McDonald’s (NYSE:MCD) is a very stable quick-service restaurant company with good earnings upside. MCD stock is worth 18-to-20% more than today’s price and has good value and growth characteristics.

For example, its dividend yield of 2.5% is well covered by this year’s expected earnings of $5.76 per share. Moreover, 35 analysts polled by Yahoo! Finance expect McDonald’s to grow earnings by 39% next year to $7.99.

Recently, Seeking Alpha reported that a research firm Longbow Research completed channel checks on McDonald’s store sales.

Apparently sales were flat in the last half of June, but have turned positive for the beginning of July.

This implies that despite Covid-19 restrictions and people’s willingness to venture outside, McDonald’s is still one of the stores they will visit.

McDonald’s Makes Plenty of Cash Flow For Its Dividends

McDonald’s generated $1.064 billion in free cash flow last quarter, after all quarterly costs and capital expenditures.

Therefore, FCF was still high enough to pay for its quarterly dividend that costs $905 million.

Moreover, the company decided to continue its ongoing stock repurchase program. That cost another $902.6 million. Granted, this was down from the $1.44 billion it spent on buybacks in Q4.

But this is another powerful way that McDonald’s has shown it will return capital to its shareholders.

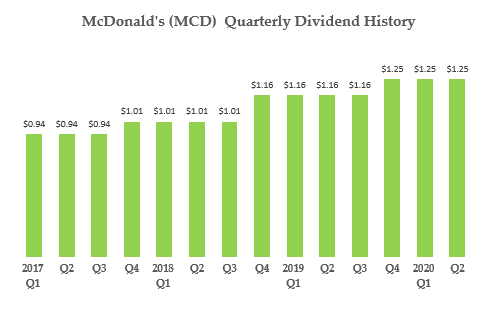

For example, by reducing the share count outstanding it can continue to increase its dividends per share. You can see this in the chart below.

Source: Mark R. Hake, CFA

Source: Mark R. Hake, CFA

This shows that after every four quarters the company tends to increase the dividend per share. The growth in the dividend per share would not be possible if it were to stop its share buybacks.

The upcoming dividend will be the fourth at the $1.25 quarterly level. McDonald’s makes a big point on its corporate site that it “has raised its dividend each and every year since paying its first dividend in 1976.” Therefore, I would expect it will do so again in the fall.

Last year it raised the dividend 8%. If it did so again, the new dividend would be $1.35 per quarter, or $5.40 annually. At today’s price, that gives MCD stock a prospective yield of 2.82%.

What MCD Stock Is Worth

I used three methods of valuing MCD stock. For example, its historical yield is 2.56% over the past four years, according to Seeking Alpha. That implies MCD stock is worth 10% more using the new prospective dividend of $5.40 per share. This is calculated by taking dividing $5.40 by 2.56% to result in a target price of $210.94, or 10.1% above today’s price.

A similar method is used to find its historical price-earnings based valuation. For example, over the past five years, McDonald’s average trailing P/E ratio has been 26.8 times. Therefore, using the 2021 estimates above of $7.99 given by Yahoo! Finance for its 2021 earnings, we derive a target price of $214.17. That represents an upside of 11.8% from today’s price.

Lastly, the average comp price-to-earnings valuation for eight of its publicly traded quick-service peers is 31.7 times earnings. This multiple, applied to 2021 estimate yields a target price of $252.88, or 32% above today’s price.

Source: Mark R. Hake, CFA

Source: Mark R. Hake, CFA

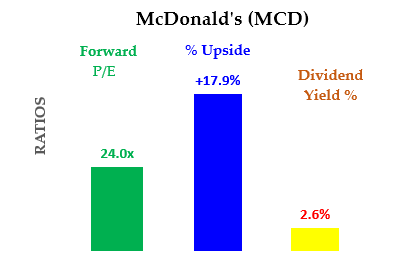

The average valuation for all three of these prices for McDonald’s is $226 per share. That represents a potential upside for the stock of 18%. If its earnings come in higher for this year or next that target price will be higher and vice versa.

What to Do With MCD Stock

Barron’s reported last month that three Wall Street firms raised their price targets for McDonald’s. This was despite the company reporting that sales for May were down 5.1% in the U.S. on a same-store basis.

But that was an improvement over April’s 19.2% decline. So far it has updated its sales data for June. But June is likely to be better. Many states eased up on QSR food location restrictions.

Investors should take comfort in the fact that its dividend is stable, and earnings and cash flow cover it. Moreover, McDonald’s continues to buy back shares, which will allow the dividend to grow. Lastly, MCD is statistically undervalued.

It is trading for a cheap 24 times earnings, a 2.6% dividend yield, and an attractive upside of at least 18%. This is the kind of stock that attracts value investors over the long run.

— Mark R. Hake

Legendary fund manager Louis Navellier – a man Forbes calls "the king of quants" – is going "ALL-IN" on this game-changing AI technology. He says, "This is the culmination of everything you've been reading about AI for the last 60 years."Get the details...

Source: Investor Place