I want to tell you about a high-quality stock that pays big, growing, reliable dividends.

These growing dividends are funded by growing profit, because this business is a leading chemicals company for the production of countless everyday products.

Consumption of everyday products is such an integrated part of everyday life, people are often referred to as consumers.

Think about that.

You’re more a consumer than a person.

You’re more a consumer than a person.

Well, this is not going to change.

If anything, consumption is on the rise.

And this company makes sure that a variety of everyday products are able to actually be produced.

This puts them in a position to grow their revenue, profit, and dividend for as long as consumption is a thing.

I’ve personally invested in stocks just like this one on my way to going from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

Getting back to the stock I’ll tell you about today though, perhaps best of all, it looks undervalued right now. Price is what you pay. But value is what you get.

Why’s that important? Because buying a dividend growth stock when it’s undervalued should provide a higher yield, greater long-term total return potential, and reduced risk. With this in mind, I want to tell you about an opportunity I recently came across with a stock that appears to be trading at a significant discount today…

Eastman Chemical Company (EMN)

Eastman Chemical Company (EMN) – is a global specialty chemical company that manufactures and markets a wide range of advanced materials, chemicals, and fibers which are used in various consumer and industrial products.

Founded in 1920, Eastman Chemical is now a $12 billion (by market cap) chemicals giant that employs 14,000 people.

The company reports results through four segments: Additives & Functional Products, 35% of FY 2021 sales; Advanced Materials, 29%; Chemical Intermediates, 27%; and Fibers, 9%.

The company generates 42% of its sales from inside the US, while the remaining 58% comes from outside the US.

Eastman Chemical has exposure to nearly every industry you could think of, spread out across most major markets in the world.

Everyday end products that are used in everyday life often require advanced materials and chemicals in order to be manufactured.

Packaging, electronics, autos, and cosmetics are just a few examples.

Eastman Chemical is a part of the backbone of the global manufacturing complex.

This positioning has led to steady growth across the business.

And unless the world suddenly stops consuming manufactured products, Eastman Chemical stands to grow its revenue, profit, and dividend for many years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

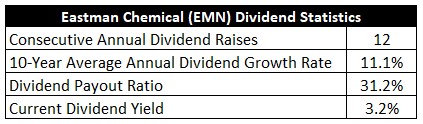

To date, the company has increased its dividend for 12 consecutive years.

The 10-year dividend growth rate is 11.1%, but I will caution that the size of dividend increases can be somewhat lumpy from year to year.

Plus, the stock offers a market-beating 3.2% yield to start off with.

Plus, the stock offers a market-beating 3.2% yield to start off with.

That yield, by the way, is 40 basis points higher than its own five-year average.

And with a payout ratio of 31.2%, based on midpoint adjusted EPS guidance for this fiscal year, this is a healthy dividend poised for much more growth.

I really like dividend growth stocks in what I refer to as the “sweet spot” – that’s a yield of between 2.5% and 3.5%, paired with a high-single-digit (or higher) dividend growth rate.

This stock offers both a yield and a dividend growth rate that are on the higher end of what I tend to look for.

Very, very sweet.

Revenue and Earnings Growth

Looking at business growth, Eastman Chemical increased its revenue from $8.1 billion in FY 2012 to $10.5 billion in FY 2021.

That’s a compound annual growth rate of 2.9%.

Not amazing. But certainly not bad, either.

Meanwhile, earnings per share grew from $2.93 to $6.25 over this period, which is a CAGR of 8.8%.

Modest buybacks have helped to move the needle in terms of excess bottom-line growth, and net margin has improved relative to this starting point.

Pretty good bottom-line growth, but I’ll caution, again, that the growth can come in fits and spurts.

The business is cyclical, and the results are lumpy from year to year, but the long-term picture appears to be very good.

Looking forward, CFRA believes that Eastman Chemical will compound its EPS at an annual rate of 10% over the next three years.

This would mark some acceleration in growth relative to the last decade.

The optimism doesn’t seem unfounded to me.

Rightfully so, CFRA highlights Eastman Chemical’s diversified portfolio as a key strength.

In addition, they note that pricing power and cost savings will be two levers for the business to pull.

CFRA states: “…we see more upside in 2022 from strong growth in Eastman Chemical’s specialty products and pricing actions.”

CFRA then adds: “We also think Eastman Chemical’s focus to remove $200 million of structural costs by 2022 will benefit the firm’s earnings profile in the medium-term.”

I would also point to Eastman Chemical’s own FY 2022 guidance for further evidence of a reasonable forecast.

The company is guiding for $9.75 in adjusted EPS at the midpoint for this fiscal year, which would represent 10.2% YOY growth compared to the $8.85 in adjusted EPS the company reported for FY 2021.

This kind of EPS growth would support similar dividend growth over the foreseeable future.

Pairing high-single-digit dividend growth with a 3.2% yield is quite enticing, in my view.

Financial Position

Moving over to the balance sheet, the company does have a good financial position.

The long-term debt/equity ratio is 0.8, while the interest coverage ratio is 9.

Eastman Chemical’s balance sheet isn’t spectacular, but there are no financial issues here.

Profitability is solid.

Over the last five years, the firm has averaged annual net margin of 9.2% and annual return on equity of 16.1%.

Eastman Chemical doesn’t necessarily “wow” me in any one area, but it’s just a well-put-together business that looks really good on a sum-of-the-parts basis.

And with economies of scale, IP, R&D, and technological know-how, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Raw material and other input costs can be volatile, which causes fluctuations in cash flow.

The cyclical nature of manufacturing exposes the company to slowdowns and recessions.

There’s technological risk, as manufacturing technologies could change in a way that would reduce the need for some of the company’s offerings.

Stock Price Valuation

Overall, I see the risks as very tolerable, especially when viewed against the quality and growth profile of the business.

And with the stock down 25% from its 52-week high, the valuation makes it especially compelling at this point in time.

The stock is trading hands for a P/E ratio of 10.7.

That’s about half that of the broader market’s earnings multiple.

It’s also materially lower than the stock’s own five-year average P/E ratio of 17.3.

We can also see that the current P/S ratio of 1.2 is slightly lower than its own five-year average of 1.3.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

That dividend growth rate is not as high as I’ll go, and I think it builds in a margin of safety.

This mark is lower than the company’s demonstrated dividend growth rate and EPS growth rate over the last decade, and it’s also lower than the near-term expectation for EPS growth.

Also, the payout ratio is still quite moderate.

Because of the cyclical nature of the business, and the lack of extreme quality, I find it prudent to be conservative here.

That said, it wouldn’t surprise me at all to see Eastman Chemical exceed this 7% dividend growth rate over the foreseeable future.

But I would rather err on the side of caution.

The DDM analysis gives me a fair value of $108.43.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Morningstar rates Eastman Chemical as a 5-star stock, with a fair value estimate of $140.00.

CFRA rates Eastman Chemical as a 4-star “BUY”, with a 12-month target price of $125.00.

I came out low here, but we’re all in general agreement that the pricing is favorable. Averaging the three numbers out gives us a final valuation of $124.48, which would indicate the stock is possibly 27% undervalued.

Bottom line: Eastman Chemical Company (EMN) is an under-the-radar business that is being run in a very competent manner across its operations. Unless global consumption of everyday products suddenly ceases to exist, this company has a bright future. With a market-beating yield, double-digit long-term dividend growth, a moderate payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 27% undervalued, long-term dividend growth investors ought to seriously consider this name while it appears to be on sale.

Bottom line: Eastman Chemical Company (EMN) is an under-the-radar business that is being run in a very competent manner across its operations. Unless global consumption of everyday products suddenly ceases to exist, this company has a bright future. With a market-beating yield, double-digit long-term dividend growth, a moderate payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 27% undervalued, long-term dividend growth investors ought to seriously consider this name while it appears to be on sale.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from DTA: How safe is EMN’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 85. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, EMN’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends and Income