During volatile times like these, the best thing to do is this: stay calm and keep collecting your dividends.

Fighting the urge to sell is critical, because doing so could slash your dividend income by 82% or more.

Here’s where I’m getting that number: let’s say you hold the stocks in our Contrarian Income Report portfolio, which yields an average of 7.2% as I write this.

(If you bought a while back, you’re likely yielding more on your investment, thanks to our picks’ dividend growth, but let’s use 7.2% as our benchmark here.)

And let’s say you’ve got a reasonable nest egg—about $350K—invested. Your 7.2% yield translates into an income stream of $25,200 a year.

I think you’ll agree that dividend payouts of that size are a big part of the retirement puzzle—and they’d stop cold the moment you sell.

What would you buy instead? Treasuries? At today’s 1.3% yield, the 10-year would pay you $4,550 a year on your $350K—or 82% less than our CIR picks! That’s no way to fund a retirement.

Here’s an even better reason to hang on to your high yielders: these stocks tend to hold up quite well in a downturn like the one we’re living through now.

Our 3-Point “Pullback-Proof” Checklist

What are the hallmarks of a resilient high-yield dividend play? Here are three telltale signs I always look for:

- A history of holding firm in past downturns. It’s obvious: if a stock held its own in the last pullback, odds are it will outperform in the current one.

- A high—and rising—dividend. Big payouts tend to get investors’ attention in times like these, when the first-level crowd is going all in on pathetic payers like Treasuries. A growing 7%+ payout looks great compared to the 1.3% the 10-year is currently dribbling out.

- A low “beta”: Beta ratings sound like a shadowy technical indicator with no value to us conservative dividend investors, but that’s false.Beta—measured over five years on most stock screeners—is an important volatility measure. Its simple: a beta of 1 means a stock tends to move in tandem with the S&P 500. Below 1: less volatile. Above 1: more volatile. For pullback-resistant buys, I look for a beta of 0.5 or less.

To see this 3-point strategy in action, let’s look at Omega Healthcare Investors (OHI), which I’ve recommended in Contrarian Income Report. OHI is a real estate investment trust (REIT) with investments in 950 senior-care facilities, almost all of which are in the US.

OHI Is a Rock in a Downturn

Let’s start with point No. 1, strong performance in the last downturn.

Check! In the late 2018 wipeout, which ran from September 20 of that year to Christmas Eve, OHI investors made money—and no small amount, either: we bagged a 4.9% total return in that three-month period, while the broader market returned negative 19%.

OHI Profited in the 2018 Crash

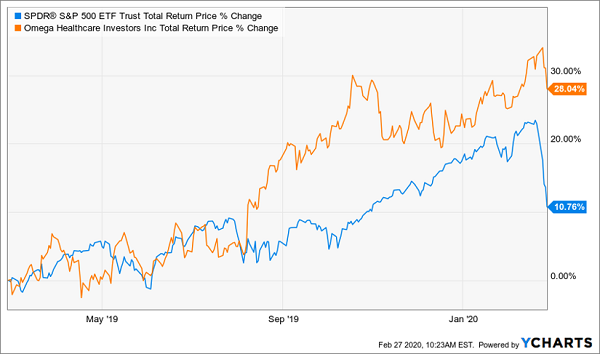

So it probably comes as no surprise that OHI is holding up nicely again in 2020. Even though the market had tanked 10% from February 19 to last Thursday morning, OHI was paddling along nicely, its share price off only about 1.7%, while its shareholders continued to benefit from its 6.2% dividend.

And on the year, it was still well into positive territory, particularly when you look at its total return (including dividends) while the S&P 500 was deep in the red:

OHI Holds Firm in a Rough Start to 2020 …

Go back a year and the difference is even more stark:

And Crushes the S&P 500 in the (Somewhat) Longer Term

Big—and Growing—Dividend Draws a Crowd

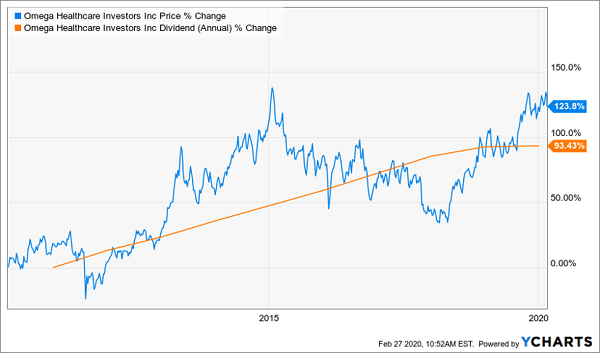

Bear in mind that these steady performances come from a stock paying “just” a 6.2% dividend today, well below our CIR portfolio average of 7.2%. But the key takeaway here is that OHI’s dividend has grown, and as I’ve written before, a rising payout acts like a magnet, pulling a company’s stock up with it. You can see that tight correlation in the following chart:

Dividend Growth = Share-Price Growth

The Final Ingredient? A Low—and Falling—Beta

Finally, OHI ticks the last of our three boxes: a low beta, at just 0.39, meaning the stock is less than half as volatile as the S&P 500. And perhaps the most interesting thing about OHI’s beta happens when you overlay it with the chart above:

OHI’s Rising Dividend Adds to Its Stability

This is one of the best testaments to the ability of a high (and rising) payout to stabilize your portfolio that I’ve ever seen! As you can see, as the payout (in orange) grew over the last decade, it pulled up the share price (in blue) and made the stock steadier: OHI’s beta rating fell by 62%.

Put it all together, and you can see that OHI has been the definition of a pullback-resistant dividend—in the long haul and the short.

— Brett Owens

These 5 “Pullback-Proof” Dividends Pay Up to 9.8% (Buy Now) [sponsor]

At times like this, the best move you can make is to look at companies with the three “pullback-proof” strengths I just listed above.

OHI is a good example, but I’ve honed in on 5 other stocks trading at even more attractive levels, with even bigger dividends. As I write, these 5 steady income plays yield an incredible 8.5%, on average. And the highest payer of the bunch throws off a massive 9.8% payout!

Think about that for a moment: with nearly 10% of your initial buy boomeranging straight back to you every year in dividend cash, you’re getting a built-in “shock absorber” to protect you in a downturn.

If you hold on for 10 years, you’ll have recouped all of your investment in dividend income alone. At that point, you can ignore the stock price, because everything you bring in—in price gains or dividends—is gravy!

That’s the very definition of safety, and I can’t wait to share these 5 cash-rich dividend-payers with you, along with my complete strategy for surviving—and thriving—in a market storm.

Don’t deny yourself the peace of mind (and high income) you need in these uncertain times. Click here and I’ll give you my full safe-investing plan and everything I have on these 5 “pullback-proof” dividends: names, tickers, buy-under prices, dividend histories and a full rundown of their downturn-resistant businesses.

Source: Contrarian Outlook