Every day of every year is a great opportunity to increase your wealth and passive income.

But the start of a new year is a particularly good time to look at investment ideas that could hold the potential to deliver better results than most other investment ideas available.

With this in mind, I’m going to reveal my top 5 stock ideas for 2022! Let’s say you have $5,000 that you’d like to spread across five different stocks. Well, you might want to take a good look at this list.

Now, keep in mind that I’m a long-term investor, and these are long-term investment ideas. I think all five stocks will do very well over the next 10+ years. And when I think about investing in these businesses, that’s the kind of time horizon I have in mind.

However, I think each stock is especially attractive at this point in time due to a variety of reasons that apply to each specific business, such as growth, valuation, yield, fundamentals, and competitive advantages.

As a result, I think they’ll do well over both the short term and long term. That’s a win-win.

I’ve personally invested in stocks just like these on my way to going from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint. If you’re interested, you can download a free copy of my Early Retirement Blueprint here.

If your aim is to build your wealth and passive income, become financially independent, and potentially even retire early in life, these stocks could help you do all of that. Ready? Let’s dig in.

Before the big reveal, I want to tell you three important things about these five stocks.

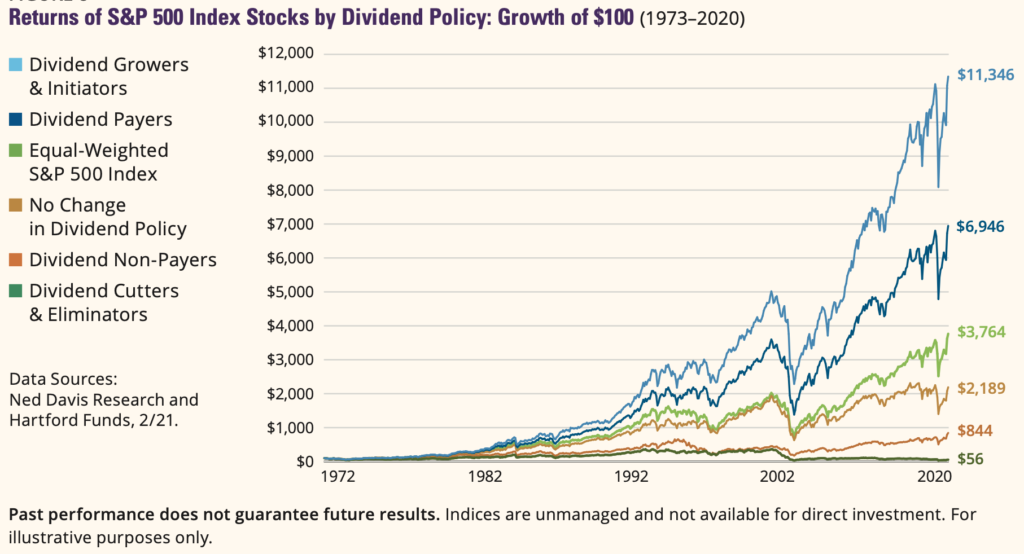

First, they’re all dividend growth stocks.

Dividend growth stocks tend to outperform the broader market over the long run.

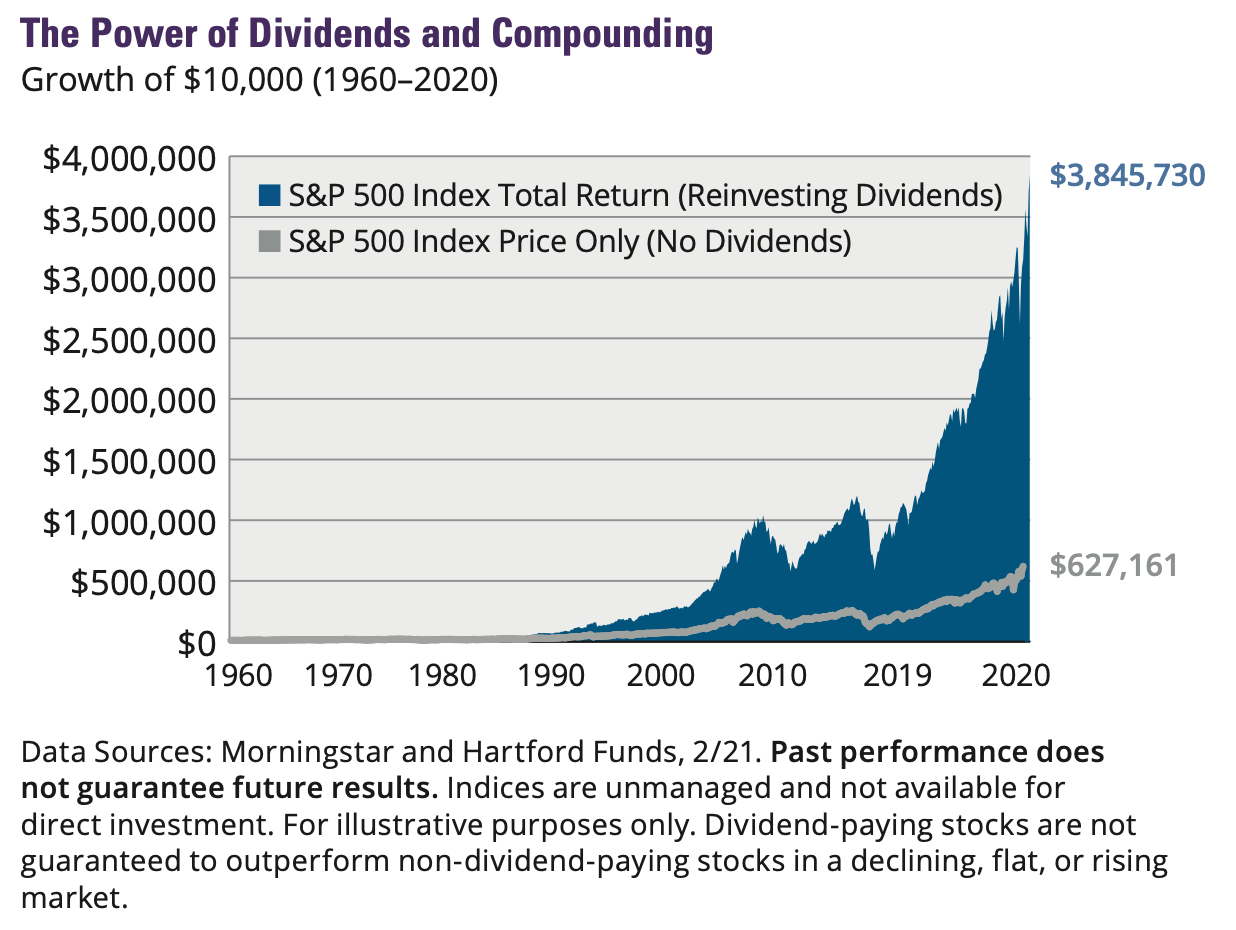

It’s easy to understand why. Dividends aren’t simply a component of the market’s total return over the long term; dividends are the main component. And reinvesting growing dividends intensifies that effect.

It’s easy to understand why. Dividends aren’t simply a component of the market’s total return over the long term; dividends are the main component. And reinvesting growing dividends intensifies that effect.

Second, they’re all high-quality businesses.

Every business I’m going to discuss has excellent fundamentals and durable competitive advantages. It’s one thing to be a dividend growth stock. It’s quite another thing to be a wonderful business. A growing dividend can, and often does, serve as a great initial litmus test for business quality. That’s because only a strong business that’s producing growing profit can sustain a growing cash dividend for years on end. But it definitely isn’t the only thing to look for.

To that point, every business I’m highlighting has brisk top-line and bottom-line growth, robust profitability, a rock-solid balance sheet, impressive dividend growth metrics, and numerous competitive advantages. The importance of business quality has never been more clear than right now. The last year or so has seen an acceleration of trends worldwide. And businesses that aren’t healthy and nimble are getting left behind.

Third, they all appear to be attractively valued.

Even the best stock in the world can be a poor investment, especially over a shorter period of time, if an investor pays far too much. But if one is able to invest in a great business at a great value, they’re setting themselves up for truly outstanding investment performance. That outstanding investment performance is possible over the short term, but it’s almost certain over the long term.

Now my top five stocks for 2022.

Stock #1 is Allstate (ALL).

Allstate is an insurance company that operates as one of the largest property-casualty insurers in the United States.

After being founded in 1931, they’ve grown into an insurance powerhouse with a market cap of $31 billion. They’re one of the biggest and best insurers in the US. They have a great balance sheet. And economies of scale, brand recognition, and the float are durable competitive advantages that protect the business. Regarding that last point – the float – the prospect for rising rates is a big catalyst here, as that would be a tailwind for their investment portfolio in terms of the net income the business can produce.

But even without rising rates, this is an all-star business.

They’ve increased revenue at a CAGR of 3.6% and EPS at a CAGR of 28.9% over the last decade. That great long-term business performance should lead to great long-term stock performance, right? Well, right you are. This stock is up more than 300% over the last 10 years – a 10-year period, by the way, that didn’t include rising rates. Also sporting great performance is the dividend. The company has increased its dividend for 11 consecutive years, with a 10-year DGR of 10.2%.  Along with that double-digit growth comes a 3% yield – which is 120 basis points higher than the stock’s own five-year average yield. And the dividend is protected by a very low payout ratio of 25.9%. Insurance has long been one of Warren Buffett’s favorite business models. Well, it’s one of my favorites, too. And you can probably see why.

Along with that double-digit growth comes a 3% yield – which is 120 basis points higher than the stock’s own five-year average yield. And the dividend is protected by a very low payout ratio of 25.9%. Insurance has long been one of Warren Buffett’s favorite business models. Well, it’s one of my favorites, too. And you can probably see why.

This stock is flat for 2021, but 2022 could be the year in which it moves a lot higher.

Since May of 2021, all this stock has done is gone down – it’s now 23% off of its 52-week high. This is despite the business knocking it out of the park with earnings reports. I see this temporary disconnect between business performance and stock performance as a tremendous opportunity and something that should right itself in the near future. While business performance and stock performance tend to correlate over the long run, as I pointed out earlier, there can be short-term disconnects.

Indeed, every basic valuation metric is significantly lower than its respective recent historical average, including the P/E ratio of 10.1. I actually analyzed and valued this stock in mid-October, estimating intrinsic value at nearly $150/share. In that video, CFRA ranks the stock as a five-star “STRONG BUY”, with a 12-month target price of $160! That’s 48% higher than the current price of slightly over $108. The valuation provides support and upside. And even a whiff of higher rates could send the stock rocketing higher. So this one has valuation and macroeconomic catalysts.

Stock #2 is Enbridge (ENB).

Enbridge is an energy distribution and transportation company.

Founded in 1949, now with a market cap of $75 billion, this is the largest energy infrastructure company in North America. Enbridge operates the world’s longest and most complex crude oil and liquids transportation system. It shouldn’t be a surprise to see durable competitive advantages here, including massive scale and extremely high barriers to entry. Simply put, it would be almost impossible to build a competing pipeline network from scratch today. The company also has an investment-grade balance sheet.

I think Enbridge is a no-brainer investment here.

Business growth over the last decade has been great. Revenue has a CAGR of 8.1% over the last 10 years, while the bottom line has compounded at an annual rate of 8.3%, in per share terms, over that time frame. This has helped them to produce outstanding dividend metrics. I’m talking 25 consecutive years of dividend increases, a 10-year dividend growth rate of 11.3%, and a payout ratio of 68.9%.

But wait. There’s more. The stock yields 7.1% here. Where else will you get a 7%+ yield and a 10%+ dividend growth rate? And with a sudden, shall we say, renewed appreciation for traditional, non-renewable energy products after an energy scare in Europe, Enbridge could be given a bit more regulatory slack than usual.

This name is positioned for for great short-term and long-term performance.

This name is positioned for for great short-term and long-term performance.

Regarding the short term, it’s had a nice run in 2021 – up almost 17% YTD. However, it’s down 14% from its 52-week high, reached only a month ago in early November. This is due for a bounce, because it didn’t look expensive even when it was over $40/share. In fact, I analyzed and valued Enbridge in late November, showing how shares could be worth nearly $48/each. With the stock currently at around $37/share, looking 30% undervalued, I see a lot of upside here – short term and long term.

Stock #3 is Johnson & Johnson (JNJ).

Johnson & Johnson is a global healthcare conglomerate.

This $420 billion (by market cap) company, which can trace its roots back to its founding in 1886, is about to experience, perhaps, its biggest transformation ever. The company announced that it will split into two businesses in 2023 – one business focused on pharmaceuticals and medical devices, and the other focused on consumer products. Meanwhile, this super high-quality, blue-chip company enjoys one of only two AAA credit ratings in the world. And their durable competitive advantages are incredibly strong, including global scale, IP, R&D, switching costs, entrenched products, brand recognition, and established healthcare relationships.

This company has one of the most impressive dividend resumes you’ll ever see.

Where do we start? How about 59 consecutive years of dividend increases? They’re a Dividend Aristocrat and a Dividend King. The 10-year DGR of 6.6% is something they’re uniquely consistent with. And the stock offers a market-beating 2.7% yield to boot. With a payout ratio of 43.3%, based on adjusted EPS guidance for this year, the dividend is easily covered.

All of this dividend goodness is the result of business goodness. Revenue has compounded at 2.7% annually over the last decade, while EPS has a CAGR of 9.7% when using adjusted EPS for FY 2020. Solid numbers. But Johnson & Johnson is especially remarkable in the smooth, consistent way in which they grow the top line and bottom line.

I think this stock is wildly underappreciated here.

I think this stock is wildly underappreciated here.

This was actually one of my top stocks for 2021. With it up only 2% thus far in 2021, it hasn’t been a great year. But the more the business grows, and the longer the stock moves sideways, the more the valuation compresses and acts like a spring ready to explode. Maybe that explosion happens in 2022. Maybe not. This is a long-term investment.

That said, I see the news of their split as a big catalyst to get market participants more interested in this stock, which could cause it to move higher in the short term. With a forward P/E ratio of 16.2, based on adjusted EPS guidance for this year, the stock has an undemanding valuation for the level of business quality and its catalyst potential. Johnson & Johnson might be a boring business, but the next year could prove to be very exciting.

Stock #4 is Lockheed Martin (LMT).

Lockheed Martin is is the world’s largest defense contractor.

Founded in 1912, with a market cap of $92 billion, this company has scale where scale matters. In addition to scale, other durable competitive advantages include high barriers to entry, long-term contracts, unique government relationships, and technological know-how. Plus, the balance sheet is solid. Look, sovereign defense isn’t going anywhere in terms of importance or necessity. If anything, it only becomes more important and necessary over time. With China’s overtures toward Taiwan, and Russia getting aggressive with Ukraine, this is apparent.

All it takes is one geopolitical crisis, and this stock will likely fly higher.

Meanwhile, you collect a market-beating 3.4% yield – 80 basis points higher than the stock’s own five-year average yield. This is a dividend that’s been increased for 19 consecutive years, with a 10-year DGR of 9.8%. And the payout ratio of 51.6% shows us a dividend that’s only going to continue growing for years to come. Also supporting that dividend growth thesis is the business growth. This is a company that’s grown its revenue at a CAGR of 3.9% and EPS at a CAGR of 13.4% over the last 10 years. These are outstanding numbers.

Meanwhile, you collect a market-beating 3.4% yield – 80 basis points higher than the stock’s own five-year average yield. This is a dividend that’s been increased for 19 consecutive years, with a 10-year DGR of 9.8%. And the payout ratio of 51.6% shows us a dividend that’s only going to continue growing for years to come. Also supporting that dividend growth thesis is the business growth. This is a company that’s grown its revenue at a CAGR of 3.9% and EPS at a CAGR of 13.4% over the last 10 years. These are outstanding numbers.

This stock has been basically flat since February 2018. It’s due for a big breakout.

Like Johnson & Johnson, this was another top pick for 2021 that didn’t really perform well. The stock is down very slightly for the year. This is despite Lockheed Martin performing well as a business. Its backlog is $135 billion. And they’re almost a lock for a massive $19 billion Canadian contract with the Canadian government to provide F-35 fighters.

Will the stock explode in 2022? I can’t say for sure. But I think the fact that this stock has been range bound for four years is ridiculous when looking at how the business has grown its revenue, EPS, free cash flow, and dividend materially since late 2017 – when it was trading hands for a similar price to where it is now. I analyzed and valued Lockheed Martin in early November, estimating intrinsic value at almost $449/share.

With the stock at about $334, it looks 34% undervalued right now. The upside potential here is tremendous. In our video, I called Lockheed Martin one of my best long-term ideas. Well, if they win that huge Canadian contract, it could turn out to be one of my best short-term ideas, too.

Stock #5 is Merck & Co. (MRK).

Merck is a leading global pharmaceutical company.

This $185 billion (by market cap) company, founded in 1891, should have an even higher market cap than it does, quite frankly. They maintain a very good balance sheet, sport high margins, and have a number of durable competitive advantages like economies of scale, a global distribution network, patents, IP, and R&D. That’s not all, though. Merck owns one of the world’s best-selling drugs in Keytruda. It’s second only to Humira, and it’s expected to overtake Humira within the next few years. But wait. There’s more. They also offer a COVID-19 therapeutic in the form of molnupiravir, which is a near-term tailwind for them.

If you think that’s neat, check out these dividend metrics.

The stock offers a very appealing yield of 3.8%. That doesn’t just blow away what the broader market offers; it’s nearly 100 basis points higher than the stock’s own five-year average yield. Merck has increased this dividend for 11 consecutive years, most recently only days ago with a nice 6.2% dividend increase. The five-year DGR is 6.3%, so this was right in line for them. And the payout ratio, even after the increase, is only 48.7%, based on midpoint adjusted EPS guidance for this fiscal year. While revenue is essentially flat over the last 10 years, EPS has compounded at an annual rate of 12.7%. These are great numbers, and that’s before getting into any kind of molnupiravir benefit.

This company is selling billions of dollars worth of a COVID-19 therapeutic, but it’s getting no love for it.

This company is selling billions of dollars worth of a COVID-19 therapeutic, but it’s getting no love for it.

The stock is down 5% this year. The current price of a bit over $73/share is well off of the pre-pandemic pricing of around $90/share. The market is pricing the stock as if the company is hurting from the pandemic, when it’s the opposite. To my point, the US federal government has committed to buying $2.2 billion worth of molnupiravir.

Canada’s government is buying an initial 500,000 doses, with an option for 500,000 more. The market is valuing all of this as a giant zero for Merck. Actually, less than zero. This makes no sense. I analyzed and valued Merck in early September. I estimated intrinsic value at slightly over $92/share. And I factored in nothing regarding molnupiravir. That’s free upside.

The stock looks 26% undervalued here. Plus, you get a yield near 4%. This pandemic winner is being treated like a pandemic loser, but I think that could change in 2022 as the market finally starts to recognize the value here.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com