I want to tell you about a high-quality stock that pays big, growing, reliable dividends. These growing dividends are funded by growing profit, because this business is a leading provider of high-value technology manufacturing equipment.

This world is drowning in semiconductors. And yet we’re hungry for more. From autos to smartphones to refrigerators, devices left and right are becoming more smart, more connected, and more reliant on semiconductors.

Well, this company provides specialized manufacturing equipment that allows for semiconductors to get made. And that’s why it continues to rack up higher revenue and more profit, and pay out a larger dividend. I’ve personally invested in stocks just like this one on my way to going from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

If you’re interested, you can download a free copy of my Early Retirement Blueprint.

Getting back to the stock I’ll tell you about today though, perhaps best of all, it looks undervalued right now.

Price is what you pay. But value is what you get.

Why’s that important? Because buying a dividend growth stock when it’s undervalued should provide a higher yield, greater long-term total return potential, and reduced risk. With this in mind, I want to tell you about an opportunity I recently came across with a stock that appears to be trading at a significant discount today…

Lam Research (LRCX)

Lam Research (LRCX)

Lam Research (LRCX) – is a major manufacturer of equipment used in the fabrication of semiconductors.

Founded in 1980, Lam Research is now a $62 billion (by market cap) capital equipment giant that employs 17,000 people. Take a good look around you. What do you see? Semiconductors… everywhere.

Well, you might not literally see these semiconductors. But that doesn’t make them any less ubiquitous. Semiconductors are already in countless devices across pretty much every area of our lives. And this pervasiveness is only increasing.

Devices like smartphones and computers are obviously hungry for semiconductors.

However, semiconductor application stretches far beyond the obvious – think communications, healthcare, military systems, transportation, energy, etc. For example, a new car has, on average, more than 1,000 chips in it. With semiconductors being a cornerstone of our modern-day society, the equipment that allows these semiconductors to come into existence are obviously critical.

That’s where Lam Research comes in. The company is a leader in providing machines focused on etch, deposition, and cleaning, which are key steps in the semiconductor manufacturing process. Without the capital equipment necessary for fabrication, semiconductors don’t get made.

Well, Lam Research already has an installed base of 75,000 units. And it’s only growing.

This is what perfectly positions Lam Research to ride the semiconductor wave to higher revenue and profit well into the future, which should translate into a dividend that continues to grow at a high rate.

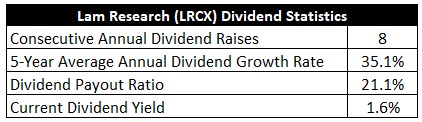

Dividend Growth, Growth Rate, Payout Ratio and Yield

Already, Lam Research has increased its dividend for 8 consecutive years. The company is somewhat new to the dividend growth game. But Lam Research is getting the hang of it very quickly.

The five-year dividend growth rate is a jaw-dropping 35.1%. That’s huge.

By the way, a double-digit dividend growth rate continues – Lam Research increased its dividend by 15% only days ago. Now, one would almost require that kind of high growth rate when you see that the stock yields only 1.6%.

However, this is more of a long-term compounder than an income play.

However, this is more of a long-term compounder than an income play.

That said, this yield is 20 basis points higher than its own five-year average.

And with an extremely low payout ratio of 21.1%, I suspect that shareholders can look forward to plenty more double-digit dividend increases in the years ahead.

For younger dividend growth investors who prefer growth and compounding over current income, these dividend metrics are appealing.

Revenue and Earnings Growth

Looking at business growth, Lam Research moved its revenue from $3.6 billion in FY 2013 to $17.2 billion in FY 2022. That’s a compound annual growth rate of 19%. Truly extraordinary top-line growth here.

Meanwhile, earnings per share grew from $0.66 to $32.75 over this period, which is a CAGR of 54.3%. This is almost unreal EPS growth.

However, it’s made to look more exceptional than it really is by virtue of FY 2013’s unusually low EPS. If we look at more recent results, Lam Research compounded its EPS at an annual rate of 25.6% over the last five years.

Still fantastic. Just not quite as amazing as the prior number. Lam Research has been able to meaningfully expand net margin over the last decade, which explains much of the excess bottom-line growth. As impressive as the margin expansion story has been, it’s almost impossible for them to repeat this.

Looking forward, CFRA is forecasting that Lam Research will compound its EPS at an annual rate of 10% over the next three years. This would be a material drop in EPS growth compared to what transpired over the last decade. But I think it makes sense to take a cautious stance right now. CFRA highlights near-term challenges from high freight costs and manufacturing difficulties (which both circle back around to broader supply chain issues).

In addition, as I just pointed out, it’s hard to imagine net margin expanding much more than it already has. There’s also Lam Research’s exposure to China. For the company’s most recent quarter, the top three geographic areas for distribution of revenue were: China, 31%; Korea, 24%; and Taiwan, 19%.

China’s well-documented troubles, as well as tensions between China and Taiwan, add a cloud of uncertainty around Lam Research.

Furthermore, this geographic distribution of revenue disproportionately exposes the company to the strong dollar. CFRA’s forecast looks sensible to me, as Lam Research’s most recent quarter (Q4 FY 2022) showed 9.5% YOY EPS growth.

All this said, managing to produce double-digit EPS growth during such an unsettled time would further showcase how great and important this business is. And that would allow the dividend to easily grow at a double-digit rate, especially with the payout ratio being so low.

Putting it all together, I see Lam Research continuing to increase its dividend at a high rate for the foreseeable future.

Financial Position

Moving over to the balance sheet, the company has a strong financial position.

The long-term debt/equity ratio is 0.8, while the interest coverage ratio is over 29. Furthermore, total cash of $3.9 billion is nearly enough to totally offset all long-term debt. Profitability is terrific.

Over the last five years, the firm has averaged annual net margin of 23.7% and annual return on equity of 50.5%. I want to quickly add some perspective on the net margin expansion story.

Lam Research was printing net margin in the low-teen area a decade ago, whereas net margin came in at nearly 30% last fiscal year. This is an extremely high-quality business with excellent fundamentals.

And with a large installed base that adds “stickiness”, IP, R&D, technological know-how, global economies of scale, and high barriers to entry, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry. The company’s geographic mix adds geopolitical and currency risks.

The very business model is a risk, as technology is rapidly changing. Lam Research must constantly innovate and stay ahead of the curve in order to remain competitive. Current supply chain challenges are adding execution and near-term earnings risks.

Stock Price Valuation

Although semiconductor demand is mostly secular over the long run, there is short-term cyclical risk in the industry. There are formidable risks present, but I think the quality of the business is even more formidable. And with the stock down a stunning 40% from its 52-week high, the valuation makes this name look more compelling to me than it has in years.

The stock’s P/E ratio is 13.5. That’s well below the broader market’s P/E ratio. It’s also way off of the stock’s own five-year average P/E ratio of 18.8. For a company growing at such a high rate, this is an absurdly low earnings multiple. We can also see that the P/S ratio of 3.6 is quite a bit lower than its own five-year average of 4.4. And the yield, as noted earlier, is higher than its own recent historical average.

I valued shares using a two-stage dividend discount model analysis. I factored in a 10% discount rate, a 14% dividend growth rate over the next five years, and a long-term dividend growth rate of 8%. So I’m assuming that the next few years will still be pretty heady in terms of dividend growth, but I also see growth leveling off thereafter.

I think the near term looks so bright because of the low payout ratio (a ratio which can be expanded) and near-term EPS growth expectation.

The most recent dividend increase gives me further confidence. It would be silly to expect high-double-digit dividend growth to persist indefinitely, but my long-term dividend growth expectation here is as high as I’ll go.

In my view, a business of this kind of quality deserves the designation. The DDM analysis gives me a fair value of $483.91. The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Morningstar rates LRCX as a 4-star stock, with a fair value estimate of $720.00.

CFRA rates LRCX as a 4-star “BUY”, with a 12-month target price of $594.00.

We have a range, and I came out on the low end, but we all see a stock that looks cheap. Averaging the three numbers out gives us a final valuation of $599.30, which would indicate the stock is possibly 35% undervalued.

Lam Research (LRCX) is a very high-quality business benefiting from the crucial nature of their products in an industry that is only seeing increasing global demand over the long run. With a super low payout ratio, an outstandingly high dividend growth rate, almost 10 straight years of dividend increases, and the potential that shares are 35% undervalued, this is a compelling idea for long-term dividend growth investors who prefer growth over income.

Lam Research (LRCX) is a very high-quality business benefiting from the crucial nature of their products in an industry that is only seeing increasing global demand over the long run. With a super low payout ratio, an outstandingly high dividend growth rate, almost 10 straight years of dividend increases, and the potential that shares are 35% undervalued, this is a compelling idea for long-term dividend growth investors who prefer growth over income.

I’ll see you next time.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is LRCX’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 66. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, LRCX’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

The old way of investing in tech giants is over. A NEW strategy unlocks 146X more income on the SAME underlying stocks (like Meta, Apple, and Amazon) -- WITHOUT options trading. Click here to uncover the NEW MAG-7 alternative.

Source: Dividends & Income