A lot of closed-end fund (CEF) investors—particularly new ones—wonder how CEFs can sustain huge 8% dividends in a 2% (if we’re lucky!) world.

It’s actually pretty easy. Below we’ll look at three ways CEFs make these retirement-changing payouts happen. And, in response to a question I’m hearing a lot from CEF Insider subscribers these days, we’re going to zero in on one particularly sticky subject: return of capital (ROC).

Contrary to what many people think, ROC isn’t a fund simply handing your cash back to you—and charging a fee for doing so. It’s actually a dividend-investor’s dream! Let’s set up our deep dive into ROC with a snapshot of how easy it can be for CEFs to hand us those rich 8%+ dividends.

Source: CEF Insider, Bloomberg

Source: CEF Insider, Bloomberg

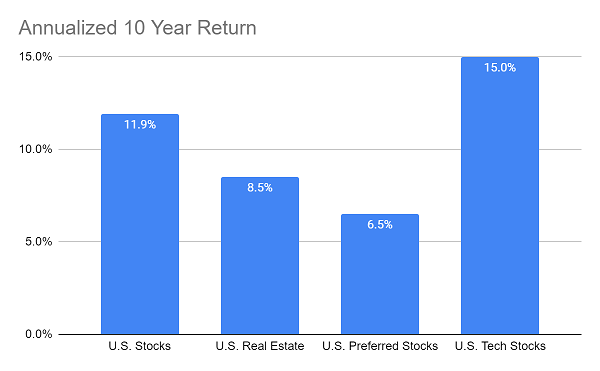

As you can see, a diversified portfolio of US stocks, preferred stocks and real estate would’ve easily returned 8%+ (10.5% on average) in gains and dividends over the past decade.

Add municipal bonds and corporate bonds to the mix, and the return is still 9.4%, well clear of our 8% threshold.

In fact, there are over 100 CEFs tracked by CEF Insider that have returned more than 8% in the past decade (or since inception for younger funds).

Set municipal-bond funds aside (muni funds make up a large part of the CEF universe and tend to have lower returns because of their lower risks and higher tax-free income) and 31% of CEFs have returned more than 8%.

There’s more to the story: let’s take a closer look at how a CEF’s returns land in your account as an outsized dividend payout—it’s crucial to understanding that ROC concept I mentioned a second ago.

A Quick Guide to How CEFs Fund Payouts

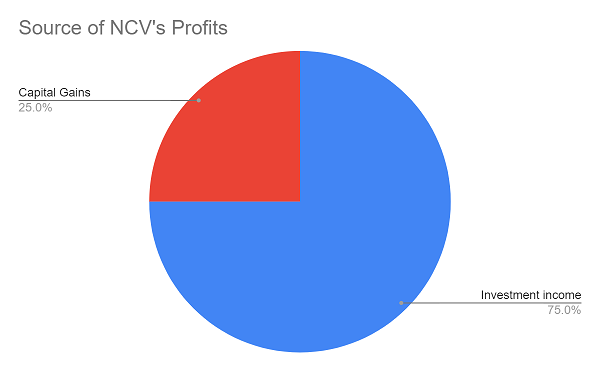

Let’s use a corporate-bond fund, the AllianzGI Convertible & Income Fund (NCV), as our guide. It’s useful because its 11% dividend stream comes from a variety of sources.

Two of those sources are straightforward: the first is investment (or dividend) income on NCV’s portfolio; the fund owns corporate bonds, interest from which accounts for 75% of its dividend income. The second is capital gains; when NCV buys a bond and sells it for a profit, it can then hand us that gain as a dividend.

Source: CEF Insider, AllianzGI

Source: CEF Insider, AllianzGI

This is where ROC (which, in the past, I’ve likened to bad-tasting medicine that’s good for investors) comes in.

To understand ROC, let’s back up and remind ourselves about taxes. Whenever a fund earns a profit, it must pay taxes on that profit. The tax rate for investment income and capital gains differs for the fund, just as it does for you, the investor, on your own portfolio.

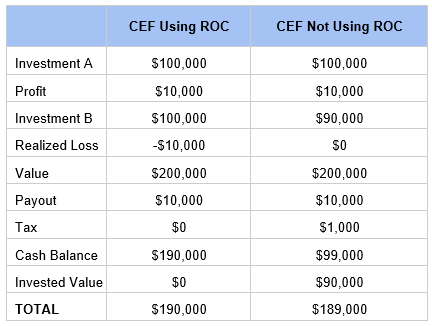

But CEFs can use ROC to minimize, or eliminate, taxes. If, for instance, a CEF makes a $10,000 profit on one investment of $100,000 and has an unrealized loss of $10,000 on another $100,000 investment, it can sell both for a net profit of $0 (in the eyes of the IRS), then hand over that $10,000 to shareholders.

In this scenario, that $10,000 will be classified as ROC, not capital gains, so the fund can reinvest its cash balance into new investments while avoiding taxes. Here’s a quick, back-of-the-napkin scenario showing how this works:

When we compare this to a fund that doesn’t take advantage of the tax code, we see the fund’s value is 1% less than the fund that paid out ROC. This is why ROC is often a good thing.

When we compare this to a fund that doesn’t take advantage of the tax code, we see the fund’s value is 1% less than the fund that paid out ROC. This is why ROC is often a good thing.

Unfortunately, many CEF investors see the “realized loss” line above and wrongly conclude that the CEF employing ROC is doing worse than the one that doesn’t, even though ROC has increased the value of the CEF’s portfolio. In other words, these folks would rather a fund hold on to investments for too long (and pay more in taxes) than be nimble and pivot to where the most money can be made!

— Michael Foster

4 Huge (and Tax-Smart) 9.4% Dividends—With 20%+ Upside [sponsor]

The 4 best CEFs I know have made ROC an art form—deftly cutting their tax bills and freeing up more cash to hand to YOU in the form of rich dividend payouts.

And when I say “rich” I mean it: these 4 funds yield 9.4%, on average! And there’s another secret about the CEF world you should know: CEF investors tend to be very slow to react to events in the market, meaning we still have time to buy these 4 funds cheap!

Each one trades for a massive discount—so much so that my proven CEF-picking model has pegged them for 20%+ price upside in the next 12 months, even if the market only treads water from here.

That’s in addition to the huge 9.4% dividend you’ll pocket from these 4 hidden gems!

These 4 “tax warrior” CEFs are the answer to the crisis we’re living through. Don’t miss out: go here for full details on these 4 stout income plays—and start tapping their incredible 9.4% payouts today!

Source: Contrarian Outlook