When I ask closed-end fund (CEF) investors what they like most about these funds, their answer is almost always the same: the dividends!

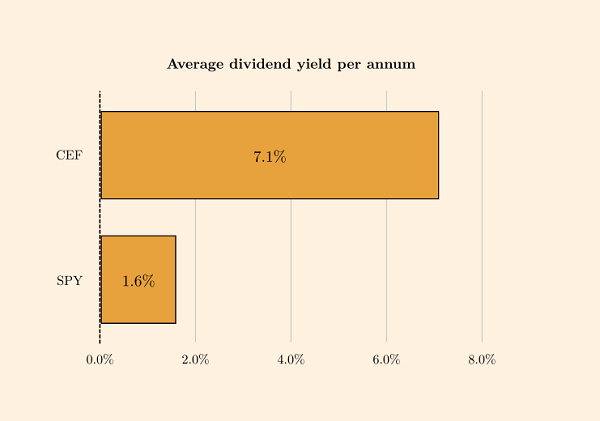

It’s easy to see why. The average CEF yields 7.1%, and that majority of the 500 CEFs in existence pay dividends monthly. Those two strengths put you miles ahead of someone who bought the average S&P 500 stock, with its pathetic 1.6% payout.

CEF Dividends Reign Supreme

Source: CEF Insider

Source: CEF Insider

With a 7.1% dividend, you’d collect just under $50,000 in annual income on a $700,000 investment. Compare that to a popular index fund like the 1.6%-paying SPDR S&P 500 ETF (SPY): you’d need over $3.1 million to collect the same $50,000 of income!

What’s more, if you limit yourself to SPY, as many investors do, you’re getting just the S&P 500, including losers like Carnival Corp. (CCL) and ExxonMobil (XOM).

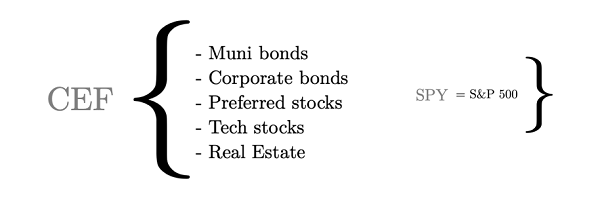

But with CEFs, you can easily create a portfolio of blue-chip stocks, municipal bonds, corporate bonds, preferred shares, tech stocks and real estate investment trusts (REITs). And it’ll pay you that healthy 7%+ dividend, too.

Source: CEF Insider

Source: CEF Insider

How CEFs Build Wealth for Your Children (and Grandchildren)

Aside from high income and easy diversification, CEFs give you something else: the ability to leave a lasting legacy for your kids (and grandkids).

The oldest CEFs have been around for more than a century and have been building serious wealth for families who’ve held on to these funds for generations.

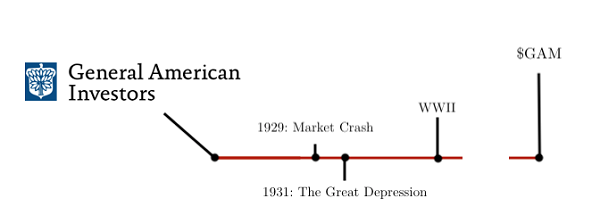

Let’s take the General American Investors Company (GAM) as an example.

The CEF was founded in 1927—just two years ahead of the 1929 crash and the Great Depression.

Today, it holds mostly US stocks, with blue chips like Microsoft Corp. (MSFT), Amazon.com (AMZN), TJX Companies (TJX) and Berkshire Hathaway (BRK.A) among its top-10 holdings.

GAM’s Long History

Source: CEF Insider

Source: CEF Insider

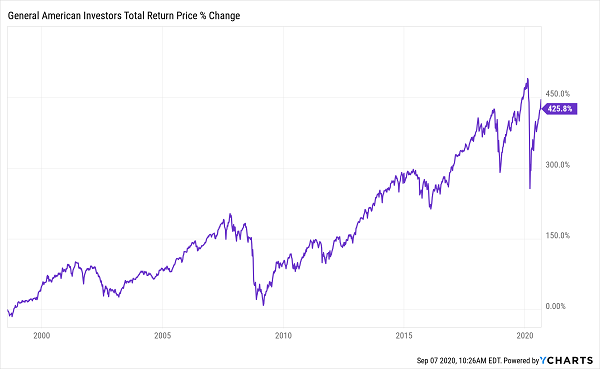

GAM survived 1929 and continued through World War II, the Vietnam War, the Cold War, the 9/11 attacks, the 2008 crash and today’s crisis. If we zoom in on the last couple decades, we see that it’s provided reliable gains and a large income stream, which have combined to deliver a solid total return.

Growing Wealth, Decade by Decade

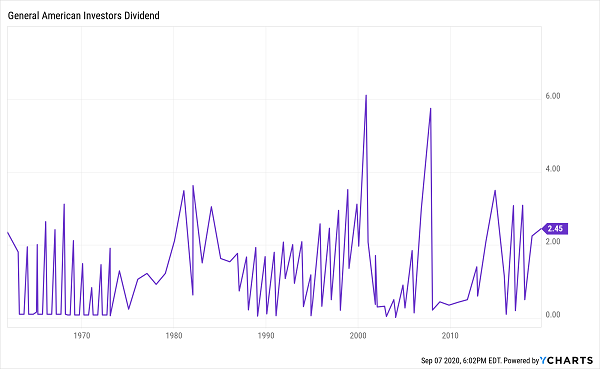

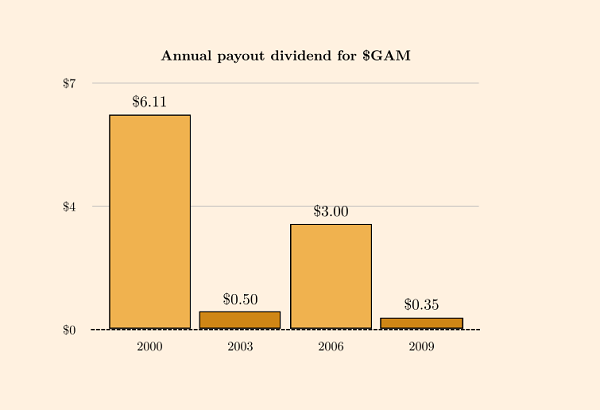

Let’s first talk about GAM’s income potential. This CEF yields 7% on an annualized basis today and has offered a similar yield for decades. Here’s a close look at its history of dividend payouts.

A Well-Managed Income Stream

As you can see, those payouts jump around, but that’s for a good reason: GAM ties its dividend to its portfolio’s performance. Its managers sell stocks and take profits when they see fit, handing those profits to you as dividends.

That also means GAM doesn’t overpay in tough years and pays generously in boom times. This isn’t just a matter of preserving the fund’s portfolio by making sure it doesn’t sell stocks when the market is down. It also means GAM is taking profits when the market is overbought; you can see in the chart above that its biggest payouts were in the bubble years of 2000 and 2006, while later years saw more modest payouts.

Prudent Portfolio (and Dividend) Management

Source: CEF Insider

Source: CEF Insider

This is the key to GAM’s multigenerational approach. It looks to keep its net asset value (NAV, or the per-share value of its portfolio) growing with a focus on the very long term. This has delivered both a secure income stream and growth in the fund’s share price.

Here’s how that’s translated into dollars and cents: an investor who put $500,000 in GAM in 1984 got $50,000 of income to start and a growing income stream that would now come in at $72,814.

Reinvesting Dividends: the Key to Building Long-Term Wealth

But here’s where the really serious gains are. If our investor took the income from GAM and reinvested it into the fund, they’d now be sitting on $6.6 million in GAM stock that would be paying $469,000 of dividends yearly. That’s serious multigenerational wealth!

GAM is the tip of the iceberg, being a CEF focused on stocks. Other CEFs provide steadier and higher payouts for the long haul, even if they’ve been around for less than GAM’s 93 years. Build a portfolio of these, with REITs, bonds and stocks, and you have a diversified collection of funds set to produce wealth for decades to come.

— Michael Foster

4 MORE CEFs That Build Wealth Forever (average yield: 9.4%) [sponsor]

GAM is a great fund. In fact, it fell just short of my list of the top CEFs I’d buy and hold forever. The reason: I’d just like to see a slightly higher current yield, and more predictable payouts, from GAM today.

How much higher would that yield need to be? Well, for us to really maximize our multigenerational strategy, I like to see payouts of 9% or more … which is exactly what you get when you cobble together a “mini-portfolio” of the top 4 CEFs I’m recommending now.

On average, this quartet yields 9.4% today, and these stout CEFs are still absurdly cheap (and have been made even more so, thanks to this latest selloff).

The bottom line is we’re looking at 20%+ price upside, on average, from these 4 funds, thanks to their shrinking discounts alone. And that’s in addition to the near-10% dividend payout you get when you buy in today.

If you want to leave a legacy, simply buy these 4 funds and reinvest your dividends year after year—rinse and repeat. Or you can choose to take your dividend payments out as soon as they roll in and use them however you see fit. It’s your call.

That’s the beauty of CEFs, and my 4 top buys (average yield: 9.4%) are waiting for you now. Click here and I’ll give you the whole profitable backstory on each of these 4 smartly run “legacy” funds: names, tickers, complete dividend histories and everything else you need to know.

Source: Contrarian Outlook