I have found myself really liking PayPal (NASDAQ:PYPL) lately. Somehow this growth titan has quietly accumulated a $284 billion market capitalization. PayPal stock has climbed the market cap ladder seemingly just below most investors’ noses.

While everyone’s attention is on FAANG, high-growth stocks or the latest short-squeeze stock of the day, they should really be paying attention to a sleeping giant like PayPal stock.

Although I have been a long-term bull on this name, it surprises me that so many investors have missed the ride in this one.

PayPal is a well-capitalized and highly profitable firm riding multiple growth trends. As those trends expand, so too do PayPal’s strengths.

Obviously the stock is prone to pullbacks — what stock isn’t? — but those pullbacks are opportunities for long-term investors.

It may have a $284 billion market cap today, and maybe tomorrow it’s $250 billion. Maybe it’s $225 billion. But down the road, this company has all the makings of a future tech titan.

Why We Love PayPal Stock

First and foremost, PayPal has strong growth and it operates in long-term secular trends. Those are the two most important observations for investors. In particular, this is true for growth investors.

However, more conservative investors can also benefit from plucking out names like PayPal. It offers them a safe yet attainable growth stock that doesn’t come with some of the risks of younger companies out there.

Get a look at this. For 2020, analysts expect roughly 19.2% revenue growth. That’s followed by estimates calling for 18.7% growth in 2021 and 19.3% growth in 2022.

Back of the envelope, we’re looking at roughly 20% growth for these three years. When it comes to investing, this is the type of consistency that investors crave. On the earnings front, it’s more of the same. Analysts expect 22.5% growth this year and 19.5% growth next year.

Is PayPal stock cheap? Not really. Shares trade at 51 times forward earnings estimates. But why should a high-quality premium operator trade at a discount?

Gross margins have stabilized near 45%, yet profit margin is near the highest its ever been, around 15.5%. Free cash flow has absolutely exploded over the last few years, too.

And while all of this is great, PayPal’s greatest strength may be its end markets. Digital payments and e-commerce have some of the most consistent and long-term growth that we can ask for. But the company hasn’t stopped there.

Its latest foray into the crypto space now allows customers to purchase Bitcoin (CCC:BTC-USD), Bitcoin Cash, Ethereum (CCC:ETH-USD) and Litecoin (CCC:LTC-USD).

As investor interest in this asset class continues to climb, so will trading volumes. With PayPal being one of the ways to buy and sell these cryptocurrencies, we’re seeing PayPal pull additional growth levers.

A Look at the Assets

Last but not least, we need to talk about PYPL’s assets here because it’s not just the legacy platform we like. Businesses use PayPal for online sales and subscriptions. John uses it to send his kids some money or split the dinner bill with his brother.

But PayPal is more than that. It’s more than crypto, too.

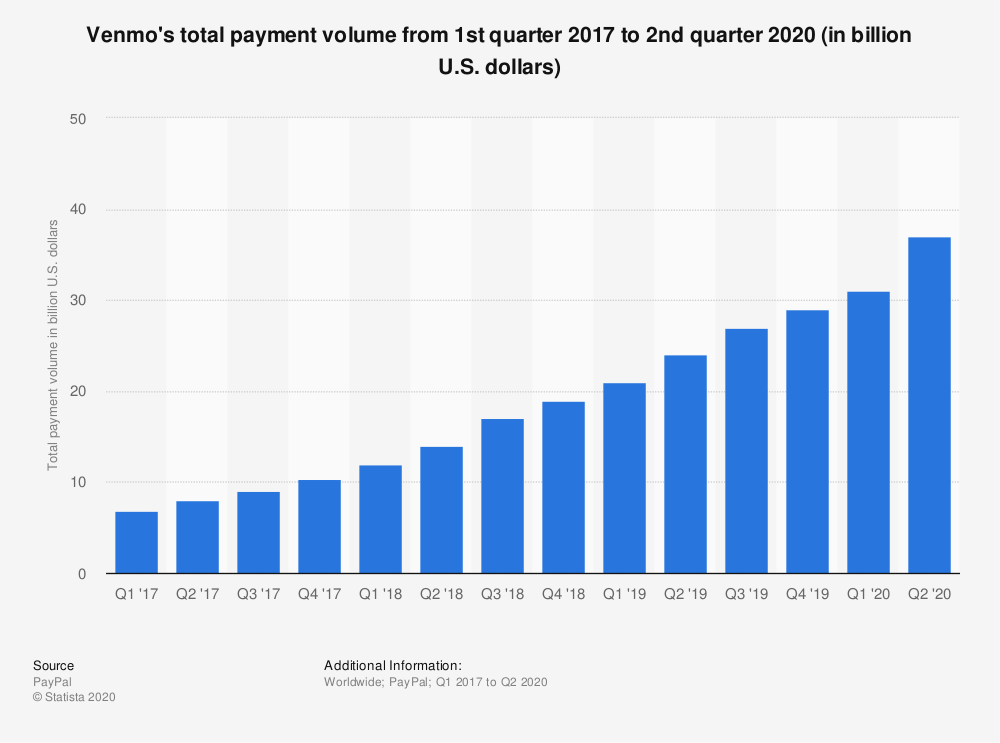

It owns the Venmo property, a multibillion-dollar entity that was scooped up on the cheap, and has transformed it into a money-sharing juggernaut. Well, cheap is relative. PayPal paid $800 million for Braintree, receiving the Venmo property in the deal, but it was a great purchase.

In Q2 2017, Venmo had $8 million in payment volume. In Q2 2020, it had $37 million. While the pandemic raged on, this platform saw Q2 volume grow 37% year-over-year and almost 20% sequentially.

PayPal also plunked down some serious cash on Honey, paying $4 billion for the asset.

While some critique this move, I think it helps build out PayPal’s e-commerce ecosystem. The stickier it becomes — and nothing keeps consumers around more than saving money — the more value it drives for PayPal as a whole.

Some people don’t like to see mergers and acquisitions (M&A) from the stocks they own. Personally, I see it as a way of investment. If management can continue to take the free cash flow its business throws off and invest it into properties, platforms and acquisitions that generate value, then it will only make them stronger down the road.

Some of the greatest stocks on earth have done just that.

Bottom Line on PYPL Stock

On Jan. 25, PayPal stock hit new all-time highs. Since then, it has endured four declines in the past five sessions. Shares are down about 4% as a result.

For a high-quality holding, that’s a decent start to begin accumulating. Bulls have to remember, this is a long-term story, and there will be bumps along the way. But PayPal stock can be a core holding for a wide range of investors.

Continue to buy the dips, and use any deep corrections in 2021 as an opportunity.

— Matt McCall and the InvestorPlace Research Staff

Legendary fund manager Louis Navellier – a man Forbes calls "the king of quants" – is going "ALL-IN" on this game-changing AI technology. He says, "This is the culmination of everything you've been reading about AI for the last 60 years."Get the details...

Source: Investor Place