Last week I showed you how to get a 16.4% yield (or “cash on cash return” as we call it) on a single family rental property with a $25,000 investment. Today we’re going to look at what we can do with a little more money.

Last time, when we ran numbers for the featured property, it was under the assumption that you were local to the property and could manage it yourself. But that only works if you have opportunities close to you.

From now on, we’ll run numbers with a property manager baked in the cake… so we’ll be looking at generating passive real estate income for you. Just know that if you can manage it yourself, your returns will be even better.

Let’s say we have $50,000 to work with this time. With this amount we have options available to us that we didn’t have before. A down payment of this size will let us venture into the world of multifamily housing. There are variables in multifamily housing that don’t exist in single family, but in my experience, the risk is almost always worth the reward.

The first difference is that for a multifamily property with 2-4 units you will need to put 25% down. That’s instead of the 20% that we put down on the single-family rental.

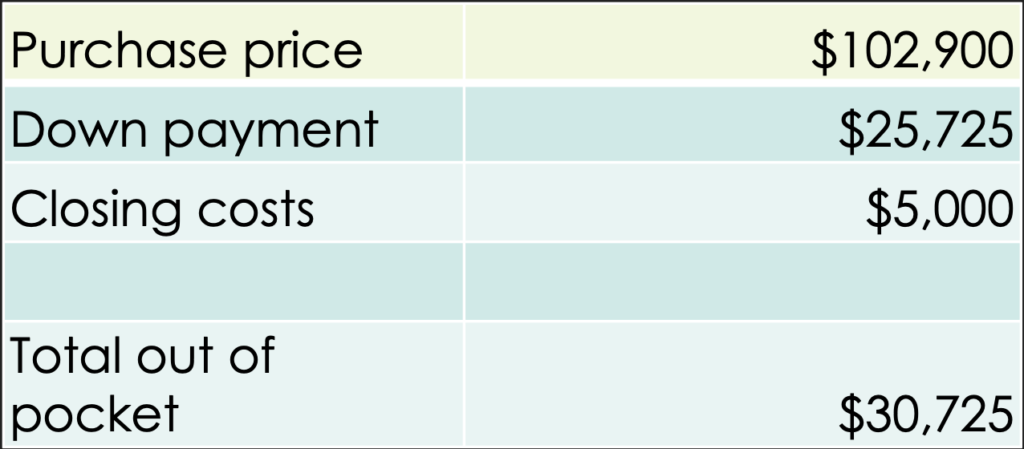

Again, let’s assume we have $50,000 to work with. Our closing costs are going to be $5,000 or 3% of the purchase price, whichever is greater. There will also be some polishing that needs to be done to the property. With this in mind, we’ll need to stay with a purchase price of $175,000 or less.

For the purposes of this article I was able to stay well within our budget and identify a 2 bedroom 1 bathroom / 1 bedroom 1 bathroom duplex on the market in Portsmouth, Virginia that’s for sale with James and Lee Realty for $102,900.

Generate relatively safe double-digit yields investing in properties like this.

A conventional loan for a two-family property like this will require a 25% ($25,725) down payment and have about $5,000 in closing costs.

In Virginia, the rule of thumb on closing costs for a residential purchase with a mortgage is that your closing costs will be 3% of the purchase price or $5,000, whichever is greater. That holds true up to about $600k.

This puts you at $30,725 out of pocket to acquire the property and leaves plenty of money left over to handle any deferred maintenance or repairs that you may have inherited with the property or to make minor updates.

I find that it’s a good practice to meet with your tenants as soon as possible and ask them if they have any issues with the property that need to be addressed and to handle them quickly. This will start your relationship off right and show them that you’re going to be an attentive landlord.

If you’e going to raise rents on existing tenants, it’s important to make visible improvements to the property so that the tenants understand they’re getting something in exchange for the increase in rent.

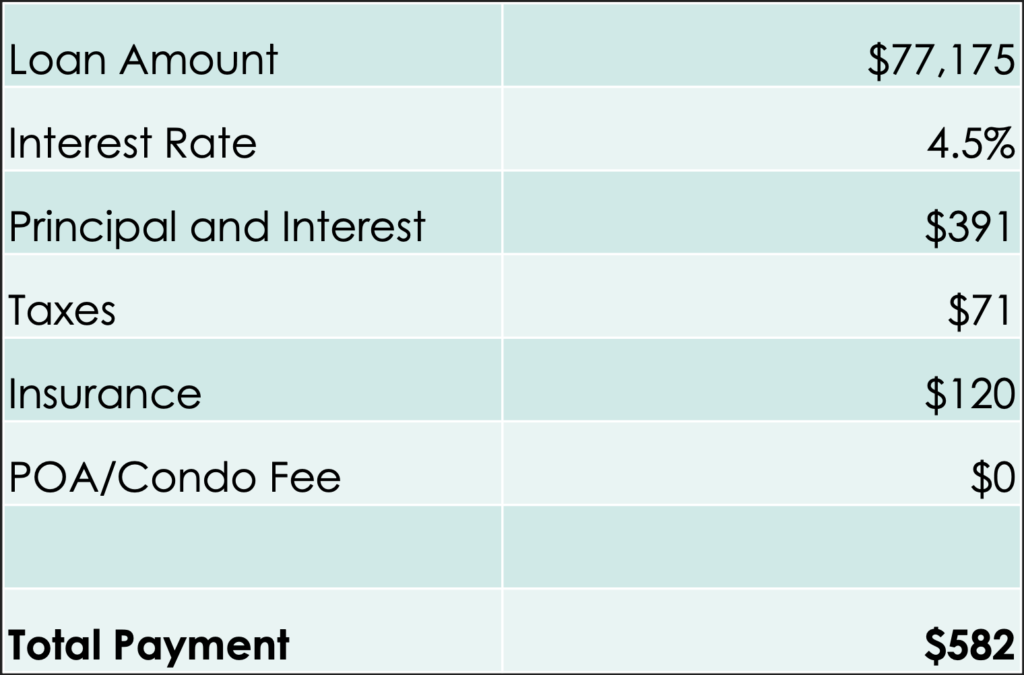

Interest rates on a conventional, non-owner occupied residential property are about 4.5%, and with $25,725 down you would have a loan amount of $77,175.

Your mortgage payment is made up of four items we refer to as PITI: Principal, Interest, Taxes and Insurance. The “P” and “I” portion of your payment would be $391, the taxes on this property are $71 per month and the insurance on a property like this would be about $120 per month, bringing your total monthly payment to $582.

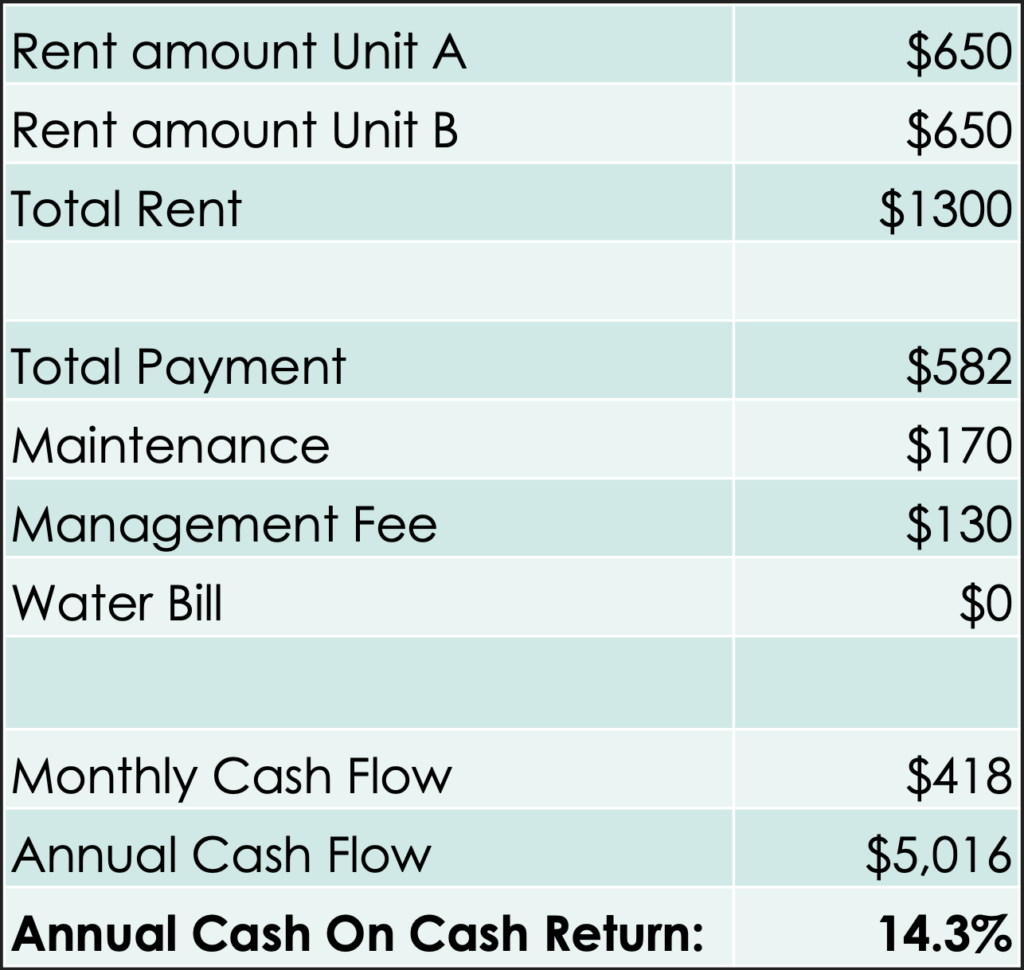

One of the reasons I selected this property is that both units are currently rented for $650 per month each. If you live near the property that you’re purchasing, you can maximize your yield by managing the property yourself. If you’re purchasing remotely, you will inevitably need property management. While that will take a lot of work and stress off of your plate, it will also reduce the yield.

It’s tempting to simply subtract the mortgage payment from the rent and think that will be the monthly cash flow, but it’s critical to not overlook maintenance and repairs. The average property that we manage here at Inlet Realty goes through about $1,000 worth of maintenance annually, so we need to factor in $85 per month per unit for a maintenance budget.

Some properties will have a homeowners’ association or condo association fee that needs to be part of the budget as well. This property doesn’t.

With all expenses accounted for — including management — this property would generate $418 per month in passive income. That’s $5,016 a year, which works out to a 14.3% annual cash on cash return on a $35,000 investment. Without management fees, this property would return over 18% annually cash on cash.

It’s important to note that not all properties make good rentals and so it is critical that each property be underwritten carefully. I like to look at three parts of the property up front, I call them “The Trifecta”, the roof, the windows, and the HVAC. When these items fail, replacing them adds little value to the home and nothing to the amount of the rent you receive, yet you must do them and none of them are cheap.

This particular property has a nice, architectural shingle roof in the middle of its lifespan and the windows are older but in good condition. The HVACs in this property are heat pumps and are in the middle of their life.

With multifamily properties you will have items to evaluate that are not present in single family properties. Frequently in multifamily buildings the units will have separate electric meters but one water meter.

Historically, landlords would end up on the hook for any utility that was not individually metered but between technology and proper management there are a couple of ways to make sure that as the owner you are not responsible for the tenants’ utilities.

Carefully evaluate how the electric, water and gas are metered on any multifamily property that you are considering. Lawn maintenance is also a factor to be considered. There are ways to have the tenants take care of the lawn but each property must be evaluated individually to find the best solution.

The solution for an over and under duplex vs a side-by-side vs an apartment building will each be different. Also, parking will always be a consideration on a multifamily property. Is there only one driveway? Who gets to use it? Is there street parking available if the driveway is too small? These are factors that must be considered to maximize your tenants’ happiness and your cash flow.

Remember, not every property and not every city and neighborhood will make a good rental. To see if you are close, the monthly rent should be about 1% of the purchase price. If you are close to that number, it’s worth the time to take a closer look at all of the expenses and see what the true projected yield will be.

At the end of the day, I realize investing in real estate remotely makes a lot of people nervous… but teamed up with the right Realtor and property manager, there’s no better way to create long-term wealth and income.

Christian Phillips

Inlet Realty, Owner and Real Estate Broker

P.S. I just put together a video on this particular investment property that goes into a little more detail than what I covered in this article today. Check it out here if you’re interested:

P.P.S. If you have any questions, or if you’re interested in working with me to help you find and manage an investment property, feel free to reach out to me over at Inlet Realty. My team and I help walk our clients through every step of the process: from finding a property… to purchasing it… to renovating it (if needed)… to managing it. All of which can help you invest in property for both long-term wealth building and current passive income.

Source: DividendsAndIncome.com

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.