Stocks are up, the economy is in shambles and lockdowns are making a comeback. But people are also being vaccinated as I write this, just 12 months after we learned that COVID-19 was even a thing.

How do we invest through this transitional market? I’ve got a three-point plan for you that works in any economy—not just the Twilight Zone one we’re living in now.

Step 1: Start With “Tollbooth Stocks” and Build From There

Tollbooth stocks are the kinds of companies we safety-conscious dividend investors love: they hold the infrastructure—think pipelines, warehouses and data networks—big players like, say, Amazon.com (AMZN) must have to operate.

These quiet “toll collectors” hand over most of the cash they collect to us as dividends.

Another benefit of these stocks is that buying them is much safer than trying to pick individual winners in competitive industries.

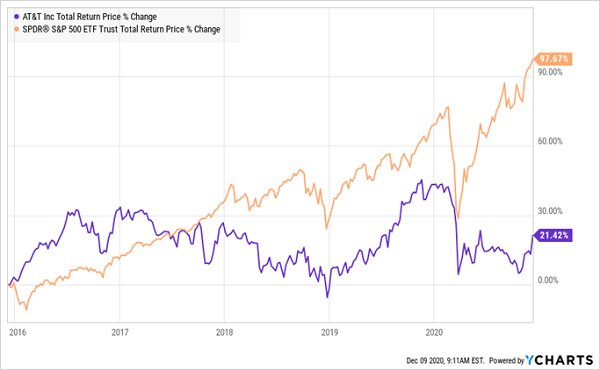

To show you what I mean, let’s say that, five years ago, you wanted to buy into the trend toward surging mobile-device use and data consumption. You could have bought the go-to US telecom stock, AT&T (T), which is renowned for high yields: it paid around 5.5% then.

But that high yield wouldn’t have saved you from a lousy return. In the last five years, AT&T has been run over by the S&P 500—even with dividends included!

Popular Telecom Pick Flops

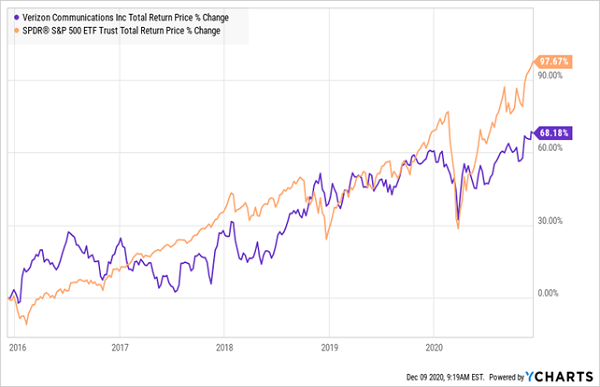

What about Verizon Communications (VZ)? It typically yields a bit less than AT&T. But it did make up for that in price gains over the last five years, crushing Ma Bell’s stock. Even so, it still fell well short of the S&P 500:

Verizon Does a Bit Better, But Still Disappoints

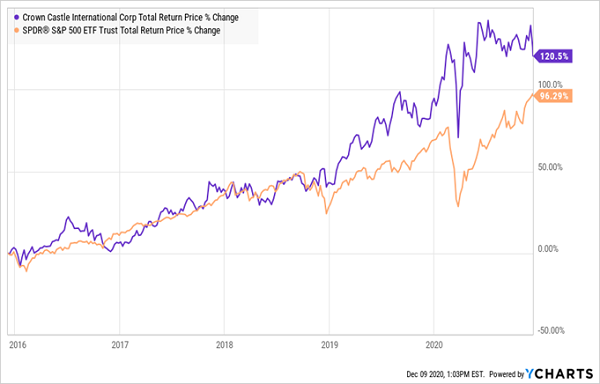

Now let’s compare this duo to our tollbooth play, Crown Castle International (CCI). It’s a real estate investment trust (REIT) with 40,000 cell towers and 70,000 small-cell nodes. The latter are “mini-towers” that boost capacity and service quality in a particular area and are vital to the deployment of next-gen 5G networks. All the major telcos pay “rent” to CCI, including AT&T and Verizon.

The stock roared past both of them—and the market, to boot!

This Tollbooth Play Is Anything But Boring

Crown Castle is just one example of an effective tollbooth play. There are plenty more out there, including pipelines, owners of corporate data centers, and utilities.

Step 2: Add Growth With “Relative Strength”

Tollbooth plays can provide a great base for your portfolio. Now let’s add upside (in both share prices and dividends) with stocks showing what I call “relative strength.”

Relative strength means that strong stocks tend to stay strong, giving them a solid base from which to jump. Forget the bargain bin—we’re not looking for low P/E ratios here—just stocks that have momentum.

Everybody loves betting on a long shot, but the trouble is, these underdogs simply don’t come in enough to pay. We like strong stocks, smart management and megatrends. But everybody wants those, so where do we find our edge?

In two places:

- We find underappreciated and hence undervalued stocks in popular sectors. Think: firms with a technology edge that are not—yet!—priced like go-go tech stocks.

- Or we look at an out-of-favor sector and find a stock that has been mislabeled. REITs are one place to search—many people associate them with (dying) shopping malls, but there are many kinds of REITs, like Crown Castle, for example, or landlords of other specialized properties, like lab owner Alexandria Real Estate Equities (ARE).

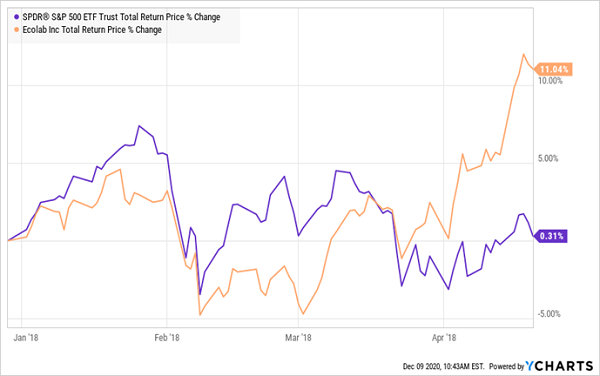

Cleaning-supply company Ecolab (ECL) provides a good example of the kind of fast return a relative-strength stock can deliver.

Pre-COVID, most investors saw it as too boring to bother with. But its stock was getting set to soar in early 2018. Look at the right side of the chart below—you can see the stock (orange line) establishing a base and then springing past the market.

Ecolab Plants Its Flag

With the pattern firmly established, I recommended Ecolab in my Hidden Yields service in April 2018. When we sold in December 2019, we took a 31% return with us, easily besting the S&P 500’s 24% return in that time—all thanks to a “boring” cleaning-supply company!

Now let’s move on to the final key in our dividend-investing plan:

Step 3: Take Out Some Inflation “Insurance”

With the Fed’s money-printing quantitative easing likely to stick with us, it doesn’t hurt to build some inflation protection into our portfolios.

Most investors think gold is the best inflation hedge, but it doesn’t work for us because coins and bars don’t pay dividends! (In fact, you’ll probably have to pay to store them.) Gold miners aren’t exactly dividend machines, either. Major producer Newmont Corp. (NEM) yields just over 1%.

Instead, we’ll look for stocks with:

- Dividends that outrun inflation: To maintain our lead over rising prices, we need stocks with growing—and ideally accelerating—payout growth. Steady dividend growth grows your yield on cost over time. That can mean that a 3% current yield could grow to 10%+ years down the road. (I’ll show you this yield gain in action below.)

- A low beta rating: Beta is a volatility measure. A rating below 1 means a stock is less volatile than the S&P 500; above 1 is more volatile. We want a rating of 1 or below so we can enjoy our dividends in peace.

The utility sector is a good place for us contrarians to hunt for stocks that tick these two boxes. Midwestern utility WEC Energy (WEC), for example, boasts a payout that’s surged 161% in the last decade. As a result, folks who bought back then don’t care a bit about the 2.9% yield the stock offers today—the inflated dividend they’re collecting now amounts to a much bigger percentage of their original purchase price—9.7%, to be exact!

They’ve also seen a nice gain as investors have followed that surging dividend and bought the stock, driving it up 216% in that time.

Finally, the beta rating—WEC’s five-year beta is 0.5, meaning WEC investors have to contend with half the volatility the typical S&P 500 investor does. That means they can enjoy their growing payouts with much less risk of the stock price falling out from under them.

— Brett Owens

REVEALED: How to Make a PREDICTABLE 20% Gain in 2021 (Bull or Bear!) [sponsor]

I hope this 3-step dividend safety plan helps you navigate 2021 with more peace of mind. By following it, you can nicely set yourself up to capture serious upside while protecting your portfolio from a pullback, too.

And these 3 stocks aren’t the only ones you can use this 3-step plan on. In fact, I’ve got 7 MORE picks that are even better buys as the calendar flips to 2021. I call these 7 dividend growers “recession proof” because I’ve handpicked them to hand you predictable returns of 12% to 20% a year in a bull or bear market!

This 7-stock “mini-portfolio” puts the power in your hands. All 7 of these picks are nicely positioned to:

- Predictably double or triple your investment every few years.

- Protect your portfolio from wild swings so you can enjoy a stress-free, secure retirement.

- Let you hold them for years without the “can’t sleep at night” worries you’ve no doubt been living with through 2020.

All 7 of these low-key dividend growers are bargains now, but I don’t expect that to last as more investors clue into the low-volatility dividends and gains on offer here.

Get full details—names, tickers, complete dividend histories, best-buy prices and more—on all 7 of these stout dividend growers now. You have everything to gain and nothing to lose by giving them a look.

Source: Contrarian Outlook