Dividend growth investing is like the gift that keeps on giving. Except it’s better than that. It’s the gift that keeps giving more… and more… and more. That’s right.

High-quality dividend growth stocks are stocks that consistently increase their dividends.

So dividend growth investors don’t just look forward to getting paid to sit on their hands and own shares. No.

They look forward to getting paid ever-larger dividends, year in and year out, like clockwork.

Since inflation means the price of everything is going up over time, you want to make sure your passive income can keep up.

Well, many high-quality dividend growth stocks are growing their dividends even faster than inflation. That means your purchasing power actually increases over time.

Today, I want to tell you about six dividend growth stocks that just increased their dividends. Ready? Let’s dig in.

The first dividend increase I want to tell you about came from Amgen (AMGN).

Amgen just increased their dividend by 10.2%.

Whenever I see Amgen, I almost read it as Amgem. Because this business is a gem. All it seems to do is make more money and reward shareholders with bigger dividends. How can you not love this?

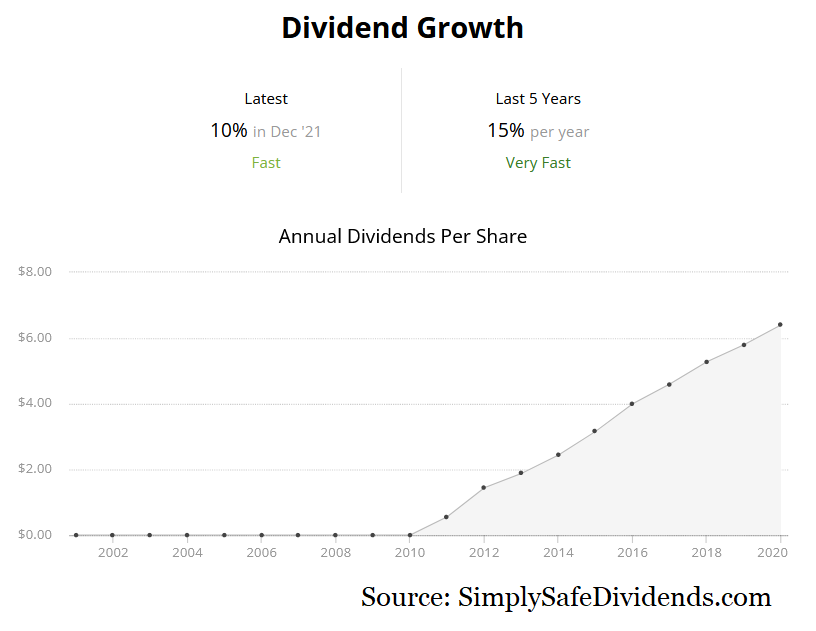

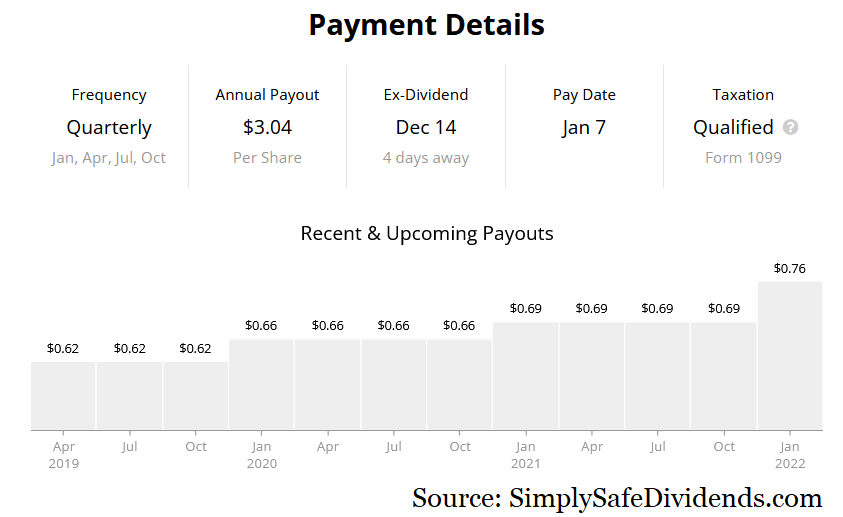

This marks the 12th consecutive year of dividend increases for the global biotechnology company.

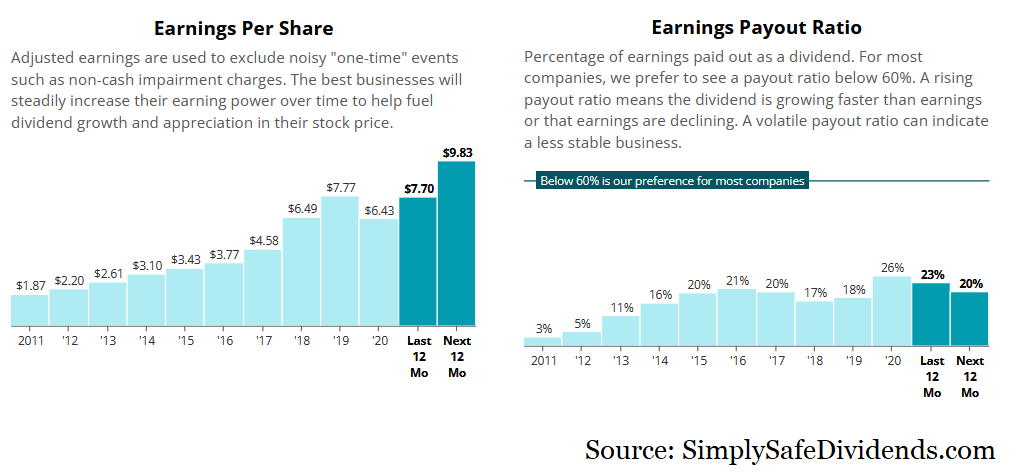

This dividend increase does trail the five-year DGR of 15.2%, but investors can’t expect that kind of dividend growth to persist forever. This 10.2% dividend increase actually came in higher than my own expectations, which were in the high-single-digit range. The stock now yields a very appealing 3.7%, which is well above its five-year average. And the payout ratio is only 46.2%, based on midpoint adjusted EPS guidance for this fiscal year, which gives them room to continue generously raising the dividend for the foreseeable future.

This dividend increase does trail the five-year DGR of 15.2%, but investors can’t expect that kind of dividend growth to persist forever. This 10.2% dividend increase actually came in higher than my own expectations, which were in the high-single-digit range. The stock now yields a very appealing 3.7%, which is well above its five-year average. And the payout ratio is only 46.2%, based on midpoint adjusted EPS guidance for this fiscal year, which gives them room to continue generously raising the dividend for the foreseeable future.

I think Amgen’s stock is a bona fide steal right now.

I analyzed and valued Amgen only days ago, showing my estimate of intrinsic value at nearly $250/share. And that video came out before the dividend increase came through, which makes the stock that much more attractive. With the stock currently at less than $210, there could be a lot of upside here. If you’re not already loaded up on Amgen, consider changing that.

The second dividend increase I have to highlight is the one that was announced by Eastman Chemical Company (EMN).

Eastman Chemical just increased their dividend by 10.1%.

Another high-quality dividend growth stock. Another double-digit dividend increase. These are like “pay raises” that you don’t have to do anything at all to receive, other than simply sit on your hands and not sell your stock. It doesn’t get any easier than that, folks.

This is the 12th consecutive year in which the chemical company has increased its dividend.

Their 10-year dividend growth rate is 11.6%, so this dividend increase was right on the money. The stock now yields 2.8%, which easily beats the market and is right in line with the stock’s own five-year average yield. With the payout ratio at only 34.2%, based on midpoint adjusted EPS guidance for this fiscal year, you already know that this dividend is headed even higher from here.

Their 10-year dividend growth rate is 11.6%, so this dividend increase was right on the money. The stock now yields 2.8%, which easily beats the market and is right in line with the stock’s own five-year average yield. With the payout ratio at only 34.2%, based on midpoint adjusted EPS guidance for this fiscal year, you already know that this dividend is headed even higher from here.

After some decent performance this year, the stock looks fairly valued to me.

It’s up about 11% this year, before the dividend. And that’s not bad at all for a boring chemical business. I like Eastman Chemical, but I see it as fully valued here. Most basic valuation metrics are in line with, or even higher than, their respective recent historical averages. The P/CF ratio, for instance, is 9.4. That’s not egregious at all in this market. But it is higher than its five-year average of 8.2. I’d keep it on my radar, but it’s not a name I’d be going crazy over.

Third up is the dividend increase that came from Mastercard (MA).

Mastercard just increased their dividend by 11.4%.

A double-digit increase in income for doing nothing other than sitting on shares. Isn’t that beautiful? Actually, it’s a double-digit increase in passive income. So you take something awesome – passive income – and amplify its awesomeness by increasing it.

The international financial services company has now increased its dividend for 11 consecutive years.

The five-year DGR of 20.1%, which is outstanding, might have set up shareholders for higher expectations here, but I doubt anyone is all that disappointed with an 11.4% boost in their passive dividend income. Of course, this is the kind of stock that you really do want to see double-digit dividend growth from, because it only yields 0.6%. This is more of a long-term compounder than an income play, so you’re betting on that growth. Well, they’re set up to deliver a lot more of that. With a payout ratio of 24.1%, I expect many more sizable dividend increases in the future.

This stock has recently pulled back, and it looks just about fairly valued here.

Mastercard typically sports a high-flying valuation. And with a P/E ratio of 41, it still sports a high-flying valuation. And you could argue it deserves it – this stock is up 750% over the last decade! That said, this stock can go through periods of somewhat extreme valuation, where it just becomes far too expensive. Indeed, this stock was over $400 this summer. But it’s cooled down somewhat, and Mastercard is now at about $333/share. The valuation doesn’t scream “cheap” by any measure. But many multiples are in line with their respective recent historical averages. Mastercard actually looks buyable here. Take a look at it, if you haven’t already.

Mastercard typically sports a high-flying valuation. And with a P/E ratio of 41, it still sports a high-flying valuation. And you could argue it deserves it – this stock is up 750% over the last decade! That said, this stock can go through periods of somewhat extreme valuation, where it just becomes far too expensive. Indeed, this stock was over $400 this summer. But it’s cooled down somewhat, and Mastercard is now at about $333/share. The valuation doesn’t scream “cheap” by any measure. But many multiples are in line with their respective recent historical averages. Mastercard actually looks buyable here. Take a look at it, if you haven’t already.

The fourth dividend increase I want to bring to your attention is the one that came in from McCormick & Company (MKC).

McCormick just increased their dividend by 8.8%.

Imagine waking up to news that one of your investments is now going to pay your more passive dividend income. And all you have to do in order to get this pay raise is continue existing and not sell stock. That’s another day in the life of a dividend growth investor.

This is the 35th consecutive year in which the food company has increased its dividend.

McCormick is famous for their spices. Well, they ought to be just as famous for the spicy dividend increases they keep handing out to shareholders. The 10-year DGR of 9.1% basically telegraphed the size of this most recent dividend increase, so no surprises there. The yield of 1.6% is healthy, and that’s slightly higher than the stock’s own five-year average yield, although this one leans more toward that long-term compounding and growth than current income. Since the payout ratio remains a moderate 52.5%, I foresee many more spicy dividend increases to come.

The stock is actually down on the year, and this could be a rare opportunity for accumulation.

The stock is actually down on the year, and this could be a rare opportunity for accumulation.

This stock is one that looks almost perpetually expensive in terms of valuation. But it’s been basically flat since the summer of 2020, even while the business continues to advance. And this could be a rare opportunity for those looking to buy in. Now, I’m not saying the stock is cheap in any way. But it’s far more reasonable than it usually is. And that might be enough. The P/E ratio of 32.1 is tough to swallow, but this stock typically commands an earnings multiple near 30. I’d definitely have it on my radar.

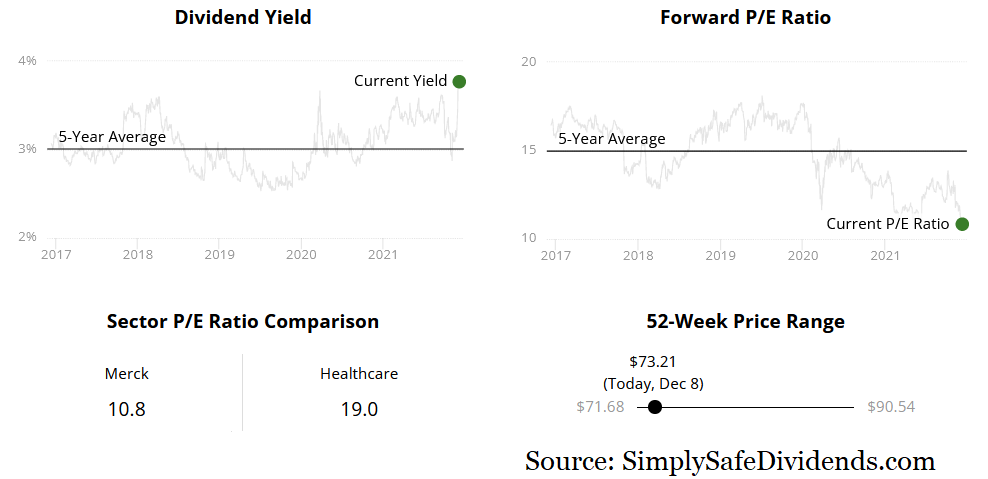

I now want to share with you the dividend increase that was announced by Merck & Co.(MRK).

Merck just increased their dividend by 6.2%.

It’s not as impressive as what Amgen delivered, but this is still a very nice increase in one’s passive dividend income. It beats inflation. And remember, shareholders did nothing to get it other than, well, hold shares.

This marks the 11th consecutive year of dividend increases for the global pharmaceutical company.

And I think they’re really just getting warmed up. This dividend increase was pretty much right in line with my own expectations, and it’s right in line with the five-year DGR of 6.3%. Along with that growth, you get a yield of 3.8% that handily beats the market. And the payout ratio, at 48.7%, based on their adjusted EPS guidance for this fiscal year at the midpoint, indicates no trouble whatsoever with covering the dividend and being able to continue increasing it.

The stock is down 5% YTD, and I see it as materially undervalued right now.

To my eye, Merck looks like one of the best deals out there. Every basic valuation metric indicates cheapness. And this is despite the business doing well, and the fact that Merck is selling billions of dollars worth of a COVID-19 therapeutic. They’re getting no credit for that at all. If anything, it’s worse than no credit – it’s negative credit. The stock is still priced below where it was in early 2020, before the pandemic hit. I called out Merck as an undervalued high-quality dividend growth stock in early September, revealing my estimate of intrinsic value at slightly over $92/share. At less than $74/share, I think there’s significant upside.

To my eye, Merck looks like one of the best deals out there. Every basic valuation metric indicates cheapness. And this is despite the business doing well, and the fact that Merck is selling billions of dollars worth of a COVID-19 therapeutic. They’re getting no credit for that at all. If anything, it’s worse than no credit – it’s negative credit. The stock is still priced below where it was in early 2020, before the pandemic hit. I called out Merck as an undervalued high-quality dividend growth stock in early September, revealing my estimate of intrinsic value at slightly over $92/share. At less than $74/share, I think there’s significant upside.

Last but not least, let’s talk about the dividend increase that was handed out by WEC Energy Group (WEC).

WEC Energy just increased their dividend by 7.4%.

Good stuff, especially considering that this is a utility. Who said that utilities are boring or can only post up modest growth? If getting a 7%+ boost in your passive dividend income is boring, I’d like to see exciting. Also, there’s nothing modest about high-single-digit growth.

The electricity and natural gas utility company has now increased its dividend for 19 consecutive years.

Almost two straight decades of ever-higher dividends. That’s consistent. Also consistent is the rate at which they do it – the five-year DGR is 7.7%, so they’re bang on with this most recent dividend increase. The stock also yields 3.2%, so there’s plenty of both income and growth here. The payout ratio, at 70.1%, is high, but not out of line for a utility. These are very good dividend metrics.

Almost two straight decades of ever-higher dividends. That’s consistent. Also consistent is the rate at which they do it – the five-year DGR is 7.7%, so they’re bang on with this most recent dividend increase. The stock also yields 3.2%, so there’s plenty of both income and growth here. The payout ratio, at 70.1%, is high, but not out of line for a utility. These are very good dividend metrics.

This is a stock that can be expensive at times, but I actually see it as reasonably valued here.

This utility typically gets a premium valuation, due to its premium quality. That premium can sometimes become a bit too much. But it’s pulled back a bit of late, and it now looks sensible. I’m not saying it’s a steal. Far from it. But the P/E ratio is 22.2. That lines up almost exactly with its five-year average earnings multiple of 22.1. This company has one of the best, and most consistent, growth profiles of any utility out there. If your portfolio needs a quality utility business, it’s worth taking a good look at this name.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com