“It’s my money, and I want it now!”

That’s the rallying cry of everyday folks in commercials for J.G. Wentworth, a financial services firm that offers lump-sum cash payments for structured settlements, annuities, lottery payments and more. (If you’ve never seen one of these TV spots, I suggest you try one out. They’re so bad they’re good.)

Every income investor could (and probably should) take a cue from its motto. To quote another spot: “Show us the money!”

Monthly dividend stocks, of course, pay more often than any other income investment.

Dividend checks coming in every 30 days are especially handy for retirees who have bills to pay.

Mortgage payments (maybe), cell phones (obviously), along with electricity, heat and cooling and even Netflix (NFLX).

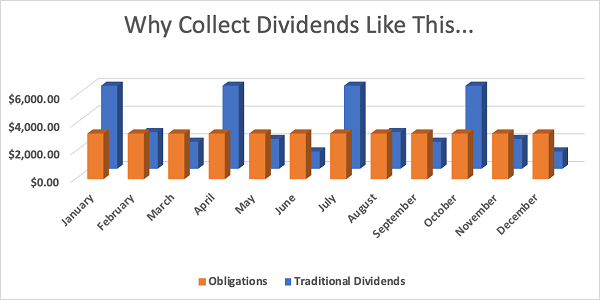

Most stocks and funds, however, only pay quarterly. That leads to “lumpy” income that doesn’t align with reality. Some months you’re ahead of the game, others you’re not:

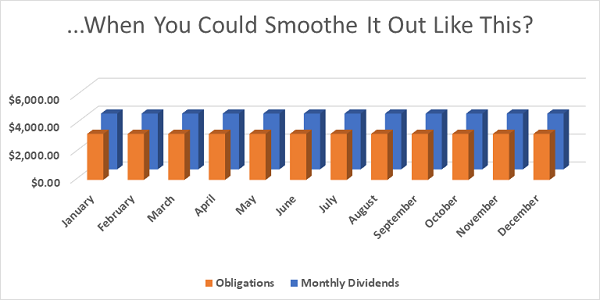

But monthly dividends are easy. Every month is the same total payment:

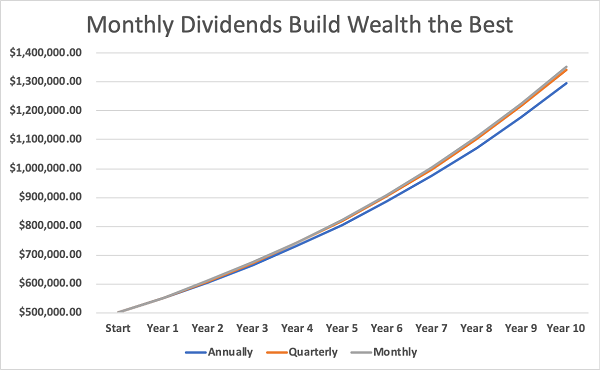

Plus, monthly dividends compound faster. If you get paid, say, $12 per share per year, you have to wait until that annual payment to put that $12 to work. With quarterly dividends, you can put part of that $12 ($3) to work after a quarter, and another part the next quarter, and so on. With monthly payers, you can put $1 to work every single month.

For those of us who reinvest our payouts, receiving them faster helps us buy more and more shares. More shares deliver more dividends. It’s a subtle point, but these days we’ll take every extra dividend dime we can earn!

Of course, this goes out the window if the monthly payers we buy are duds. And because of the nature of companies that deliver monthly dividends—many tend to be real estate investment trusts (REITs), business development companies (BDCs), master limited partnerships (MLPs) and closed-end funds (CEFs), all of which have experienced deep pockets of pain—there are plenty of duds out there.

But there are good monthlies, too. Let’s walk through a few examples to see the difference.

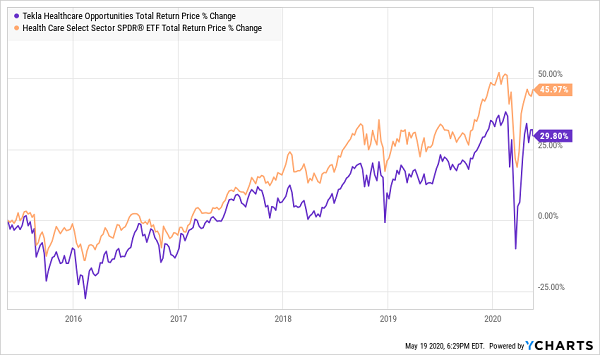

Tekla Healthcare Opportunities Fund (THQ)

Distribution Rate: 7.5%

YTD Return: -3.6%

Many healthcare stocks were actually cheaper than the broader market heading into 2020, due to worries that election-year politics might threaten profits. Now, a pandemic has reminded investors that healthcare firms are always needed.

Tekla Healthcare Opportunities Fund (THQ) is an actively managed CEF portfolio of roughly 50 stocks that’s similar to broad healthcare sector exchange-traded funds (ETFs) such as the Health Care Select Sector SPDR Fund (XLV). In fact, the two funds share seven of the same top 10 holdings, including Johnson & Johnson (JNJ), UnitedHealth Group (UNH) and CVS Health (CVS).

Both funds have a tilt toward larger companies, and both offer exposure to an array of healthcare industries: pharmaceuticals, biotechnology, health insurers, healthcare equipment and more.

But Tekla Healthcare Opportunities has a few important differences. For one, only three-quarters of the fund is invested in equities; it also has a 16% holding in convertible and non-convertible debt, and small amounts of convertible preferreds and warrants, as well as short-term investments. Additionally, THQ can invest up to 10% of assets in venture or restricted securities—exposure you’re simply going to struggle finding in other funds.

Tack on a monthly 11.25-cent-per-share dividend paid out since its 2014 IPO, as well as the fact that, as a closed-end fund, THQ can and does use leverage (about 21%) to gin up returns, and you have quite a different product than your average healthcare ETF.

Unfortunately, Boring Has Been Better

The high, consistent dividend is great, and THQ has outperformed the market by about 6 percentage points year-to-date. But XLV has done better, in 2020 and over the long haul.

Tekla Healthcare offers a 7%-plus yield delivered monthly, as well as diversified exposure to one of the market’s better sectors. But, in recent years, investors have been better off with a “lame” ETF. So lame.

NexPoint Strategic Opportunities Fund (NHF)

Distribution Rate: 13.4%

YTD Return: -49.5%

Mammoth dips like what we saw in February and March can be a deep-value investor’s dream. Especially when they result in juicy yields over 13%.

But despite a rebound from its mid-March lows, NexPoint Strategic Opportunities Fund (NHF) remains off nearly 50% year-to-date, and it’s looking weak again of late. A look under the hood doesn’t inspire confidence, either.

Accessibility can be an issue with some CEF providers, and that’s certainly the case with NexPoint’s bare-bones site, which offers scant info on NHF. A look at the annual report, while dated, does provide some clarity, though. Sixty percent of the fund is invested in the real estate sector, which has been banged up hard. So have financial stocks (21%) and energy companies (5%). NHF also has 21% of assets in agency and collateralized mortgage obligations, and another 9% or so in communications stocks. (Thanks to leverage, its holdings add up to well more than 100%).

The trouble continues when you look at individual holdings, which include NexPoint Real Estate Opportunities (24%), and NexPoint Real Estate Capital (3.5%). Those are private REIT subsidiaries, making it all the more difficult to understand what you’re investing in.

The trouble isn’t worth it. In addition to the massive losses, NHF’s 13.4% yield reflects a recent halving of its monthly dividend, from 20 cents per share to a dime. I wouldn’t depend on this black box to pay a monthly bill!

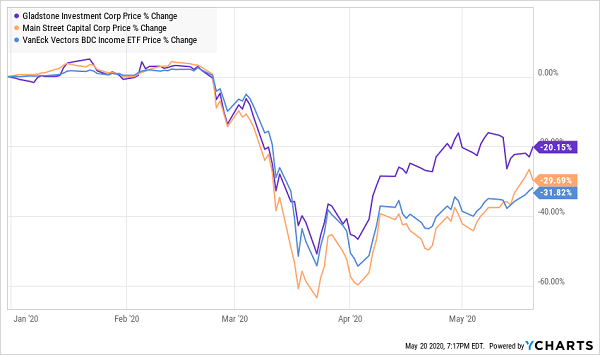

Gladstone Investment (GAIN)

Dividend Yield: 7.9%

YTD Return: -19.9%

Gladstone Investment (GAIN) is a business development company, which means that it’s invested in small firms, and that’s a tough way to make money right now.

To its credit though, Gladstone is holding up better than most BDCs. At 20% losses year-to-date, it’s almost 10 percentage points better than Main Street Capital (MAIN)—one of the space’s few high-quality names—and 11 points ahead of the broader VanEck Vectors BDC Income ETF (BIZD).

When You’re Ahead of MAIN, You’re Doing Something Right

Gladstone, which has a conservative dividend approach that combines regular monthly payouts as well as supplemental distributions as performance allows, not only recently declared monthly dividends on par with its previous rate, at 7 cents per share, but announced a 9-cent supplemental to be paid out in June.

However, there’s a time and place to invest in these private equity-esque firms, and I’m hesitant to say that time is now. Small businesses face an unprecedented struggle not just to grow, but to even survive. Gladstone could very well come out of this with its dividends fully intact, but significant gains could be difficult to come by for some time.

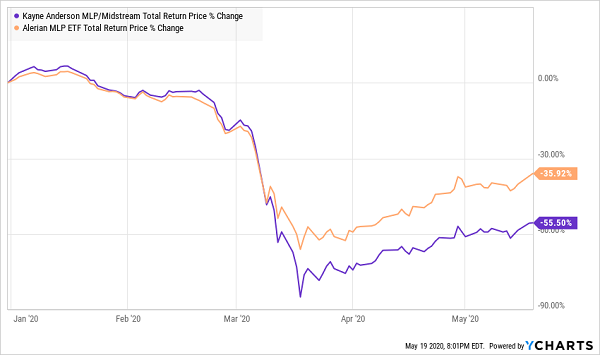

Kayne Anderson MLP/Midstream Investment Company (KYN)

Distribution Rate: 24.4%

YTD Return: -58.1%

The energy sector is loaded with depressed valuations and sky-high yields. But rather than try to pluck energy producers off the scrap heap, I’m more interested in the “toll bridges”: master limited partnerships (MLPs).

Energy MLPs, which typically are involved in the transportation and/or storage of crude oil, natural gas and other commodities and refined products, boast a couple of natural advantages. For one, their cash flows aren’t as sensitive to the downdraft in energy prices, and they also tend to pay out more income on average.

I don’t often discuss MLPs because they’re a headache come tax time, issuing a K-1 tax package that no one should have to deal with. But the Kayne Anderson MLP/Midstream Investment Company (KYN), another closed-end fund, helps you skip that with a simple 1099.

KYN invests in a handful of MLPs, including MPLX LP (MPLX), Enterprise Products Partners LP (EPD) and Energy Transfer LP (ET). And thanks to both beating in the space as well as sky-high leverage of more than 50%, the fund is able to offer distributions north of 24%.

But Leverage Also Has Its Drawbacks

Of course, that same leverage has put KYN into a deep hole this year.

Kayne Anderson can reward traders, but we typically have a narrow window to hit on the purchase. At one point, Kayne Anderson’s fund was trading at just 62 cents on the dollar, but that discount to NAV has since dried up to 14.5%.

That’s still a bargain compared to its five-year average discount of just 2%. However, there’s much more downside risk now thanks to KYN’s heavily leveraged nature, not to mention we’re not out of the danger zone as far as potential MLP distribution cuts are concerned.

— Brett Owens

How to Lock In $4,000 Each Month in Safe, Steady Dividends [sponsor]

Most investments feel like a choice between the lesser of two potential evils right now.

You can grab once-in-a-lifetime yields in KYN, but you run the risk of energy weakness eating away at those yields and sending the highly leveraged fund to exaggerated losses.

On the other end of the spectrum, you could pile into crowded, low-yield blue chips and haul in a “safe” 2% or 3% with backside protection but little upside potential.

So, what’s it going to be: A+ yields built with popsicle sticks and rubber cement, or A+ dividend security but with yields that aren’t enough to live on?

No retirement saver should have to make that choice … and thanks to my “Monthly Dividend Superstars,” you don’t have to.

This lightning-fast bear market has unlocked a few opportunities that I simply didn’t think we’d ever get to jump on again: a group of monthly-paying dividend dynamos that deliver roughly four times the market’s average yield at their currently discounted prices.

High dividends at low prices? That’s an income investor’s favorite one-two punch!

And because investors have been so preoccupied with building a mini-bubble in mega-cap stocks, they’ve ignored these screaming bargains, giving you just a little longer to secure these low prices and high yields.

These contrarian plays tick off every checkbox in the retirement wish list, including …

- High annual yields of 10%. That translates into $4,000+ in monthly income … on a nest egg of just $500,000. It’s all gravy from there if you’ve saved up even more.

- Real upside potential of about 10% annually. That will keep your nest egg growing in retirement, protecting it against any sudden financial “shocks.”

- Hidden value. There’s such a thing as “too popular.” If too many investors crowd into a stock, it becomes grossly overpriced, making more upside difficult to come by and increasing the risk of hyper-aggressive selling if investors get nervous. My “Dividend Superstars” are too small to be flush with institutional money, and far off the radar of many analysts, creating price inefficiencies that you and I can exploit.

This is the path less traveled.

Most finance-TV pundits will tell you to sink your hard-earned retirement money into “can’t-miss” blue chips like the Dividend Aristocrats. They’ve grown their dividends for decades, and probably will for decades more.

Ignore that nonsense. Those same Dividend Aristocrats only yield a little more than 2% on average, and the most established Aristocrats have slowed their dividend growth to a sloth’s pace. Worse, some of these “Aristocrats” might be kicked out of the club by this time next year, their artificially propped-up payouts exposed by a lethal dose of reality.

Don’t take that gamble. Click here and I’ll show you my set-it-and-forget-it “Monthly Dividend Superstars” portfolio paying an incredible 10% on average.

Source: Contrarian Outlook