Let’s be honest: our lives would be much easier if we could just buy the typical S&P 500 stock, get the 7%+ dividends we need for retirement, and call it a day.Trouble is, the popular kids only pay high yields when the market’s in flames!

Like Pfizer (PFE), which yields a ho-hum 3.8% now.

But if you’d bought when stocks bottomed during the financial crisis, you’d be sitting on a cash machine: back then (March 2009), Pfizer’s payout shot up to an incredible 11%!

Pfizer’s (Very) Temporary 11% Yield

Of course, you needed quick reflexes and nerves of steel to lock in that yield before it vanished in the rebound. Luckily, I’ve found a way (three ways, actually) to grab big 7% payouts much more peacefully. More on those in a moment.

Don’t Let Desperation Ruin Your Retirement

These days, we’re faced with the opposite situation of March ’09: yields are in the basement and stocks are soaring, driving desperate retirees (and near-retirees) to roll the dice on wobbly high-yielders like CenturyLink (CTL).

It’s easy to see why: the telco boasts a fat 6.8% yield right now.

But that outsized yield doesn’t tell you that the company slashed its payout in half last year. Over the past three years, the stock has plunged 42%—while the S&P 500 went 47% in the other direction!

A High Price to Pay for a 6.8% Yield

Dividend disasters like this are why I launched my Contrarian Income Report service in mid-2015. We go one step beyond the mainstream stocks everyone is obsessed with to dig up safe 7%+ dividend payers with price upside, too!

True to its mission, Contrarian Income Report has notched 12% annualized total returns since launch, with most of that gain in dividend cash: as I write, the 17 stocks and funds in our portfolio yield 7.1%.

REITs: Retirement Income Done Right

High-yielding real estate investment trusts (REITs) have been a big part of that performance.

Heck, you’ll double the S&P 500’s yield just by swapping your sub-2%-yielders for the Vanguard Real Estate ETF (VNQ), payer of a 3.3% dividend now.

But buying the “dumb” ETF still only gets you less than halfway to the 7% minimum you’d need to finance your retirement.

Not good enough. (By the way, I say 7% is a minimum because it’ll get you $35,000 in dividend income on a $500K nest egg, which could be enough to let you retire on dividends alone.)

The other problem with REITs these days is, even though I’m still finding bargains for my Contrarian Income Report members, the truth is, deals are thin on the ground, as REITs have paced the market higher in the last year:

REITs Roar, Deals Disappear

But don’t worry, there is still one place you can grab big 7%+ REIT dividends at a discount. It’s an obscure corner of the market few people ever bother to check. I’m talking about closed-end funds (CEFs), including the five specific names (and three “best bets”) we’ll get to in a moment.

First, let me explain why CEFs offer you a great shot at 7% dividends (with upside) in this bubbly market.

“Like Buying 7 Months Ago, but With a 7% Dividend”

CEFs are similar to ETFs—you can buy and sell them on the market, just like regular stocks; they give us three other critical advantages, too:

- Big dividends: There are around 500 CEFs in existence, and their average yield is 7%, the minimum we need for a secure our “dividends-only” retirement.

- Big discounts: CEFs often trade for less than the value of their portfolios. Called the discount to net asset value (NAV), this situation only exists with CEFs. So if you bought a CEF trading at a 7% discount, like the Nuveen Real Estate Income Fund (JRS) below, it would be like buying the typical REIT seven months ago, but with a gaudy 7% dividend!

- Expert management—for free: Unlike ETFs, CEFs are actively managed. And we’re often “comped” for these pros’ fees, because if a CEF trades at, say, a 7% discount and the fees are 2.1%, they’re covered by the discount—and basically thrown into the deal!

By the way, you can forget what you’ve heard about humans not being able to beat the index: when you dive into areas like REITs, preferred stocks and high-yield bonds, managers who lose to their index are the exception, not the rule.

I’ll show you that outperformance in action in a moment. First, let me roll out the five REIT-owning CEFs I want to share with you today—then we’ll cut this down to a “shortlist” of the three best funds on this list.

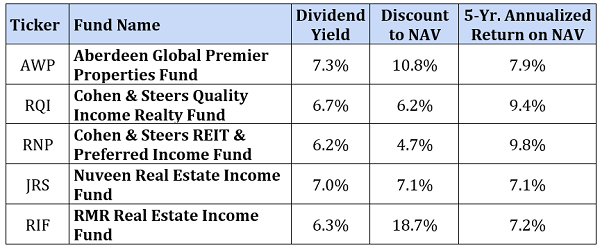

5 Ways to Buy REITs at a Discount

Right away, we can see that each of these funds trades at a nice discount to NAV. And you’re getting serious performance for your money here, too, with each posting at least a 7% five-year annualized return.

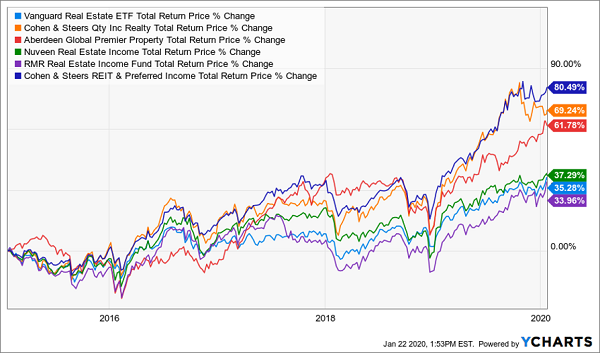

And remember when I said it was a snap for human managers to outrun their benchmarks in markets like REITs? Check this out:

REIT CEFs Cruise Past Their Benchmark

I know there’s a lot going on in this chart, but the upshot is that four out of five of the funds above did just that, with the Cohen & Steers REIT & Preferred Income Fund (RNP) only trailing VNQ by a nose.

These 2 Laggards Don’t Make the Cut

That leads me straight into the real meat of this article: we’re going to cut this group of five CEFs down to the top three. And we’ll start by cutting our lone underperformer, RNP.

That’s not the only reason why it’s getting the axe: RNP also sports the smallest discount of our quintet (potentially capping our upside) and a 6.2% dividend, well short of our 7% target.

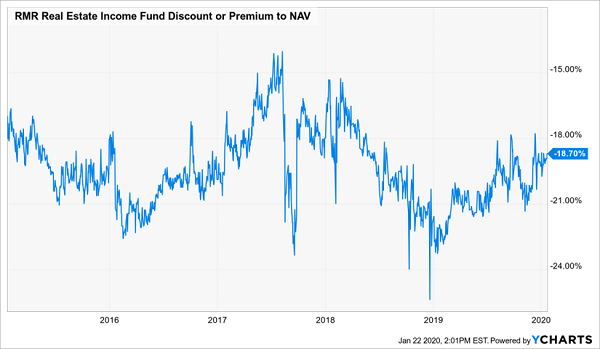

Next, let’s dispatch RIF, whose big discount might also tempt you. But a big discount is useless unless management has a plan to close it, and RIF’s crew hasn’t done that:

RIF’s Never-Ending Sale

Now, management wants to transform RIF into a commercial-mortgage lender, and plans to ask shareholders to vote on the change. If it doesn’t get the go-ahead, RMR Funds says it will likely have to cut RIF’s dividend, which is already the second-lowest yielder on our list (only RNP’s is lower).

Verdict? I see no reason to buy into RIF’s endless sale, especially with the fund aiming to move away from the CEF structure (and/or potentially cutting its dividend).

The Final 3

So where does that leave us?

With a three-fund “mini-portfolio” of AWP, RQI and JRS. Their average dividends are right on our 7% target, plus they boast a nice 8% average dividend and 8.1% average return on NAV between them, too.

That 8%-off deal let us grab top-quality REITs like warehouse operator Prologis (PLD) and senior-care-center operator Welltower (WELL), both top holdings of AWP, at a nice markdown.

Finally, we’re getting a dose of steady preferred shares to add ballast to our REITs, thanks to RQI’s preferred holdings (14% of the portfolio) and JRS’s preferred stocks (40% of the portfolio).

— Brett Owens

NEW: 4X Your Dividends With My “Perfect Income Portfolio” [sponsor]

A 7% dividend is great, but what if I told you I’d found a proven way to boost that yield to 8%?

In other words, if you hold the typical investor’s stock portfolio, you’d be yielding right around 2% today. But you could increase your income 4-TIMES just by swapping your middling S&P 500 names for the diversified picks in my new “Perfect Income Portfolio.”

It’s hard to understate what a difference that could make: on a $500K nest egg, a $10,000 income stream becomes $40,000. Got $750K? Great! Your sorry $15,000 income becomes $60,000!

And on it goes.

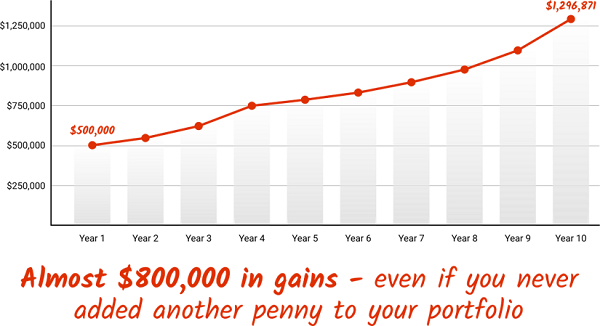

We haven’t even talked about the upside. If you followed the simple strategy behind this breakthrough portfolio, here’s what would have happened to your cash in the last decade:

Don’t wait another minute. Go right here to get full details on my “Perfect Income Portfolio,” including my complete 4X-income strategy and the names and tickers of each cash-spinning pick inside.

Source: Contrarian Outlook