Inflation.

This word is so common right now, I think even parrots are starting to say it. Seriously, though, inflation is everywhere. Inflation is this invisible tax, slowly destroying your purchasing power.

So what do you do? You stand up and fight. As a dividend growth investor, this is actually a pretty easy thing to do. All you have to do is invest in high-quality companies that grow their dividends at rates that exceed the inflation rate.

If annual inflation is running at, say, 8%, you need your dividend income to grow faster than 8%. That keeps your purchasing power moving ahead of inflation.

Now, that’s speaking generally. Everyone is going to experience inflation differently, depending on a myriad of lifestyle factors. But this is a pretty good rule of thumb.

Getting paid while you sleep, via dividends, is great. But getting paid more while you sleep – even better. Today, I want to tell you about 6 dividend growth stocks that just increased their dividends.

Ready? Let’s dig in.

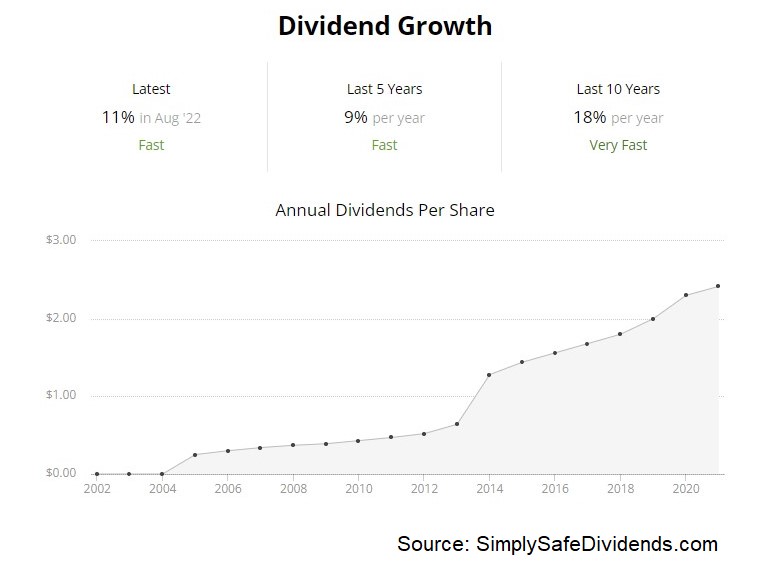

The first dividend increase I have to share with you is the one that was announced by Avnet Inc. (AVT).

Avnet just increased their dividend by 11.5%. The annual inflation rate in the US is running at 8.5%, based on the most recent report. At least, as I write this. Avnet just slam dunked on that number with this 11.5% dividend increase. If your expenses are rising by 8.5%, but your income is rising by 11.5%, you’re ahead of the game.

This is the 9th consecutive year of dividend increases for the electronic components company.

This is the 9th consecutive year of dividend increases for the electronic components company.

Avnet is flying under the radar, but their dividend increases should be garnering them some attention. The five-year dividend growth rate is 7.4%. But with inflation on the rise, Avnet has been stepping up to the plate with a flurry of dividend increases.

Indeed, Avnet increased the dividend by 8.3% back in February. So the dividend is actually up by 20.8% YOY. That’s huge. Plus, the stock yields a very respectable 2.7%. And with the payout ratio at only 16.7%, even after some recent supercharged dividend growth, the dividend remains healthy.

This stock’s low valuation makes it worth a look. Most basic valuation metrics indicate some cheapness. The P/E ratio of 6.2 is silly low and way off of its own five-year average of 19.4. The P/S ratio is only 0.2. While that is quite small in absolute terms, it’s actually right in line with its own five-year average.

I think what’s important to consider here with Avnet is whether or not its recent burst in growth across the business is sustainable or not. It’s being valued like it’s the same old business, but it could be a new business altogether. Its most recent Q4 FY 2022 report showed 21.9% YOY revenue growth and 84.8% YOY adjusted EPS growth. Avnet is interesting.

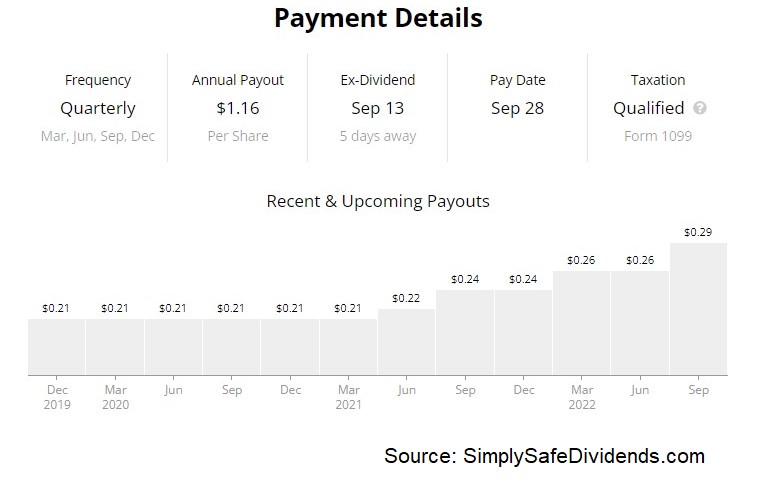

Next up, let’s quickly talk about the dividend increase that came in from Eastgroup Properties Inc. (EGP).

Eastgroup Properties just increased their dividend by 13.6%. Boom. Eastgroup Properties is putting the hammer down. I don’t think I ever once got a 14% pay raise from my boss back when I still had a day job. And even if I would have received such a pay raise, it would have been something that I had to work extremely hard for. But here, Eastgroup Properties shareholders did nothing other than hold shares in order to get a 13.6% pay raise. How awesome is that?

The industrial property real estate investment trust has now increased their dividend for 12 consecutive years. The five-year dividend growth rate is 11.1%, so there’s been some nice acceleration in dividend growth of late.

The industrial property real estate investment trust has now increased their dividend for 12 consecutive years. The five-year dividend growth rate is 11.1%, so there’s been some nice acceleration in dividend growth of late.

Along with that double-digit dividend growth, you get a yield of 3.1%. That is a very solid combination of yield and growth. The payout ratio is 72.5%, based on midpoint guidance for this fiscal year’s funds from operations per share. So we’ve got a dividend that’s easily covered.

This is a great REIT. And the valuation looks reasonable. With e-commerce in secular growth mode, and with logistics being an important part of the e-commerce story, industrial property REITs have been doing well. That includes Eastgroup Properties.

This is why the stock has been expensive at times. But after a 29% drop from its 52-week high, the stock has become a lot more appealing. The price-to-funds-from-operations ratio, based on that aforementioned guidance, is 23.7. Cheap? Not really. But reasonable. The five-year average P/CF ratio here is 24.3. We’re within spitting distance of its recent historical norm. I think this name is worth a look here.

This is why the stock has been expensive at times. But after a 29% drop from its 52-week high, the stock has become a lot more appealing. The price-to-funds-from-operations ratio, based on that aforementioned guidance, is 23.7. Cheap? Not really. But reasonable. The five-year average P/CF ratio here is 24.3. We’re within spitting distance of its recent historical norm. I think this name is worth a look here.

The third dividend increase we have to go over is the one that came courtesy of Illinois Tool Works Inc. (ITW).

Illinois Tool Works just increased their dividend by 7.4%. Okay. So this dividend increase did come in a bit lower than where the inflation rate is in the US. But as I alluded to earlier, if you manage your lifestyle properly, your personal inflation rate could be far lower than the national inflation rate – like mine is.

Moreover, a portfolio of high-quality dividend growth stocks will likely average out nicely, as this 7.4% dividend increase could be buoyed by double-digit dividend increases elsewhere. The thing about Illinois Tool Works, and the reason why I’m highlighting it here today, is their extraordinarily consistent dividend increases.

This marks the 59th consecutive year of dividend increases for the global industrial company. Just think about that. Nearly 60 straight years of ever-higher dividends. How difficult is it to consistently do anything for nearly 60 years in a row? Imagine how hard it is for a business to just keep churning out more revenue, higher profit, and a bigger dividend for almost six decades straight.

It’s incredible. This track record easily qualifies them for their Dividend Aristocrat status. The 10-year dividend growth rate is 13%, although more recent dividend increases have been in this high-single-digit range. The stock’s market-beating yield of 2.7% provides a good amount of current income while you wait for those reliable dividend raises.

It’s incredible. This track record easily qualifies them for their Dividend Aristocrat status. The 10-year dividend growth rate is 13%, although more recent dividend increases have been in this high-single-digit range. The stock’s market-beating yield of 2.7% provides a good amount of current income while you wait for those reliable dividend raises.

Since the payout ratio is 62.2%, which is slightly elevated but not troublesome, I suspect that Illinois Tool Works will continue to be an extraordinarily consistent dividend grower for years to come.

This Dividend Aristocrat isn’t super cheap, but I think it should at least be on one’s radar. Most basic valuation metrics indicate a stock that might be slightly undervalued. The P/E ratio of 23.2 is measurably below its own five-year average of 25.5.

On the other hand, the cash flow multiple is actually well above its own five-year average. You then have a P/S ratio that is basically right in line with its own recent historical average. This is a wonderful business, and I don’t see the valuation as overly demanding. It’s definitely a name to put on the radar, if not in the portfolio.

On the other hand, the cash flow multiple is actually well above its own five-year average. You then have a P/S ratio that is basically right in line with its own recent historical average. This is a wonderful business, and I don’t see the valuation as overly demanding. It’s definitely a name to put on the radar, if not in the portfolio.

The fourth dividend increase I want to cover today is the one that was announced by J&J Snack Foods Corp. (JJSF).

J&J Snack Foods just increased their dividend by 10.6%. Boom. Another inflation-beating dividend raise. Another raise that came about while shareholders did nothing other than hold their shares. It’s not just getting paid while you sleep; it’s getting paid more while you sleep. The pay raises don’t get any easier than this. Being a dividend growth investor is the best “job” I’ve ever had.

The food and beverage company has now increased its dividend for 18 consecutive years. Double-digit dividend increases are nothing new for this company – the 10-year dividend growth rate is 17.4%. Stellar. On the other hand, the stock’s yield of 1.9% means you do have to give up some yield in order to access that high growth rate. So it depends on which one you value more – income today or income tomorrow.

Really an individual call, which will likely largely come down to one’s age. The wildcard here is the fact that the company regularly reports volatile GAAP earnings. TTM GAAP EPS just barely covers the new, larger dividend. That’s something to be aware of.

Really an individual call, which will likely largely come down to one’s age. The wildcard here is the fact that the company regularly reports volatile GAAP earnings. TTM GAAP EPS just barely covers the new, larger dividend. That’s something to be aware of.

What’s very interesting about this name is the fact that the stock is still well below its pre-pandemic pricing. This was nearly a $190 stock in early 2020. It’s currently a $145 stock. In general, I’m more attracted to shares that haven’t participated in some of the nonsense that has occurred over the last two or so years – you know, the exuberance, excess liquidity, and temporary overearning.

That said, this company has been experiencing some tremendous constraints on margins. That’s been driven by significant inflationary pressures, including raw materials and packaging. And so the company just isn’t putting up some of the impressive numbers it was a few years ago.

The drop in pricing seems to be warranted here, and I’d say the stock’s valuation is only appealing if the company can quickly get the profitability back to where it’s historically been. Until then, it’s a name to keep an eye on.

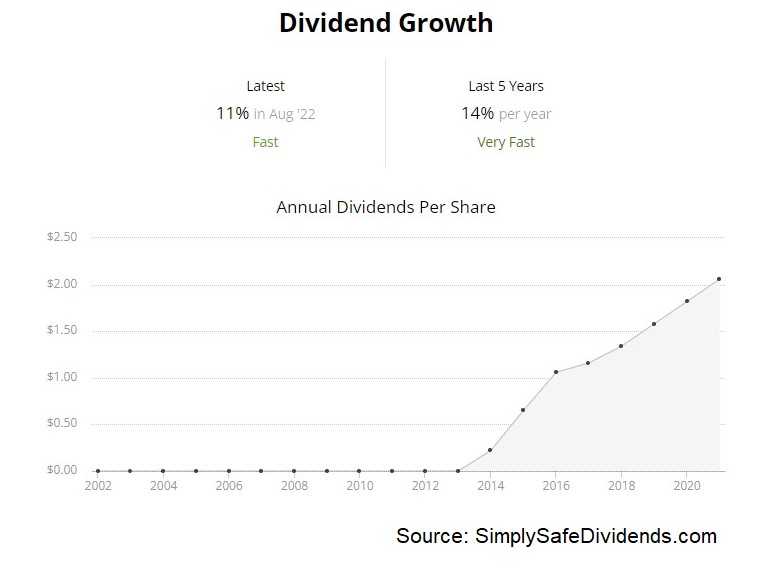

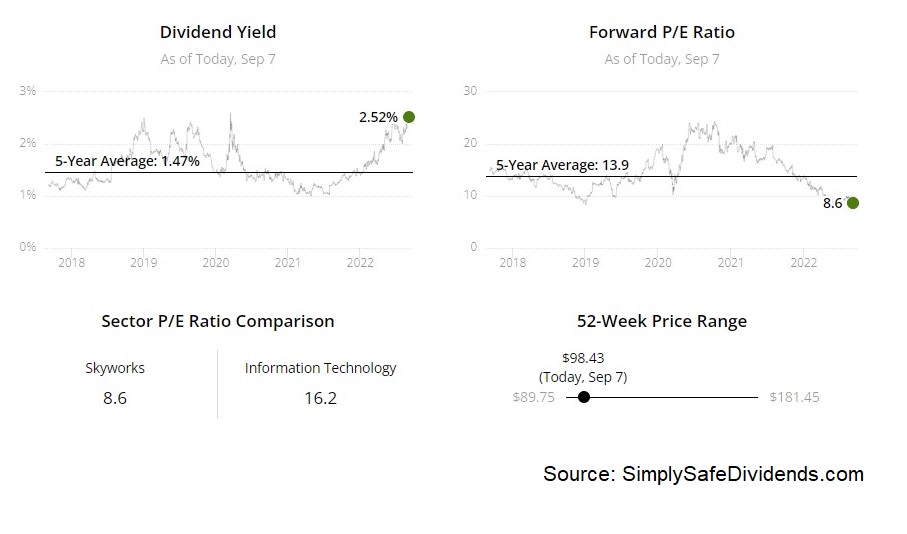

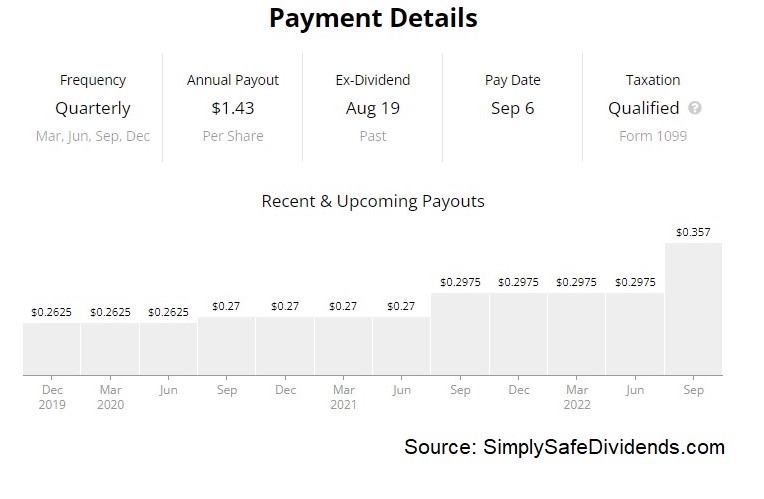

Next up, let’s have a quick conversation about the dividend increase that came from Skyworks Solutions Inc. (SWKS).

Skyworks Solutions just increased their dividend by 10.7%. Skyworks Solutions ought to be called “Income Solutions”, because they continue to solve the problem of living off of growing dividends for their shareholders. This is a company that excels at increasing their dividend, like clockwork, at a double-digit rate. I suspect we have a lot of happy shareholders here.

This is the eighth consecutive year of dividend increases for the semiconductor company. With a five-year dividend growth rate of 14.9%, along with a yield of 2.5%, Skyworks Solutions offers investors a chance to have their cake and eat it, too – you get a nice market-beating yield on one hand, and you get double-digit dividend growth on the other.

Tough to dislike any of that. And with a very low payout ratio of only 31.5%, this dividend almost certainly has plenty of double-digit increases yet ahead.

Tough to dislike any of that. And with a very low payout ratio of only 31.5%, this dividend almost certainly has plenty of double-digit increases yet ahead.

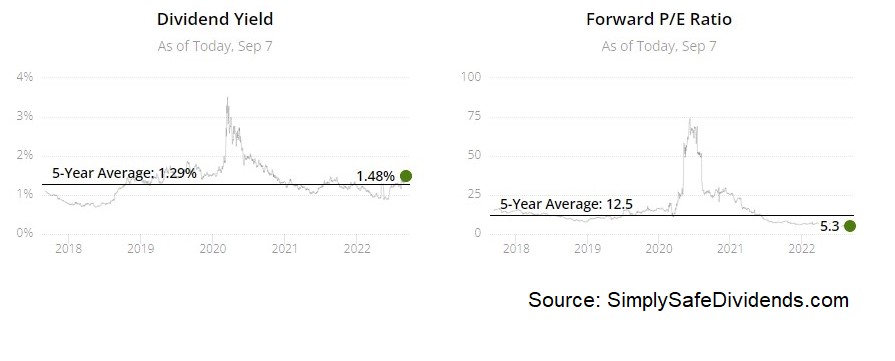

This stock looks cheeeeeap. We have a P/E ratio of 12.5. That’s low by any measure. It’s well below the broader market’s earnings multiple. It’s also substantially lower than the stock’s own five-year average P/E ratio of 20.1. If that’s not enough to convince you, the P/CF ratio of 10.2 isn’t even close to its own five-year average of 14.

Now, we do have some overhang here with Skyworks Solutions – they have an extreme amount of customer concentration with their Apple Inc. (AAPL) relationship (59% of FY 2021 revenue). If there were any one customer you’d want to rely on, you can’t beat Apple.

Now, we do have some overhang here with Skyworks Solutions – they have an extreme amount of customer concentration with their Apple Inc. (AAPL) relationship (59% of FY 2021 revenue). If there were any one customer you’d want to rely on, you can’t beat Apple.

It’s not like you have to worry about Apple going out of business. Instead, you have to worry about them cutting you out. So that’s the risk here with Skyworks Solutions. If you’re okay with that, the valuation and dividend metrics both offer a lot to like.

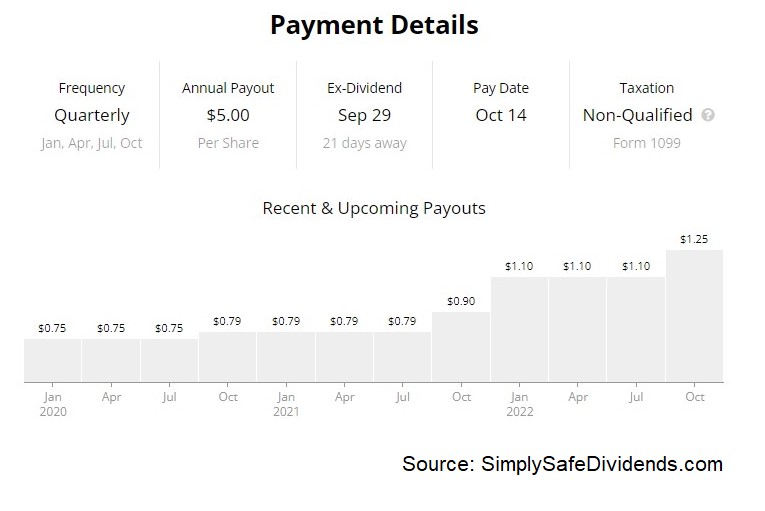

Last but not least, I want to bring to your attention the dividend increase that was announced by Westlake Corp. (WLK). Westlake just increased their dividend by 20%. Boy, I guess I saved the best for last. A 20% dividend increase. How can you not love dividend growth investing?

That’s 20% more income for Westlake shareholders, and all they had to do was hold shares. It really is that easy. This isn’t just passive income. It’s passive income that’s growing at a tremendous rate. Hard to overstate how amazing this is.

This marks the 18th consecutive year of dividend increases for the international chemical company. If this 20% dividend increase surprises you, you’re not paying attention. Westlake’s 10-year dividend growth rate is 23.2%, so this is basically status quo behavior for them.

This marks the 18th consecutive year of dividend increases for the international chemical company. If this 20% dividend increase surprises you, you’re not paying attention. Westlake’s 10-year dividend growth rate is 23.2%, so this is basically status quo behavior for them.

The issue here, if there is one, might be the yield: The stock’s yield is only 1.5%. However, it’s worth pointing out that this is actually 20 basis points higher than its own five-year average. This is a stock that typically has a low yield. Investors have been willing to accept that low yield in favor of the very high dividend growth rate. The payout ratio, at under 10%, is super, super low. But recent results have been abnormally strong.

We have a stock that appears to be extremely undervalued, but is it really? It all depends on how sustainable recent results are. Westlake’s financials can look amazing or only so-so, depending on the year and overall economic conditions. To say the business is cyclical is understating it.

We have a stock that appears to be extremely undervalued, but is it really? It all depends on how sustainable recent results are. Westlake’s financials can look amazing or only so-so, depending on the year and overall economic conditions. To say the business is cyclical is understating it.

To give you some perspective on this, the $15.58 in GAAP EPS the company reported for FY 2021 was six times higher than the $2.56 in GAAP EPS the company reported for FY 2020. The pandemic obviously skews things, so it’s hard to draw firm conclusions, but I’d also say that the stock is pricing in plenty of abnormality.

The P/E ratio is only 4.3. So the market is clearly expecting a serious drop in earnings. This is a name that you have to be careful with, just because it’s so hard to judge the road ahead, but it’s definitely interesting right now.

I’ll see you next time.

— Jason Fieber

The old way of investing in tech giants is over. A NEW strategy unlocks 146X more income on the SAME underlying stocks (like Meta, Apple, and Amazon) -- WITHOUT options trading. Click here to uncover the NEW MAG-7 alternative.

Source: Dividends & Income