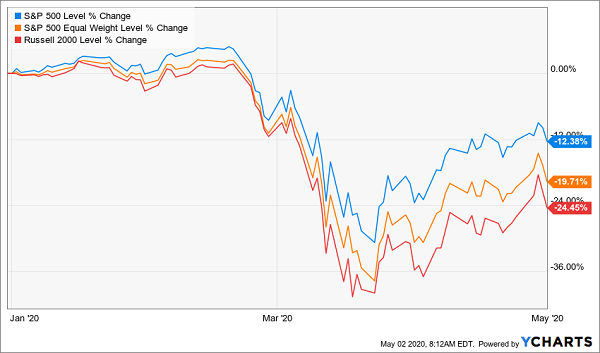

The S&P 500 index has been “relief rallying” like crazy, but to most income investors, this means nothing. The wider the basket of stocks, the rougher the year it has been. Let’s consider that (as I’m writing this):

- Year to date, the “big cap focused” S&P 500 is down “just” 12%. However,

- When we weight its 500 stocks equally, its return drops to 20% YTD. And,

- When we expand the universe to look at small cap stocks, we see the Russell 2000 is down a brutal 24% thus far in 2020:

Don’t Let the S&P 500 Fool You

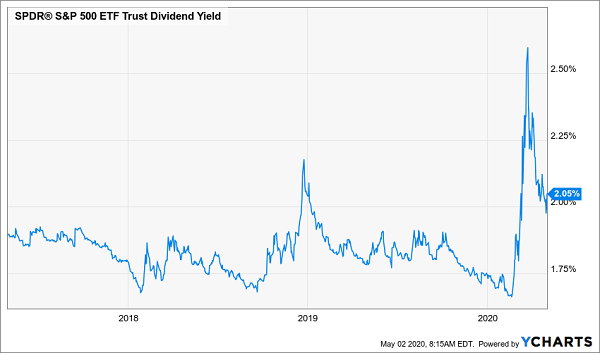

Plus, we now face another problem: an income drought! Ten-year Treasuries yield practically nothing—0.6%—and, after cruising near 3% in March, the S&P 500’s average yield has slipped back to just over 2%, near where it was last spring.

Yield Opportunity Appears—Then Vanishes

As yields grind lower, we find ourselves asking the same question we did in January: where the heck will we find the high dividends we need to retire?

Today I’m going to show you exactly where, with two cheap closed-end funds (CEFs) yielding just a hair under 9.2%, on average.

Drop $250K into these funds and you’ll kick-start a $23,000 income stream (and one of these funds even pays monthly, so your first payout could arrive in just a few days!).

I’ll also reveal two dividend-growth stocks that should be on your list now.

Not only are these companies dodging the wave of dividend cuts we’ve seen, they’re sticking by their payouts, and will likely keep driving them higher. That continued payout growth quickly builds the yield on a buy made today, and drives stock prices up, too, as we’ll see in a second.

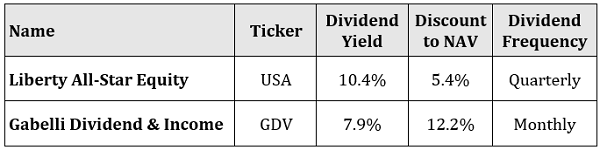

First, let’s dive into those 9.2%-paying CEF picks.

CEFs: 2 Picks for 9.2% Payouts (and Upside)

CEFs are a good choice in today’s volatile market, for two reasons:

- They pay big dividends: Many CEFs yield 7% or more, and some even higher. And when you get more of your return in cash, you naturally cut your portfolio’s volatility while boosting your income stream.

- They’re cheap: About 80% of the 500 CEFs out there trade at a discount to net asset value (NAV, or what their portfolios are actually worth). That gives us a shot at serious outperformance if the market lurches higher from here, and some downside protection of it falls back toward its March 23 low.

With that, here are the two high-yielding CEFs I want to show you today:

Our first pick, the Liberty All-Star Equity Fund (USA), will be familiar to subscribers to our CEF Insider service. It leans toward tech stocks, with Alphabet (GOOGL), Microsoft (MSFT) and Amazon.com (AMZN) among its holdings, alongside healthcare names like Abbott Laboratories (ABT) and Amgen (AMGN).

Combined, tech and healthcare comprise 41% of USA’s portfolio. And I probably don’t have to tell you that both sectors have held up well in this crisis, going by the benchmark Technology Select Sector SPDR ETF (XLK), in red below, and the Healthcare Select Sector SPDR ETF (XLV), in orange.

USA Lets Us Buy Outperformers Cheap

But thanks to USA’s discount, we can “rewind the clock” on tech and healthcare, picking up the fund’s holdings for 5.4% below today’s price, or roughly where these sectors were in mid-April. Add USA’s 14% holding in financials (oversold, in my view), and you get a nice catalyst for more upside while pocketing the 10.4% payout you’d lock in on a buy today.

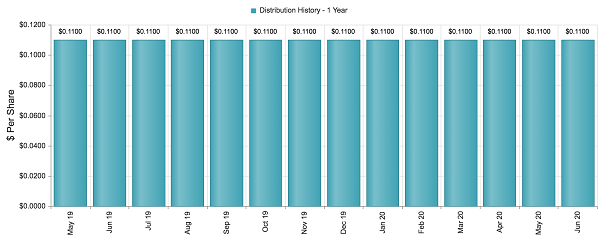

Speaking of oversold, let’s intro our second CEF, the Gabelli Dividend & Income Fund (GDV), run by the famed Mario Gabelli, who follows a similar value-investing strategy as Warren Buffett. As you can see in the table above, Gabelli’s fund pays dividends monthly, and has made a statement by going ahead and declaring its $0.11-a-share payout through June.

GDV Rides Its Monthly Payout Through the Crisis

Source: CEF Connect

The fund pairs up nicely with USA—while both have a strong position in undervalued financials (19% of the portfolio in GDV’s case), Gabelli’s fund also has significant holdings in industrials (15% of the portfolio) through stocks like Honeywell International (HON), whose products and services make its clients more efficient, something that will be in high demand in the recovery. (Honeywell’s dividend is also well protected, at just 40% of free cash flow.) Meantime, recession-resistant holdings like food maker Mondelez International (MDLZ) add ballast.

The biggest reason to consider GDV is its wide 12% discount to NAV. Consider that the fund has traded at just a 5% discount in the past year, so we’re looking at plenty of upside as this gap vanishes.

Next, Move on to Dividend Growth (2 Picks)

Now let’s flip over to another sector that’s essential now, and will only see bigger gains in the recovery as the work-from-home trend sticks.

That would be communications—but we’re not going to go with the two names everyone thinks of here: Verizon (VZ) and AT&T (T). That’s because both are meager dividend growers, with Verizon only hiking its payout by a penny last year. AT&T? It never hikes by more than a cent, and with $164 billion of long-term debt on its balance sheet, that won’t change anytime soon.

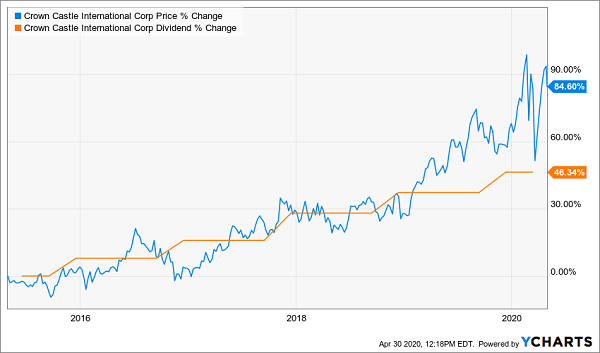

So we’ll go with Crown Castle International (CCI), owner of 40,000 cell towers across America, instead. Look at the chart below—you can clearly see the stock price bouncing higher with each dividend hike:

Where the Dividend Goes …

Now, it is true that the price has gotten ahead of Crown Castle’s dividend growth, but this stout company has what it takes to keep driving its payouts—and share price—higher. Last week, it announced an outsized 8% year-over-year jump in funds from operations (FFO, the best metric for a REIT like CCI) in the first quarter, even as the coronavirus tightened its grip on the economy.

That’s the kind of growth any other company would kill for right now!

CCI also stood by its 2020 guidance, the midpoint of which is $6.12 in per-share FFO, up nearly 8% from 2019. The payout accounts for 78% of the 2020 figure, very conservative for a REIT.

The stock yields 3%, but you’ll quickly build on your yield on a buy made today, thanks to management’s pledge to hike the dividend 7% to 8% a year—a pledge that remains intact.

UNP: A Lockdown Lifesaver

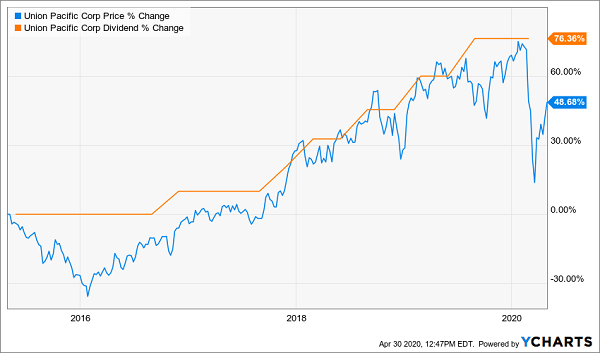

Finally, let’s branch out into transportation with Union Pacific (UNP). The railway is helping America survive the lockdown, hauling everything we need—from produce to frozen pizzas—to keep our homes stocked.

Union Pacific expects the coronavirus to shave its volumes by 25% in the second quarter, but it entered the pandemic in a strong position. For one, it’s paying a lot less for diesel fuel (down 10% in Q1). Plus, it ended the quarter with a combined ratio of 59%—an all-time record. (Combined ratio is a measure of railway efficiency; the lower, the better.)

Meantime, Union Pacific regularly hikes its dividend more than once a year, and has boosted its payout 76% in the last five years. As you can see, the share price has risen in lockstep with the payout—and is steadily closing that gap in the rebound:

Union Pacific’s Dividend Dictates Its Share Price

Finally, UNP’s dividend looks safe, at just 49% of free cash flow, and its balance sheet is strong, so management has lots of room to keep the payout growing, despite the crisis.

— Brett Owens

4 Perfect “Crisis Buys” for Huge 15%+ Dividends (and upside) [sponsor]

I know this crisis has been tough, especially if you’re a retiree who’s been sideswiped by the raft of dividend cuts we’ve seen.

But you DON’T have to sit there paralyzed. By taking a few decisive actions now, you can start pocketing annual yields as high as 15%! Plus you’ll set yourself up for massive capital gains once the rest of the herd comes back to their senses.

We’ll do it by purchasing 4 contrarian income investments throwing off life-changing dividends up to 15%! These bargain buys pay a solid 11.9% payout, on average—so a $100K investment kick-starts an $11,900 annual cash stream—and ALL of these 4 new picks pay dividends monthly!

In other words, a little more than 8 years in, you’ll have recouped your entire upfront investment in dividend cash alone! That’s the very definition of safety, and I can’t wait to show you these 4 cash-rich income plays.

Source: Contrarian Outlook