If you did any driving over the holiday weekend, you may have noticed that prices at the pump are much more manageable than they were just a few months ago. In fact, they recently hit their lowest level since mid-February.

That’s great for motorists, but has admittedly created plenty of pain for investors who thought the windfall profits in the oil patch were sustainable. Consider that the popular Energy Select Sector SPDR Fund (XLE) made up of blue chip energy stocks is down almost 15% from its June high, while the S&P 500 on average has managed to post a small gain in the same period.

You might think energy stocks are old news as a result. However, at Contrarian Outlook we never take things at face value. We look for a way to provide low-risk income that will last regardless of short-term trends in a given sector – and regardless of the headlines.

While the general outlook for energy is indeed a bit rocky, there are still attractive dividend payers in the sector. In fact, one of my favorite dividend stocks right now is an energy play that’s up about 13% from its June lows – and pays a generous and very sustainable 7.2% dividend right now.

That stock is Enterprise Products Partners L.P. (EPD). Keep reading and I’ll explain why this is a great stock to watch this Fall regardless of gasoline or oil prices – and why it’s just one of the low-risk, 7%+ dividend stocks that should be on your buy list right now.

EPD is a Midstream Stock with Staying Power

Enterprise is a “midstream” energy stock, meaning it stands between companies that take oil or gas out of the ground and the wholesalers and refiners at the end of the supply chain. It’s not a particularly high margin business compared with some of the other subsectors in the industry, but it is an incredibly reliable one. EPD is a glorified toll-taker as it moves commodities around to and from customers.

This general trait is a big vote in favor of Enterprise Products, as the midstream operations smooth out volatility. But the specific numbers showing stability and growth are what really seals the deal.

Consider that in August EPD reported distributable cash flow that was up 30% to a record $2.0 billion in the second quarter. Meanwhile, its latest distribution of 47.5 cents per share adds up to just over $1.0 billion in total payouts to shareholders. In other words, it can cover payouts twice over at this run rate.

Looking forward, Enterprise should have the growth and stability to ensure that figure isn’t an anomaly either. EPD boasts roughly $5.5 billion worth of projects in the pipeline – pardon the pun – through 2025. Natural gas investments have been a heavy focus, as this cleaner-burning fossil fuel is increasingly being seen as a bridge between the use of dirtier oil and coal and long-term green energy sources like wind and solar. Additional capacity will ensure Enterprise is playing its role in a more sustainable energy sector, and keeping its cash flow strong at the same time.

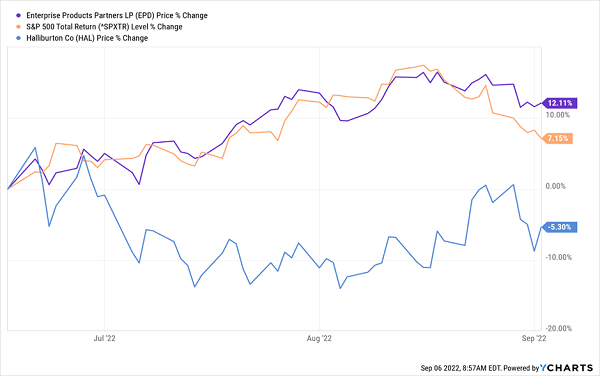

What’s more, shares are up about 12% from their June lows even as some other energy stocks have stumbled. In fact, that outperforms the broader S&P 500 in the same period to prove it’s not just a strong stock in a weak sector but actually one of the best performers on Wall Street of any flavor. That’s even more impressive considering sensitive energy stocks like oilfield service giant Haliburton (HAL) are still in the red compared with where they were two months ago.

What’s more, shares are up about 12% from their June lows even as some other energy stocks have stumbled. In fact, that outperforms the broader S&P 500 in the same period to prove it’s not just a strong stock in a weak sector but actually one of the best performers on Wall Street of any flavor. That’s even more impressive considering sensitive energy stocks like oilfield service giant Haliburton (HAL) are still in the red compared with where they were two months ago.

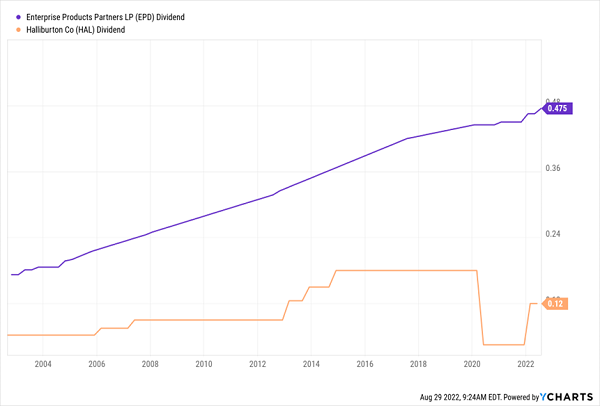

And when you compare the volatile nature of dividends elsewhere in the energy sector, there’s simply no question that EPD is in a class by itself. Just look at this 20-year chart of distributions comparing Halliburton and Enterprise Product Partners. HAL sees a few ups, a significant down, and periods where its payouts flatline for years at a time. On the other hand, EPD has slowly increased its payout like clockwork – proving its commitment to long-term dividend growth as well as reliability.

And when you compare the volatile nature of dividends elsewhere in the energy sector, there’s simply no question that EPD is in a class by itself. Just look at this 20-year chart of distributions comparing Halliburton and Enterprise Product Partners. HAL sees a few ups, a significant down, and periods where its payouts flatline for years at a time. On the other hand, EPD has slowly increased its payout like clockwork – proving its commitment to long-term dividend growth as well as reliability.

— Jeff Reeves

Placing a Premium on Reliability [sponsor]

Hopefully what EPD has to offer is clear to you. But more importantly, I hope that the investing thesis behind this stock is equally clear.

Successful long-term investing isn’t just about crunching the numbers or watching the latest headlines… it’s about discipline, and a desire to succeed in the long term regardless of day-to-day volatility.

That’s why we place a premium on reliability here at Contrarian Outlook. Other websites can serve up clickbait based on the latest consumer tech product or short-term swings in the price of a given commodity. Instead, we focus on strategies that work over the long haul.

That ultimately will wind up saving our readers from making costly mistakes, and provide consistent income they can rely on in retirement. It also has the added benefit of avoiding the stressful glued-to-your-smartphone mindset that keeps day traders up at night.

On balance, I’m optimistic about the stock market as we look to close out the year. But that doesn’t mean I’m going to start making risky bets or taking chances. Instead, at Contrarian Outlook we’re laser-focused on tactical, “just in case” stocks right now.

These investments are riding a short-term uptrend… but have proven resilience, just in case there is some backsliding for stocks in the months ahead.

Investments like these are rare, but they are out there if you know where to look for them. In fact, our overlooked basket of recession-resistant stocks haven’t just been surviving—they’ve been setting up to thrive.

How can we be so sure? Well, because our team of analysts have only gotten more selective lately even as the clouds have parted on Wall Street this summer. We only recommend companies with a proven track of increasing their dividend payments, reliable share prices, and upside potential that aims to double your money roughly every five years.

Sound too good to be true? Well, it isn’t. Click here for an exclusive, risk-free offer to discover our 7 Recession-Resistant Dividend Stocks With 100% Upside!

Source: Contrarian Outlook