What happened with AT&T (T)?

Well, the company currently has two large businesses housed under one roof. A telecom business. And a media business.

Media is being spun-off as a new independent business to shareholders next year. So AT&T investors will still basically own the same stuff, but through two separate companies. A separate media company – Discovery – is going to merge with the new media spin-off, but that’s really a small part of this story.

You’ll still have the exciting 5G exposure on one side and the exciting streaming exposure on the other. It’ll just be packaged differently.

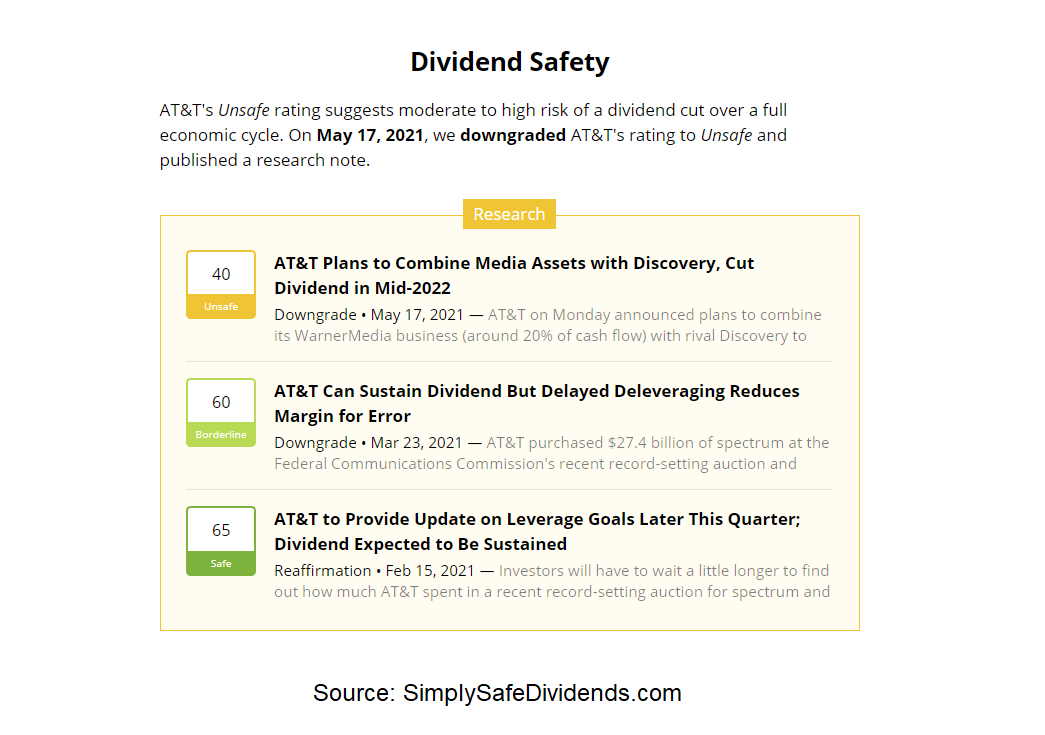

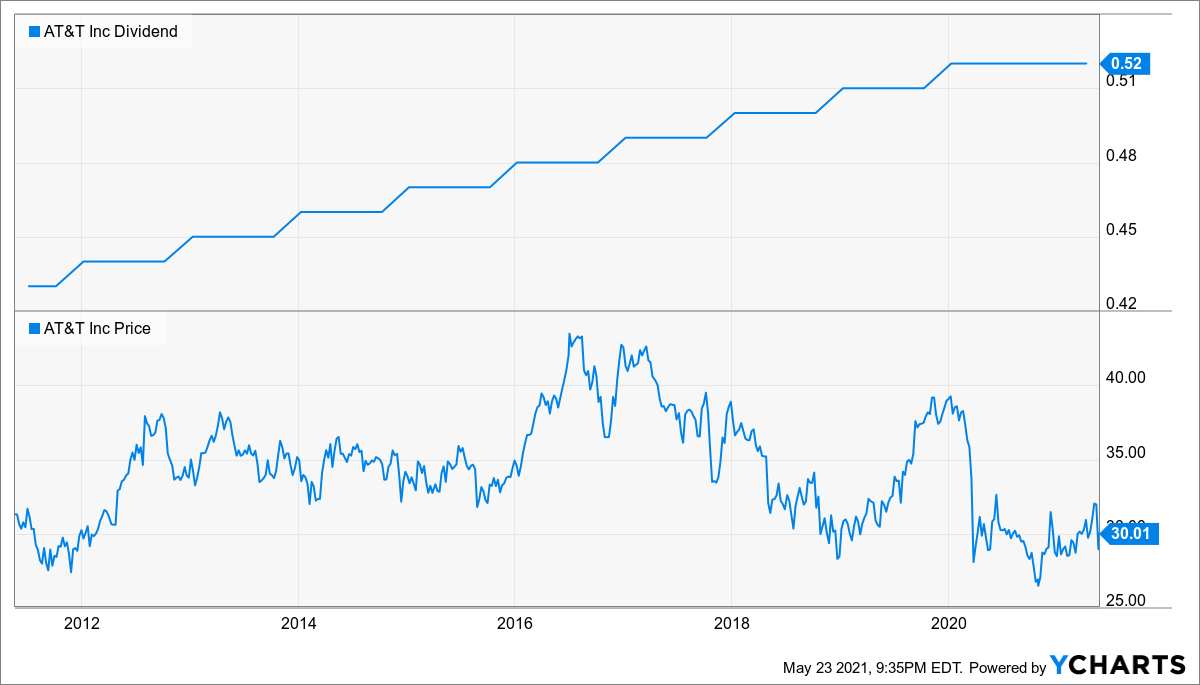

Since the media assets produce a lot of cash flow, the legacy AT&T – the remaining telecom business – will be cutting its dividend after the spin-off completes. We’re talking about a dividend cut of somewhere between 40% and 50%. Ouch.

However, the media business may pay a dividend of its own, greatly reducing the overall income loss. And if the new business doesn’t pay an attractive dividend, investors can simply sell the shares and buy something else that does.

In the end, I don’t think current AT&T shareholders are looking at a massive dividend cut after it’s all said and done. Certainly not the prevailing 50% headline number.

Moreover, both businesses could get valuation bumps, as AT&T has long been in the doldrums in this respect.

When AT&T starts trading as a telecom pure play again, I imagine it’ll be similarly valued to Verizon, with a similar business model, similar yield, similar growth prospects, and a similar balance sheet.

So if you like Verizon stock, I can’t imagine disliking AT&T stock. They’re going to be almost the same thing, and selling AT&T stock now to buy Verizon stock instead basically leaves you with a “dividend cut” and familiar business anyway.

So if you like Verizon stock, I can’t imagine disliking AT&T stock. They’re going to be almost the same thing, and selling AT&T stock now to buy Verizon stock instead basically leaves you with a “dividend cut” and familiar business anyway.

With that in mind, if you own AT&T, the best thing to do here might be to just hold it. After all, there aren’t many stocks out there that can offer that kind of yield as a direct replacement.

And any that do are in a totally different business models, changing your portfolio allocation and still exposing you to a heightened amount of long-term risk.

If you sell AT&T stock and move your money into something lower-yielding, then you’re still locking in a reduction in income. Now, it’s never nice to experience any loss in passive income, so I understand the frustration.

What can we learn from this? Two important lessons come to mind.

Both of which I’ve been consistently repeating over and over again here at the channel. I think this situation is a good opportunity to review both of them. Ready?

Let’s dig in.

Lesson #1: The importance of diversification

Di-ver-si-fi-ca-tion. I can’t repeat it enough. If you’re needlessly concentrating yourself into a couple dozen or so stocks, you’re taking on unnecessary risk and volatility. That is silly.

We put together a video earlier this month discussing why I own over 100 stocks in my own portfolio. Please watch it if you haven’t already.

It’s situations like this that prove out how important that level of diversification is.

I can be sanguine about things when bad news comes along from an investment, because no one company has an overwhelming impact on my wealth or passive income. A lot of investors out there keep fighting on me on this, absolutely determined for some nonsensical reason to concentrate themselves into a handful of stocks, then scream and cry when bad news hits. It’s your money. I’m just trying to help.

I’ve personally heard from retired investors who have 10% or more of their portfolios in AT&T stock alone because of the big dividend that helps them to cover their bills.

I’ve said time and time again how I think it’s so important to avoid that level of concentration. These retirees are now in a tough spot. And I feel for them. I really do. Because now they’re faced with limited options in order to keep their income fully intact without totally revamping their portfolios and/or taking on even more risk.

But if AT&T is, say, 1% of your portfolio, this is a non-news event.

If 30% of your income from something that’s 1% of your portfolio suddenly disappears, it’s kind of a non-issue. We’re talking about maybe half a percentage point of income after factoring in the disproportionate yield. If you’ve built up a broadly diversified portfolio of high-quality dividend growth stocks, the other stocks in your dividend growth stock portfolio should be busy stabilizing things with dividend raises of their own, quickly erasing this income loss and balancing you back out.

I think of my own portfolio as a very large gaggle of golden geese laying ever-more golden eggs.

Because I tend to stick to blue-chip stocks, these golden geese are some of the most healthy geese out there. But even healthy geese can, and sometimes do, get sick. Things happen. That’s life. And because I don’t have a crystal ball, I want to make sure that if one goose stops laying as many eggs as it’s supposed to, the other 100+ geese will stay ever-more productive to keep things humming along just fine until a solution can be worked out.

Because I tend to stick to blue-chip stocks, these golden geese are some of the most healthy geese out there. But even healthy geese can, and sometimes do, get sick. Things happen. That’s life. And because I don’t have a crystal ball, I want to make sure that if one goose stops laying as many eggs as it’s supposed to, the other 100+ geese will stay ever-more productive to keep things humming along just fine until a solution can be worked out.

If you don’t believe me on this, how about believing Warren Buffett?

We put out a video only a week ago talking, once again, about the importance of diversification. Notice a theme yet? This video recounted the valuable lesson on diversification that Warren Buffett put out there at this year’s Berkshire Hathaway meeting.

Want another example of how bad of an idea concentration can be?

How about the sudden loss of billions of dollars? That’s what happened to Bill Hwang over at Archegos Capital after running an extremely concentrated portfolio. Of course, he compounded his problems by using margin on low-quality stocks. Still, concentration can be disastrous.

Lesson #2: Don’t chase yield. Avoid high-yield stocks

I’ve said it before. I’ll say it again. Don’t chase yield. High-yield stocks are usually junk stocks.

How do you know I’ve said that before? Well, because we put out a video only weeks ago where I said exactly that.

I define dangerous high-yield as anything yielding 5 or more times the broader market’s yield.

My advice is to avoid those stocks 100% of the time. This is another thing that a lot of investors out there keep fighting me on, which is to their own detriment. Why do I say to avoid these stocks? Because they tend to be terrible long-term investments. I’d know. I’ve made the mistake of chasing yield before and suffered the consequences. In a video we put earlier this year, I shared my errors with you viewers so that you don’t make the same mistakes.

Now, AT&T has long been right on the edge of that speculative high-yield area.

The stock has typically been just below the area of what I consider dangerous high yield. It’s been on the bubble. And I’ve thought before that it qualified as an acceptable long-term idea for dividend growth investors looking to stretch the limits of income and juice the overall yield of their portfolios, assuming they’re willing to take on the risk. Another dividend growth stock on that bubble, for example, is Enbridge (ENB). While I think these names are acceptable, you really have to be careful and limit your exposure to them. Having 5% or 10% of your portfolio in any one stock is a bad idea. But having that much in something questionable like AT&T is a particularly bad move, in my opinion.

The stock has typically been just below the area of what I consider dangerous high yield. It’s been on the bubble. And I’ve thought before that it qualified as an acceptable long-term idea for dividend growth investors looking to stretch the limits of income and juice the overall yield of their portfolios, assuming they’re willing to take on the risk. Another dividend growth stock on that bubble, for example, is Enbridge (ENB). While I think these names are acceptable, you really have to be careful and limit your exposure to them. Having 5% or 10% of your portfolio in any one stock is a bad idea. But having that much in something questionable like AT&T is a particularly bad move, in my opinion.

Make no mistake. When you start getting up into the 5%, 6%, or 7% yields, you are taking on more risk. And the higher you go, the more risk you’re taking.

High yield is a red flag. Every single time. It doesn’t always blow up in your face. But you shouldn’t be surprised if it does.

High yield is a red flag. Every single time. It doesn’t always blow up in your face. But you shouldn’t be surprised if it does.

And if you’re making both mistakes simultaneously by concentrating yourself into high-yield stocks, you’re asking for trouble.

The situation with AT&T is, in my view, not exactly earth shattering. The company isn’t going bankrupt. The stock isn’t going to $0, nor is the dividend being completely eliminated. The company is simply splitting into two through a spin-off, which is actually quite a common event. It’s the reduction in the overall overall dividend payout that is less common and unfortunate. While being of little consolation to longtime AT&T shareholders today, the stock will, ironically, in many ways, be a lower-risk investment after the spin-off and dividend cut are done. But this situation is an opportunity to learn and grow as an investor, with these two lessons being especially valuable and germane.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: DividendsAndIncome.com

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.