The market has been on a tear since mid-July. As of August 24 the S&P 500 is up by 13% since bottoming out.

Good stuff, right? Not really.

If you’re a young investor who is still actively accumulating stocks, this is no bueno. It means you have to pay more money for the shares you want to buy. And since price and yield are inversely correlated, all else equal, it also means lower yields.

You pay more to get less. Bummer.

But fear not. I still see some great long-term investment opportunities out there for dividend growth investors, even after the bounce. In fact, I recently initiated a new position for my FIRE Fund. And I’m very excited to be a shareholder.

Today, I want to tell you about a Dividend Aristocrat I recently bought for my FIRE Fund.

Ready? Let’s dig in.

Which Dividend Aristocrat just got added to the FIRE Fund? It’s Caterpillar Inc. (CAT).

![]() Caterpillar is a multinational heavy machinery company with a market cap of $105 billion.

Caterpillar is a multinational heavy machinery company with a market cap of $105 billion.

This is the world’s leading manufacturer of construction and mining equipment. Caterpillar helps to keep the world turning, figuratively speaking. We can’t build out our modern-day society without the construction equipment that Caterpillar manufactures. You know which machines I’m talking about. Those big yellow ones with “CAT” blazed on them.

Everything from skyscrapers high up in the air to mines deep down in the earth require heavy machinery.

The company can trace its roots back to the late 1800s. We’re now in 2022. How and why has it been able to thrive for more than 100 years? Well, because our world cannot and would not exist as it is without the more than 300 machines that Caterpillar makes. We’re talking about articulated trucks, asphalt pavers, excavators, hydraulic mining shovels, etc.

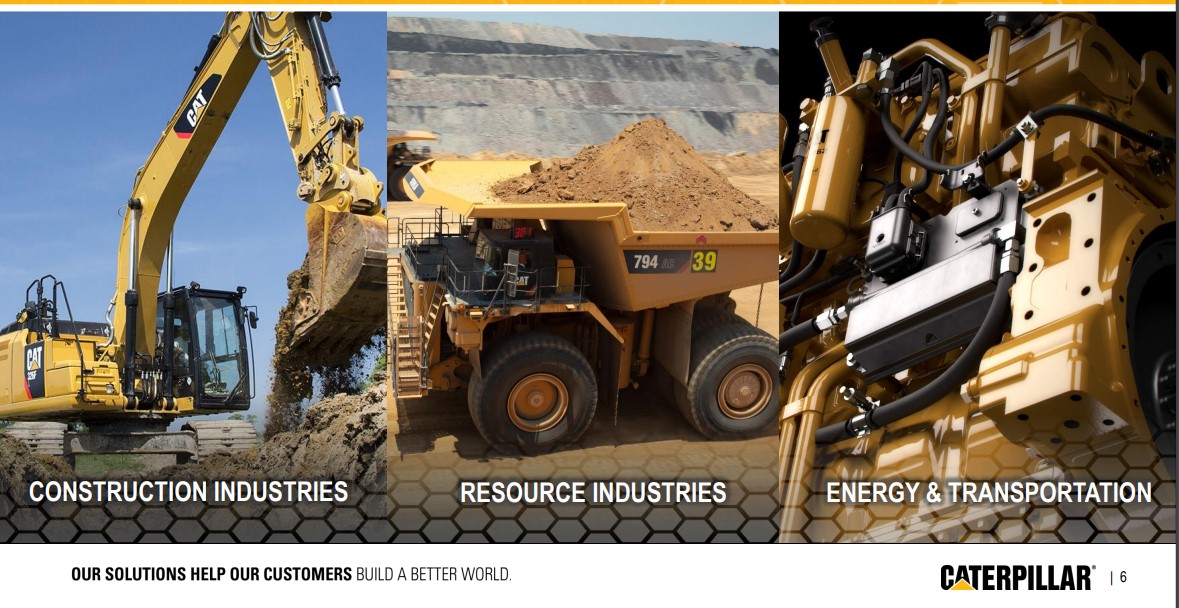

The company’s sales are broken down across three major areas.

Construction Industries comprises 40% of annual sales; Energy & Transportation 37%; and Resource Industries, 18%. The remaining 5% of annual sales is related to the company’s financing arm. As you can see, Caterpillar is diversified across industries. And it just so happens that all of these industries are healthy right now.

Construction Industries comprises 40% of annual sales; Energy & Transportation 37%; and Resource Industries, 18%. The remaining 5% of annual sales is related to the company’s financing arm. As you can see, Caterpillar is diversified across industries. And it just so happens that all of these industries are healthy right now.

The point of diversification is that, when one area of your portfolio is not doing well, you should be able to count on another area to do well and prop up the overall results. Well, all three of Caterpillar’s major areas are firing on all cylinders right now. Construction is being lifted by the $1.2 trillion Infrastructure Investment and Jobs Act, which was signed into law in November 2021.

Energy & Transportation is going gangbusters on the back of higher energy prices. And we continue to need more mining of resources ranging from lithium to copper in order for the EV story to play out, which bodes well for Caterpillar’s related machinery. Furthermore, Caterpillar’s backlog is $23.1 billion as of the end of FY 2021. That’s up from $14.2 billion as of the end of FY 2020. All three areas of Caterpillar saw increases in their respective portions of the backlog.

That’s translating to a very healthy business for Caterpillar as a whole.

The company’s most recently reported quarter, Q2 FY 2022, showed 10.5% YOY revenue growth and 22.3% YOY growth in adjusted EPS. This, during a time in which other companies are showing YOY declines in top-line and bottom-line growth in the face of tough comps and a contracting economy.

But this is nothing new for Caterpillar.

Its results are a bit lumpy, and the business is obviously quite cyclical. So its growth, or lack thereof, can depend on what time period you’re looking at. But over the long term, we can clearly see a nice upward trend across the business. Between FY 2016, which represented a bottoming out after a downturn in many of its end markets, and FY 2021, revenue grew at a CAGR of 5.8%. EPS swung from a minor loss to $11.83 in the green over that stretch.

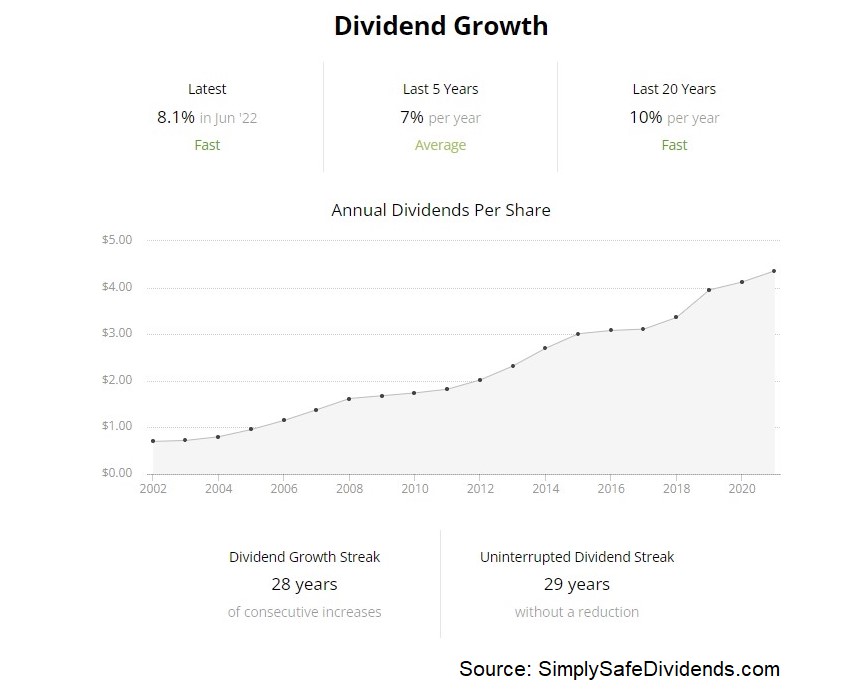

What’s not lumpy? Caterpillar’s dividend.

This might be a cyclical business, but you wouldn’t know it by looking at the dividend. Caterpillar doesn’t just pay a reliable dividend; Caterpillar pays a dividend that reliably grows. The company has increased its dividend for 29 consecutive years.

That easily qualifies them for their status as a vaunted Dividend Aristocrat.

That easily qualifies them for their status as a vaunted Dividend Aristocrat.

It’s one thing for, say, a consumer products company to become a Dividend Aristocrat. But it’s quite another thing for a cyclical machinery company to get there, which just goes to show how prudent management has been. Even though Caterpillar has a cyclical business model, and even though the stock price can sometimes look like an EKG printout, the dividend has reliably grown straight through the cycles.

Caterpillar’s dividend metrics look great.

The 10-year dividend growth rate is 9%, which is very solid and easily beats inflation over that period. That kind of dividend growth keeps your purchasing power moving ahead of inflation. And you’re pairing that dividend growth with a starting yield of 2.5%. When you can get a yield that beats the market and a dividend growth rate that beats inflation, you’re doing pretty good. Also, that 2.5% yield is 10 basis points higher than its own five-year average. With a payout ratio of 42.1%, the dividend is secure today and also cushioned against potential future downturns.

As a dividend growth investor, I like what I see with the dividend. And that’s a big part of why I initiated a position in Caterpillar.

I initiated a position in Caterpillar for the FIRE Fund on August 2nd, 2022 for $187.62 per share, and I alerted my Patrons over at Patreon about that move right after I made it. I’ll be actively building up a position in Caterpillar over the coming weeks, and I may have even bought more shares by the time you read this. I’m looking forward to being a Caterpillar shareholder for decades to come.

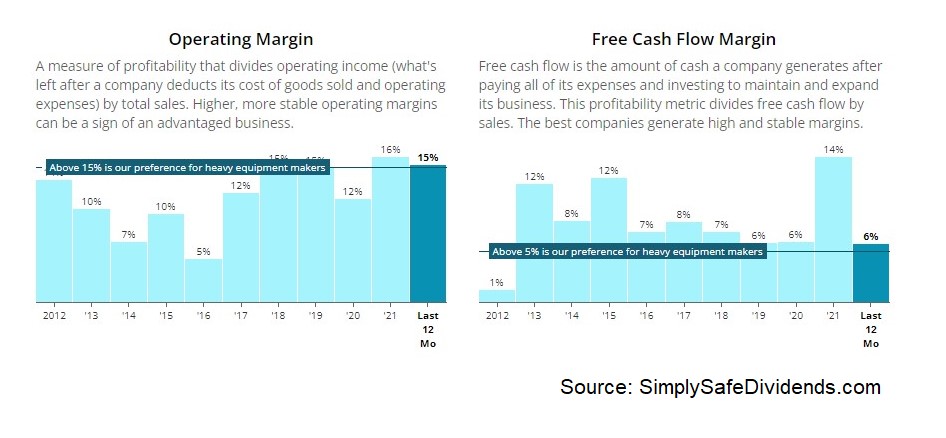

This is a business that continues to get better.

Caterpillar has eliminated over $2B in structural costs since 2014, which has helped with profitability and free cash flow. At the start of the last decade, Caterpillar was routinely putting up single-digit net margin. The company is now regularly printing double-digit net margin, with net margin coming in at 12.7% last fiscal year.

But wait. There’s more.

Free cash flow for the core business doubled YOY for FY 2021. They’re expanding higher-margin services offerings, while also bringing electrification and automation to their products. Caterpillar knows the future for machinery is in those key technologies. They’re ahead of the curve. And while the balance sheet might look heavy with debt, that’s largely because Caterpillar finances the purchases of its machinery. An interest coverage ratio of nearly 18 indicates a healthy financial position.

And all of this is available at a reasonable valuation.

And all of this is available at a reasonable valuation.

Caterpillar’s stock is trading hands for a P/E ratio of 15.4. That’s well below the broader market’s earnings multiple. Now, Caterpillar’s five-year average P/E ratio is 55. But that’s not a straight comparison, as the company’s financial results can be so volatile. On the other hand, the P/S ratio of 1.9 is exactly in line with its own five-year average. Putting it all together, I see Caterpillar’s stock as reasonably valued, although I don’t think it’s extremely cheap. But paying a fair price for a Dividend Aristocrat is rarely a bad call.

Is this Dividend Aristocrat right for your portfolio?

Well, that’s really your decision. But I think Caterpillar offers a lot to like right now. It’s a world leader that’s set to benefit from a massive spending bill. All three of its major areas are doing very, very well. The stock offers a market-beating yield, inflation-beating dividend growth, a moderate payout ratio, nearly 30 consecutive years of dividend increases, and a reasonable valuation. I’m happily buying this Dividend Aristocrat. And you may want to consider doing the same.

Well, that’s really your decision. But I think Caterpillar offers a lot to like right now. It’s a world leader that’s set to benefit from a massive spending bill. All three of its major areas are doing very, very well. The stock offers a market-beating yield, inflation-beating dividend growth, a moderate payout ratio, nearly 30 consecutive years of dividend increases, and a reasonable valuation. I’m happily buying this Dividend Aristocrat. And you may want to consider doing the same.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income