here. Don’t forget about Lam Research.

My third dividend growth stock pick for October 2022 is Omnicom Group Inc. (OMC).

Omnicom is an advertising, marketing, and corporate communications company. Omnicom flies way under the radar. But that’s okay. Some of my best investments have been in businesses that few people have ever heard of.

I’ve never been in it to win popularity contests. I’ve been in it to win financial freedom.

Despite being a business that few are familiar with, Omnicom continues to do well by being the 21st-century marketing company for 21st-century clients, managing corporate messaging in a world in which the control over information dissemination has become more important than ever.

Omnicom’s revenue is roughly flat over the last decade, partly because of the huge hit from the pandemic, but the company was still able to put up a 6.8% CAGR in its EPS over that time frame. Also under the radar is this company’s commitment to its dividend and the growth of it.

Omnicom has increased its dividend for 12 consecutive years. Sure, not the longest streak out there. But 12 years is no quick trip around the block, either. That’s actually quite a long time in the business world. It’s as long as I’ve been investing, and I feel like I’ve been at it for a while now.

The 10-year DGR is 11.2%, but more recent dividend increases have been modest. And I get that. The pandemic didn’t help them. But the most recent dividend increase was more than decent, at 7.7%. Plus, the stock yields 4.4%. I mean, we’re in utility and REIT territory here with that yield. The payout ratio, which is 42%, shows a healthy dividend primed for more growth.

The 10-year DGR is 11.2%, but more recent dividend increases have been modest. And I get that. The pandemic didn’t help them. But the most recent dividend increase was more than decent, at 7.7%. Plus, the stock yields 4.4%. I mean, we’re in utility and REIT territory here with that yield. The payout ratio, which is 42%, shows a healthy dividend primed for more growth.

This stock has held up this year. Even so, I think it’s a bargain. The stock’s 14% YTD decline looks pretty good in the face of a 23% drop from the S&P 500. The thing is, this stock already looked cheap at the start of the year. In my opinion, it’s gone from cheap to cheaper. This stock has a P/E ratio of 10.3. We’re nearly in the single digits here.

That’s a very undemanding earnings multiple, even in this market. We actually highlighted Omnicom here on the YouTube channel not long ago, analyzing this business and estimating its intrinsic value at slightly over $87/share. Shares are currently trading hands for about $63 a piece. We could have a huge, huge discount on our hands here. Omnicom is at least worth a close look.

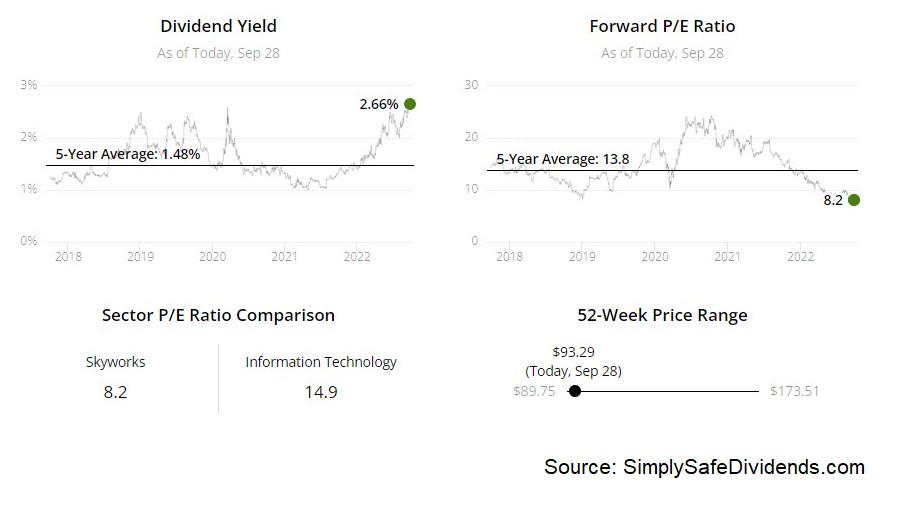

My fourth dividend growth stock pick for October 2022 is Skyworks Solutions Inc. (SWKS).

Skyworks Solutions is a large semiconductor company. Boy, it’s not often that I’ve got two tech companies on a concentrated list like this. But when tech has been absolutely slaughtered across the board, what do you expect? What’s happened with Skyworks Solutions is a bifurcation.

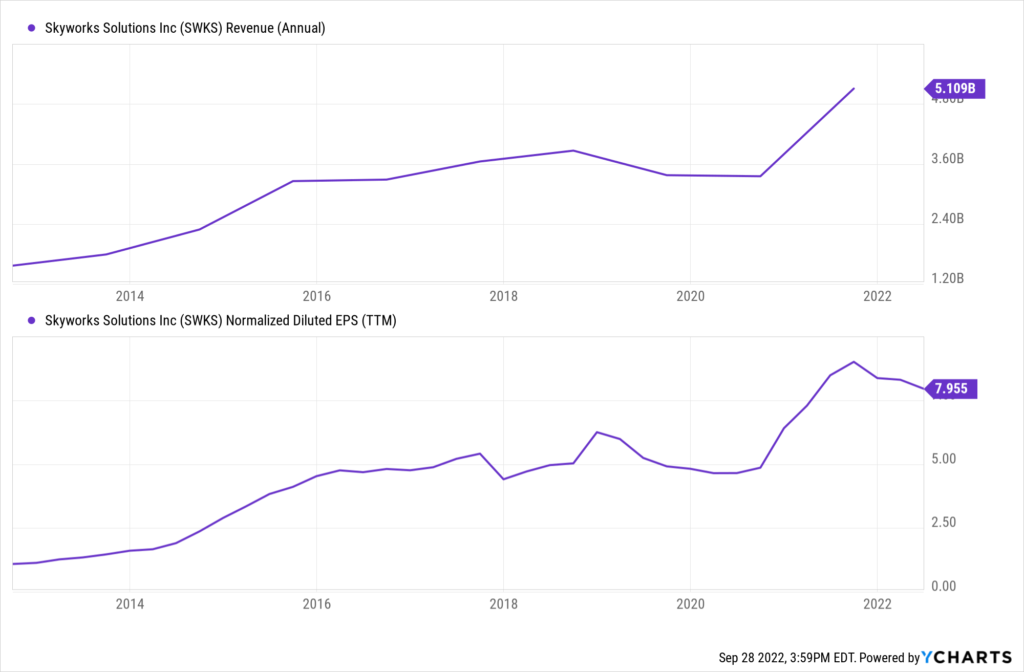

On one hand, the business continues to perform well, even this year. On the other hand, the stock has performed terribly this year. But a long-term dividend growth investor sees the advantage in something like this. Getting back to that business performance, Skyworks Solutions has been killing it – a 13.8% CAGR in revenue and a 26.9% CAGR in EPS over the last decade.

That kind of incredible business performance is why we have incredible dividend performance. If all you focus on is recent stock performance, you’re missing the far more important long-term performance metrics in the business and the dividend. Skyworks Solutions has increased its dividend for eight consecutive years.

That kind of incredible business performance is why we have incredible dividend performance. If all you focus on is recent stock performance, you’re missing the far more important long-term performance metrics in the business and the dividend. Skyworks Solutions has increased its dividend for eight consecutive years.

The five-year DGR is 14.9%. And homing in on the more recent action, the company increased its dividend by almost 11% in early August. Along with that double-digit dividend growth rate, the stock yields a comfortable 2.7%. This yield, by the way, is 120 basis points higher than its own five-year average. This dividend is protected by a low payout ratio of only 31.5%.

After seeing its stock price get cut in half, Skyworks Solutions looks very compelling here. This stock is sporting a P/E ratio of 11.8. To put that in perspective, its five-year average P/E ratio is 20.1. There is a huge cushion in place here. The market seems to be anticipating a massive drop in earnings that has yet to materialize.

We recently highlighted Skyworks Solutions, going through a full analysis of the business and estimating intrinsic value for the firm at just over $145/share. Valuation matters. Quite frankly, the stock looked expensive when it was flying high earlier this year at $175. On the other hand, it looks very compelling down here below $100. This name should be on your radar.

We recently highlighted Skyworks Solutions, going through a full analysis of the business and estimating intrinsic value for the firm at just over $145/share. Valuation matters. Quite frankly, the stock looked expensive when it was flying high earlier this year at $175. On the other hand, it looks very compelling down here below $100. This name should be on your radar.

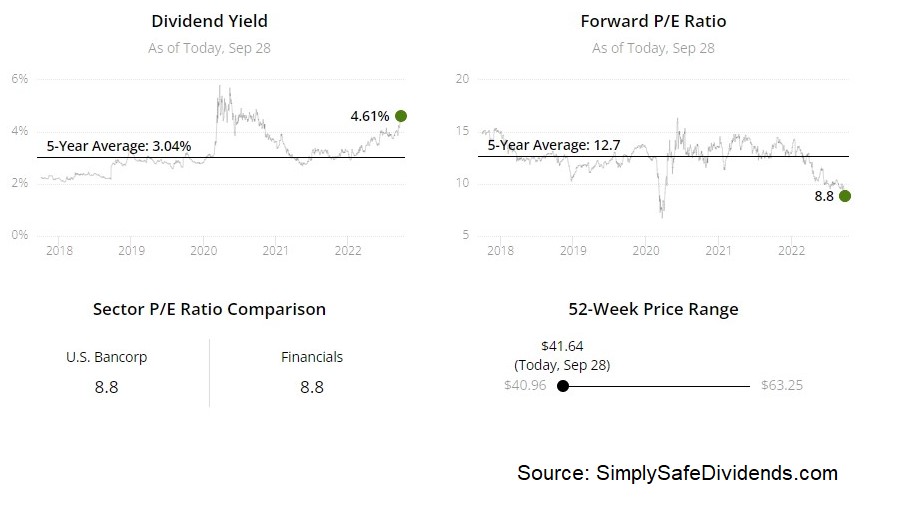

My fifth dividend growth stock pick for October 2022 is U.S. Bancorp (USB).

U.S. Bancorp is an American bank holding company. The banking business model dates back to antiquity. Why has it been so enduring? Society’s ongoing prosperity has been, and continues to be, dependent on banking and the flow of capital. Without banking, our way of life essentially collapses.

Banking is, quite literally, in the business of money. And since we’re all here because of money, that’s a pretty good match. Now, the last decade has been about as challenging as it could possibly get for banking. Still, U.S. Bancorp put up respectable numbers – a 1.3% CAGR for revenue and a 6.7% CAGR for EPS over the last 10 years. I think that proves how durable this business is.

You know what else is durable? The bank’s growing dividend. Some people like to point to the Great Financial Crisis as evidence that dividends from banks are not durable. But that was a once-in-a-lifetime type of event.

It’d be like if society called San Francisco unlivable after the 1906 earthquake. Bad things happen. You learn from them and become stronger.

It’d be like if society called San Francisco unlivable after the 1906 earthquake. Bad things happen. You learn from them and become stronger.

To that point, banks have arguably never been stronger or more durable than they are today. That translates to U.S. Bancorp and its dividend. The company has increased its dividend for 12 consecutive years, with a 10-year DGR of 11.1%. On top of that, the stock yields a market-smashing 4.7%. That’s incredible. And a payout ratio of 39.7% shows a well-covered dividend with plenty of leeway.

Banks, in general, are pretty cheap. But U.S. Bancorp looks especially appealing. Every single basic valuation metric I look at is well off of its own respective recent historical average. The P/E ratio of 9.5 is significantly lower than its own five-year average of 12.9. The P/B ratio is currently at 1.5. Its own five-year average is 1.7.

Banks, in general, are pretty cheap. But U.S. Bancorp looks especially appealing. Every single basic valuation metric I look at is well off of its own respective recent historical average. The P/E ratio of 9.5 is significantly lower than its own five-year average of 12.9. The P/B ratio is currently at 1.5. Its own five-year average is 1.7.

What I think separates U.S. Bancorp is their buildout of resilient fee-based businesses, as well as the stock’s gaudy yield. Our recent analysis and valuation video on this bank highlights both points and also goes on to show an estimate of intrinsic value at $57.54/share. In my view, U.S. Bancorp is a name to bank on.

— Jason Fieber

The old way of investing in tech giants is over. A NEW strategy unlocks 146X more income on the SAME underlying stocks (like Meta, Apple, and Amazon) -- WITHOUT options trading. Click here to uncover the NEW MAG-7 alternative.

Source: Dividends & Income