I’ve been successfully investing for more than a decade now. One of the biggest things I’ve learned?

You have to be willing to go against the crowd.

This is true in investing… and life, in general, quite frankly. When the herd is going one way, you’ve gotta muster up the courage and discipline to go the opposite way. Because when everyone is chasing after certain stocks and bidding them way up, you quite simply get less for your money.

Conversely, when everyone is running away, that’s when you get more value for money and more safe, growing dividend income on the same investment capital.

Do you like to get more or less for your money? My point exactly.

Well, the good news is that some stocks have recently been pummeled and have become way cheaper. I’m even talking about some high-quality dividend growth stocks. These are stocks that pay reliable, rising dividends. And how do reliable, rising dividends get funded?

Through reliable, rising profits. Great businesses on sale after the crowd ran away? Sounds like long-term investment opportunities to me.

Today, I want to tell you about five dividend growth stocks that are down more than 20% from their recent highs.

Ready? Let’s dig in.

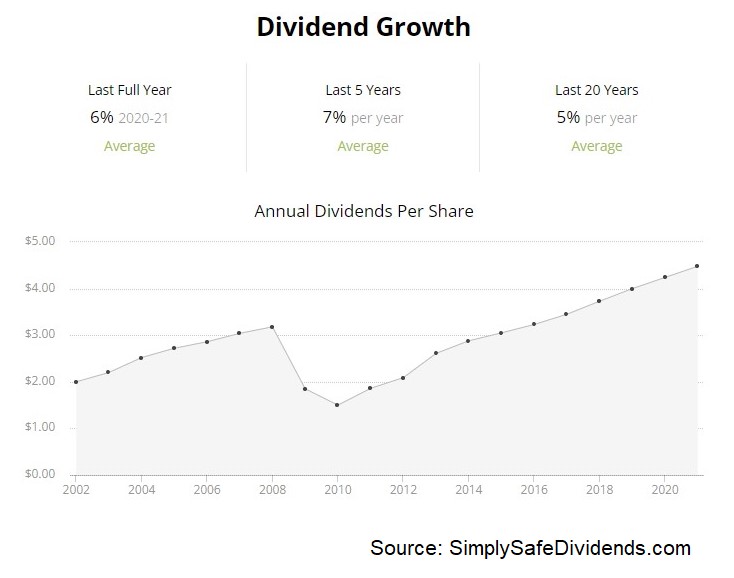

The first stock I want to highlight today is Alexandria Real Estate Equities Inc. (ARE).

Alexandria Real Estate is a life science and technology real estate investment trust with a market cap of $26 billion.

So what’s happened here with Alexandria Real Estate is that they’ve been lumped in with office building REITs, which have largely been shunned by the market over the last two or so years in the face of a pandemic that caused office buildings to empty out.

Office buildings still haven’t really recovered. However, Alexandria Real Estate isn’t your typical office building REIT. Its properties are highly specific, built-for-purpose laboratories that can’t be replicated in a coffee shop or someone’s extra bedroom. As such, their property portfolio features an occupancy rate of nearly 95% and a rent collection rate of 99.9%. Rock-solid property portfolio. Rock-solid dividend.

The REIT has increased its dividend for 12 consecutive years.

This name flies under the radar. Nonetheless, the dividend metrics are actually great. The 10-year DGR is 9.3%, which is rather high for a REIT. Plus, you get a 3% yield right now. Now, recent dividend increases have been somewhat smaller. And I can’t fault management for being prudent during such a strange period in life and business. But the dividend commitment has clearly never wavered. And with the dividend only sucking up 56.1% of this fiscal year’s expected adjusted funds from operations per share at the midpoint, it’s one of the safest dividends in REITdom.

This name flies under the radar. Nonetheless, the dividend metrics are actually great. The 10-year DGR is 9.3%, which is rather high for a REIT. Plus, you get a 3% yield right now. Now, recent dividend increases have been somewhat smaller. And I can’t fault management for being prudent during such a strange period in life and business. But the dividend commitment has clearly never wavered. And with the dividend only sucking up 56.1% of this fiscal year’s expected adjusted funds from operations per share at the midpoint, it’s one of the safest dividends in REITdom.

Talk about getting hammered. This stock is down 29% from its 52-week high.

Like I said, Alexandria Real Estate got caught up in the herd fleeing away from office building REITs. But not all REITs are created equal. Every business is different. And this REIT has unique, high-value laboratories that continue to be in demand from some of the biggest companies in healthcare that need to continue investing in research and development. The stock’s 52-week high is $224.95. Its current pricing of $160, as I write this article, is nowhere near that. The stock’s P/CF ratio of 23 is off of its own five-year average of 25.7, indicating some undervaluation. This one is worth a good look right now.

Next up, let’s quickly talk about Franklin Resources, Inc. (BEN).

Franklin Resources is a multinational investment manager with a market cap of $14 billion.

The asset management business model is fantastic. If you run it correctly, you basically can’t lose. That’s because your fee base – the global assets that you’re managing – are in a rising tide lifting all boats. High-quality global assets are typically rising over the long run, which increases your fee base, which, in turn, increases the fees you can earn. This is why Franklin Resources has a great track record for paying out a safe, growing dividend.

The investment manager has increased its dividend for 42 consecutive years.

Yep. This is a Dividend Aristocrat. It’s been increasing its dividend for longer than I’ve even been alive for. And I’m no longer some young spring chicken. The 10-year DGR is 12.9%, which is impressive, but more recent dividend increases have been in the low-single-digit range. That said, the yield is 4.2%. So this stock basically has utility-like yield and dividend growth metrics, which is right in the wheelhouse of income-oriented dividend growth investors. And with the payout ratio sitting at 31.2%, we’ve got a healthy dividend here.

Yep. This is a Dividend Aristocrat. It’s been increasing its dividend for longer than I’ve even been alive for. And I’m no longer some young spring chicken. The 10-year DGR is 12.9%, which is impressive, but more recent dividend increases have been in the low-single-digit range. That said, the yield is 4.2%. So this stock basically has utility-like yield and dividend growth metrics, which is right in the wheelhouse of income-oriented dividend growth investors. And with the payout ratio sitting at 31.2%, we’ve got a healthy dividend here.

This stock has been creamed – down 28% from its 52-week high. And it didn’t even look all that expensive before the drop.

What’s happened here is that a cheap stock got even cheaper. And that happens. Just because a stock looks cheap from every angle, that’s not to say that it won’t go down. There’s no rule against cheap getting cheaper. But if you like a stock at one price, all else equal, you should like it even more when it’s priced much lower. Indeed, the 52-week high for this one is $38.27. The stock is now hovering around $28.

What’s happened here is that a cheap stock got even cheaper. And that happens. Just because a stock looks cheap from every angle, that’s not to say that it won’t go down. There’s no rule against cheap getting cheaper. But if you like a stock at one price, all else equal, you should like it even more when it’s priced much lower. Indeed, the 52-week high for this one is $38.27. The stock is now hovering around $28.

Most basic valuation metrics are now in deep discount territory. The P/E ratio is 8.2. Yes. 8.2. Even for a stock that’s typically pretty cheap, that’s ludicrously low. Its five-year average P/E ratio is 14.8. Most basic valuation metrics are nearly half of their respective recent historical averages. Franklin Resources is worth consideration, if not capital right now.

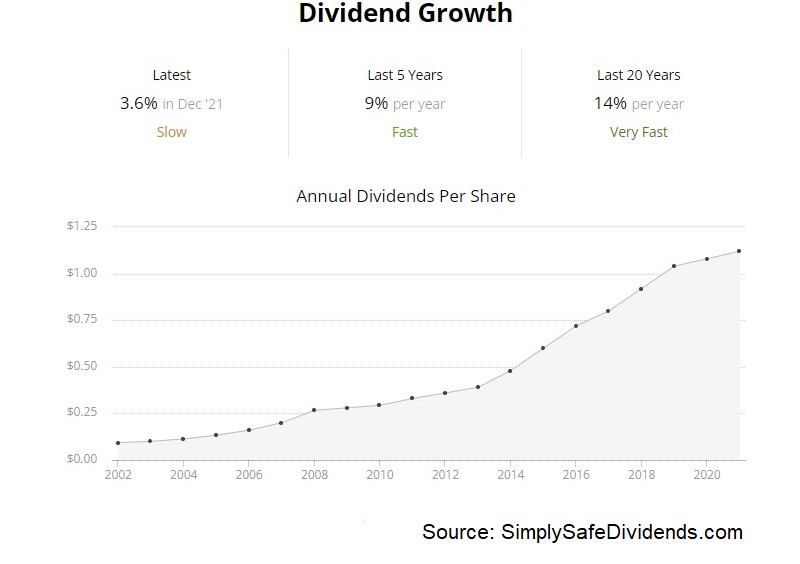

The third stock I want to bring to your attention today is Evercore Inc. (EVR).

Evercore is an investment banking advisory firm with a market cap of $4 billion.

Another financial firm here. Is that a surprise? The financial industry is littered with great businesses making money in the most obvious place to make money – money itself. Since it’s in the advisory space, Evercore makes money whether assets are going up or down. And I must say, Evercore has been growing like a weed. That’s true for the business. And it’s also true for the dividend.

The advisory firm has increased its dividend for 16 consecutive years.

Their 10-year DGR is 13.6%. Good stuff. Plus, the stock yields 2.9%. Even better. If every stock I ever bought gave me a 3% yield and double-digit long-term dividend growth, I’d be a pretty happy camper. Oh, and we’ve got a super, super low payout ratio of only 17.2%. That means this dividend is likely headed for – yep, you guessed it – more double-digit growth.

With the stock down 39% from its 52-week high, it’s time to take a look.

The stock’s 52-week high is $164.63. It’s currently priced at $101. Huge fall. But we have to keep in mind that M&A and various corporate actions went into overdrive during the pandemic. All of that has cooled down, so it’s not a surprise to see the stock also cooling down. That said, the stock is priced below where it was in 2018 – despite the business making a lot more money and paying out a much larger dividend today than it was back then.

The stock’s 52-week high is $164.63. It’s currently priced at $101. Huge fall. But we have to keep in mind that M&A and various corporate actions went into overdrive during the pandemic. All of that has cooled down, so it’s not a surprise to see the stock also cooling down. That said, the stock is priced below where it was in 2018 – despite the business making a lot more money and paying out a much larger dividend today than it was back then.

The P/E ratio has been pushed down to 6. Let me repeat that. The stock’s P/E ratio is just 6. Its five-year average P/E ratio of 14.8 is, in and of itself, not all that high. It’s now less than half of that. Evercore is very interesting here. It’s time to take a good look at it.

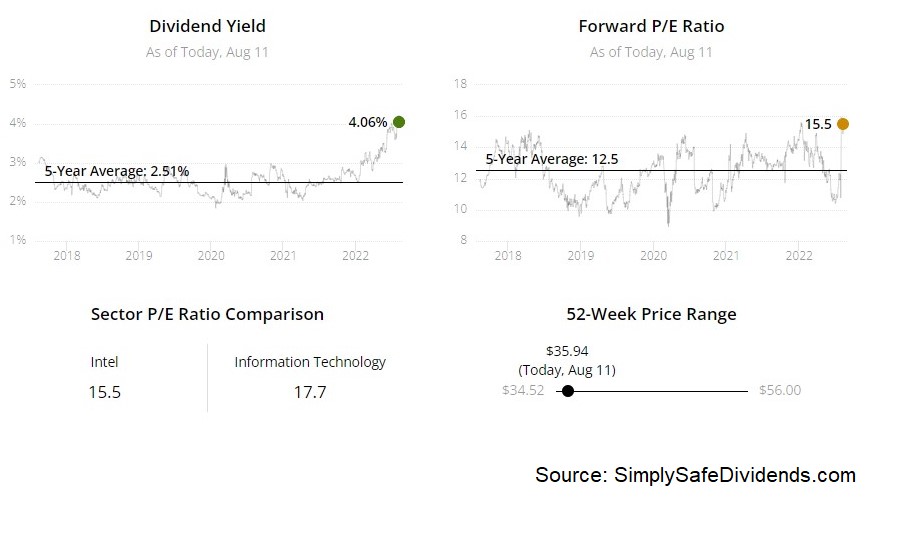

The fourth stock I want to discuss today is Intel Corporation (INTC).

Intel Corporation is a multinational technology company with a market cap of $145 billion.

Intel, Intel, Intel. This name has been in the dog house for a while now. And for good reason. A few lackluster management teams, poor capital allocation, complacency, and a lack of innovation in the face of aggressive competition have all conspired to knock this business down a few notches from its legendary perch. I’ll be honest. Intel isn’t my favorite tech company by a long shot.

It’s not even my favorite business in the semiconductor space. But let’s be clear. Intel still makes a ton of money. We’re talking nearly $80 billion in annual revenue and nearly $20 billion in annual net income. That kind of money has a way of trickling down into a very nice dividend for shareholders.

The tech company has increased its dividend for eight consecutive years.

Intel’s dividend growth track record isn’t the best out there. But it’s also not bad at all. Their five-year DGR is 6%. And that’s something they’ve been pretty consistent with. You’re pairing that 6% dividend growth with the stock’s current yield of 4.1%. If you’re the kind of dividend growth investor who tilts more toward income than the growth side of things, that’s interesting. And despite all of Intel’s stumbling around, because they just make gobs of money, the payout ratio is still only 31.3%. That gives them plenty of flexibility around the dividend.

Intel’s dividend growth track record isn’t the best out there. But it’s also not bad at all. Their five-year DGR is 6%. And that’s something they’ve been pretty consistent with. You’re pairing that 6% dividend growth with the stock’s current yield of 4.1%. If you’re the kind of dividend growth investor who tilts more toward income than the growth side of things, that’s interesting. And despite all of Intel’s stumbling around, because they just make gobs of money, the payout ratio is still only 31.3%. That gives them plenty of flexibility around the dividend.

Is this the best stock out there? No. But it is one of the cheapest after a 37% drop from its 52-week high.

Frankly, I think this name is cheaper than it deserves to be. Does Intel deserve a below-market earnings multiple? I’d argue it does. At least, until they can prove out their big bet on fabrication. However, we are much, much lower than the market. The S&P 500’s P/E ratio is about 20 right now. Intel’s five-year average P/E ratio is 13.1. Okay. But get this. Intel’s current P/E ratio, right now, is 7.6.

Frankly, I think this name is cheaper than it deserves to be. Does Intel deserve a below-market earnings multiple? I’d argue it does. At least, until they can prove out their big bet on fabrication. However, we are much, much lower than the market. The S&P 500’s P/E ratio is about 20 right now. Intel’s five-year average P/E ratio is 13.1. Okay. But get this. Intel’s current P/E ratio, right now, is 7.6.

We’re not looking at simply a below-market earnings multiple here. We have an earnings multiple that is almost 1/3 that of the market. Intel’s 52-week high is $56.28. And the stock didn’t look buyable up there. But with the stock priced at slightly over $35 here, it sure looks a lot more buyable now – especially with the company set to benefit in a major way from the CHIPS Act. Intel is worth a close look.

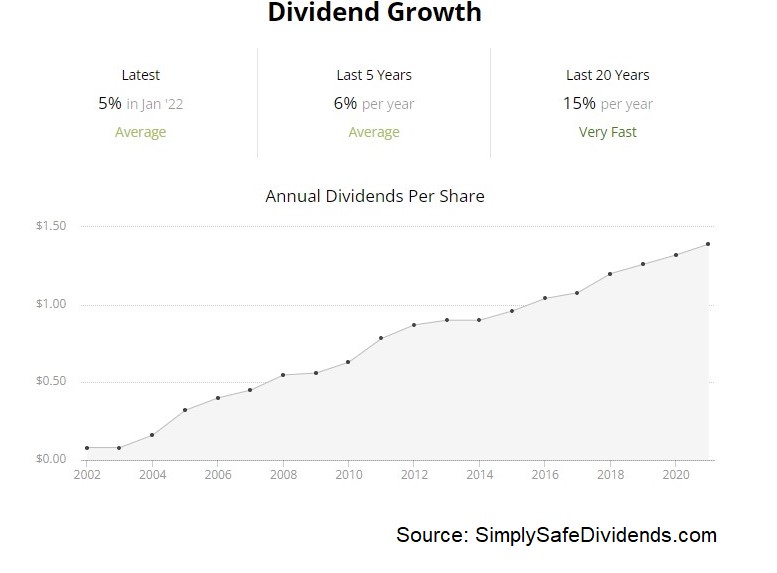

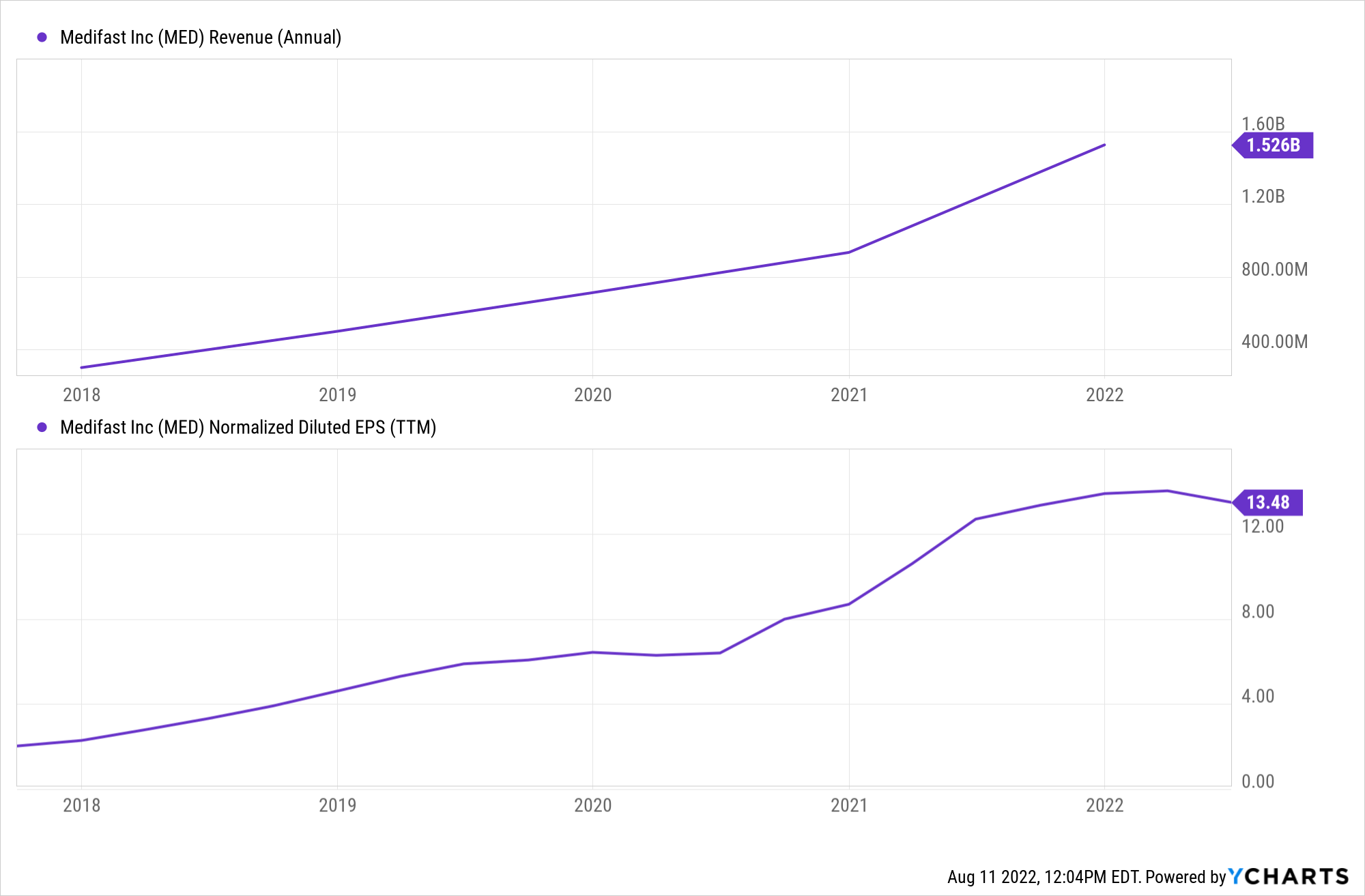

Last but not least, let’s quickly talk about Medifast Inc. (MED).

Medifast is a nutrition and weight loss company with a market cap of $1.5 billion.

Let’s be clear about what Medifast isn’t. It’s not a blue-chip business. It’s not a widows-and-orphans, sleep-well-at-night, pass-down-to-your-grandkids type of investment. This is a MLM business involved in selling weight loss products. It’s a bit speculative. But risk and reward tend to go hand in hand. I will say, Medifast has been growing like gangbusters. Over the last five years alone, revenue and EPS have more than quintupled. That massive business growth has fueled massive dividend growth.

The weight loss company has increased its dividend for seven consecutive years.

The weight loss company has increased its dividend for seven consecutive years.

Medifast is new to the dividend growth game. But they’re off to a fast start. Their five-year DGR is a whopping 40.1%. And it’s not just growth here. The stock also yields 4.8%. If you know of a stock with a higher yield that also offers a higher five-year DGR, I’d love to hear about it – because I don’t know of anything that tumps this. The payout ratio of 48.7% is still quite moderate, even after all of those huge dividend increases.

This stock is down – get this – 54% from its 52-week high.

Medifast was a bit of a pandemic darling. And they’re adapting to a resetting of sales and growth expectations amid demand reduction and supply chain disruptions. The stock’s 52-week high of $295.38 is RIP. It’s dead. We’re now looking at a $136 stock. I feel for anyone who bought the stock at that 52-week high. But on a go-forward basis, here at $136, it’s a compelling, if speculative, idea.

The company’s Q2 report, which came out in early August, was a double beat, with 15% YOY revenue growth. But adjusted EPS came in 2.5% lower YOY. Guidance was also lowered. But based on the midpoint of that now-lower guidance for this fiscal year’s adjusted EPS, the forward P/E ratio is only 10.2. That is highly reasonable for what has historically been a fast-growing business currently going through a rough patch. If you don’t mind the risk, this is a fascinating idea after seeing its price get cut in half.

The company’s Q2 report, which came out in early August, was a double beat, with 15% YOY revenue growth. But adjusted EPS came in 2.5% lower YOY. Guidance was also lowered. But based on the midpoint of that now-lower guidance for this fiscal year’s adjusted EPS, the forward P/E ratio is only 10.2. That is highly reasonable for what has historically been a fast-growing business currently going through a rough patch. If you don’t mind the risk, this is a fascinating idea after seeing its price get cut in half.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

The company manufacturing Nvidia's AI servers trades under a secret name. AI revenue: $30B this year. Stock price: $8. Click for the hidden identity →

Source: Dividends & Income