The New Year is here, which means it’s once again time to revisit a contrarian (and income) investing tradition: The “Dogs of the Dow.”

This simple yet famous dividend strategy involves buying the 10 highest yielders in the 30-component Dow Jones Industrial Average at the beginning of each year.

It’s an income play, sure, but this strategy also has to do with value.

The idea: Truly strong blue-chip stocks rarely become “obsolete,” so high yields—often driven by lower prices in the prior year—are just a signal that the stocks are oversold and due to bounce back.

It’s a win-win, in theory. Not only do you get higher-than-usual income on these blue chips, but you also get them at a good price. The combined income and value upside should make these total-return juggernauts.

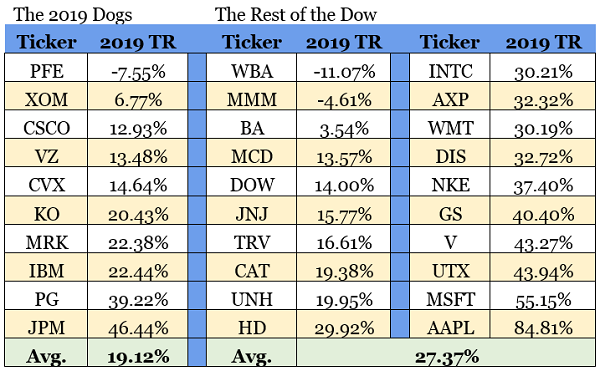

But theory didn’t play out practice last year, as dog-lovers left money on the table:

Data source: Ycharts.com

Data source: Ycharts.com

To be fair, it was a rare bit of underperformance for the Dogs. The Dogs have beaten the Dow on a total-return basis since 2001, and last year snapped a four-year winning streak for the ubiquitous dividend strategy.

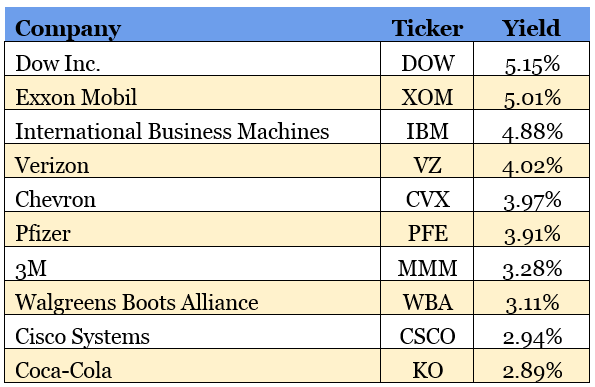

But as I look at the 2020 Dogs, it’s clear we need to be more discerning:

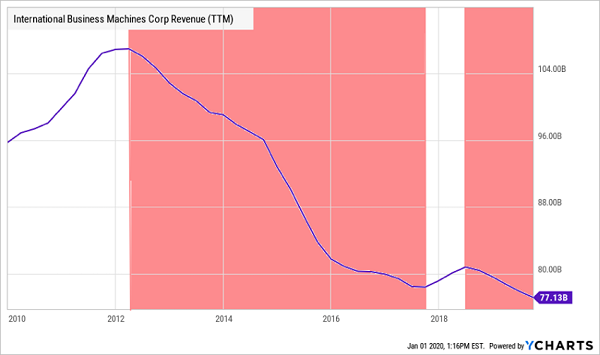

International Business Machines (IBM), for instance, hasn’t been able to escape the “doghouse” for years, and for good reason: It’s a dividend dumpster fire.

A couple of months ago, the tech company announced its fifth consecutive quarter of revenue declines. Maybe it’s trying to “reclaim the magic” from its 22-quarter sales fail that ended back in 2018.

This Is Not a Recipe for Success.

(Note: The red bars above indicate lower sales year-over-year. We are dividend investors, but we still require sales growth to fund our payouts over the long-term!)

Here are three better bets for Dow Dogs in 2020:

3M (MMM)

Dividend Yield: 3.3%

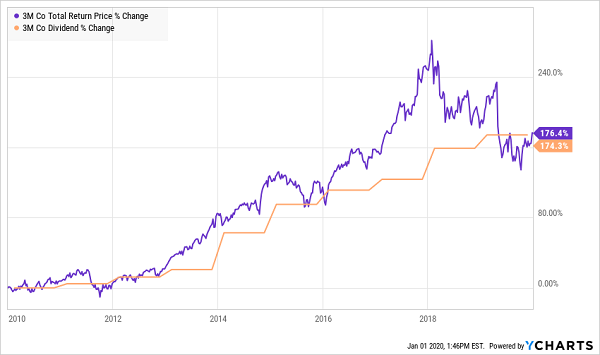

The pain continued for industrial conglomerate 3M (MMM) in 2019.

Shares of 3M—the maker of Post-it Notes, Ace brand bandages, Scotch tape, Thinsulate insulation and numerous other commercial and consumer brands—have lost almost a third of their value since early 2018, including a single-digit loss in 2019.

A huge chunk of the issue has been a mix of global cyclicality—weakening growth in China and other emerging markets has weighed heavily on demand for the multinational giant—and further Chinese pain thanks to the country’s trade war with the U.S. Thus, analyst predictions for a small recovery in global growth, paired with the expected Jan. 15 signing of a “Phase One” trade deal, should bode well for 3M.

Alas, this longtime Dividend Aristocrat has more problems on its plate.

As I highlighted back in October, JPMorgan’s Stephen Tusa didn’t mince words when he called the company’s business model “broken.” He called into question billions of dollars spent on restructuring, deeming 3M’s problem a “structural issue, that there is generally a higher cost to serve than many appreciate, now seems clear.” And on top of that, the company faces mounting legal issues (and costs) over its “PFAS” chemicals. While it has set aside hundreds of millions to cover potential legal costs, some experts are estimating a price tag upward of $10 billion.

3M might have a few bricks taken off its shoulders in 2019, but that’s not enough reason to enthusiastically buy this troubled Dog of the Dow.

3M Is Undergoing a Painful “Normalizing”

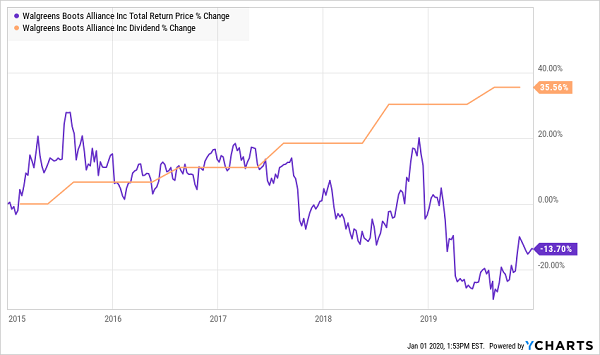

Walgreens Boots Alliance (WBA)

Dividend Yield: 3.1%

Walgreens Boots Alliance (WBA) was the worst performer in the Dow last year, at -11% including dividends, and in fact has been dead money since 2015.

It’s Like You’re Being Taxed Just to Hold Walgreens (WBA)

Much of the pain came on a 12% single-day drop in April after the company reported what CEO Stefano Pessina called “the most difficult quarter we have had since the formation of Walgreens Boots Alliance.” Second-quarter earnings fell short of expectations, and the company was forced to cut its full-year outlook amid weak performance on numerous fronts.

Walgreens’ situation is so tenuous that the company has been trying to entice KKR & Co. (KKR) into executing a leveraged buyout to take the drugstore private. But analysts called shenanigans on the logistics of the deal, and in December, The Wall Street Journal reported that it had run into financing issues.

Dividend Aristocrats are notoriously low yielders, so WBA’s 3%-plus payout looks attractive on that front. And Walgreens is trading at a dirt-cheap 9.6 times forward earnings estimates. But given that profits are expected to decline this year, and the company is otherwise rudderless, investors’ best hope of significant gains in 2020 would seem to be a buyout – one that looks less likely than it did a couple months ago.

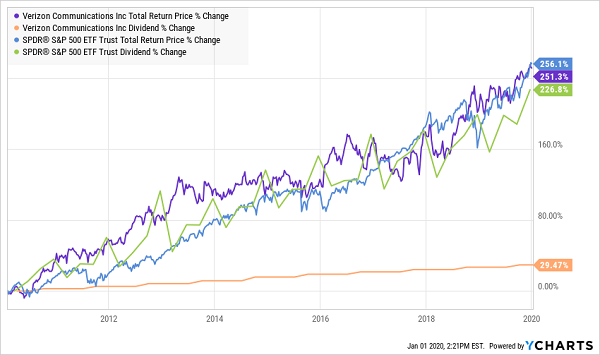

Verizon (VZ)

Dividend Yield: 4.0%

Verizon (VZ) is participating in one of the more exciting investing mega-trends of the new decade: the roll-out of 5G technology.

5G is the next generation of communications tech—what many expect to usher in an explosion of the Internet of Things, and general connectivity with the world around us. And Verizon is widely considered to be leading U.S. telecoms’ push to get that infrastructure up and running.

It sounds good. And for infrastructure REITs such as American Tower (AMT) and Crown Castle (CCI), and communications chipmakers such as Qualcomm (QCOM) and Broadcom (AVGO), it is good, and should lead to tangible growth. But at least in 2020, the pros’ expectations for Verizon look no different than recent years: low-single-digit gains on the top and bottom lines.

That’s also problematic given issues with its core business. MoffettNathanson analyst Craig Moffett points out troubling signs including shrinking margins, slightly higher customer churn and even questions about whether Verizon indeed has the best network.

Verizon is a de facto utility, and it at least pays out cash like one. Its 4% yield is one of the most respectable among the 30 Dow stocks.

This Isn’t Normal.

But note the chart above. I frequently discuss how stock prices “catch up” to dividend growth over time, but we have a situation in Verizon where we might be due for the same process in reverse—where VZ the stock “slows down” to its glacial dividend growth.

Even worse is the fact that Verizon’s payout is growing as slowly as many Dividend Aristocrats, but the telecom only has a 13-year streak under its belt. That bodes poorly for future hikes, which I expect to be nominal.

— Brett Owens

“Perfect” Retirement Income”: Start 2020 By Quadrupling Your Yield [sponsor]

The Dogs of the Dow feed into one of the most common mistakes that “first-level” retirement investors: buying the overcrowded, overpriced blue chips that financial talking heads prop up as safe bets year-in and year-out.

But they’re not safe. There’s nothing “safe” about not making enough income to take care of your most basic needs.

“Safe” is being able to afford your home, your utilities and a high quality of life even if the stock market doesn’t cooperate. And you can lock up that level of safety from the dividend-rich stocks in my “Perfect Income Portfolio.”

Nest eggs are being stretched paper-thin because medical innovations are helping us live longer than ever before, meaning retirement accounts have to last far longer than they were ever intended to. But this is 2020, not 2000. 10-year Treasuries don’t pay 6.6% anymore – they pay 2.6%. The 2%-3% yields on most Dow stocks just won’t cut it, either.

Instead, investors – especially those with more modest nest eggs – need roughly 3x to 4x the yield of the broader market. And those substantial income checks need to survive not just through 2021 or 2022, but literally decades down the road.

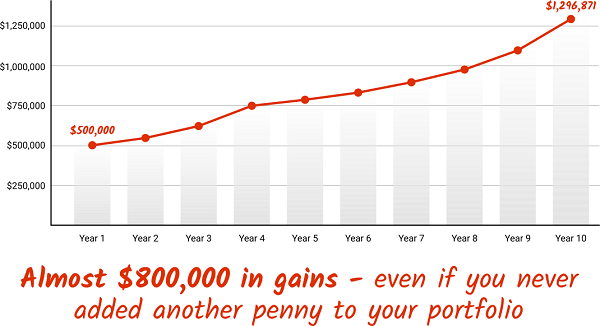

My Perfect Income Portfolio offers exactly that. In fact, several of my readers have emailed me to tell me this portfolio has literally doubled, tripled, or in a few cases actually quadrupled their annual income.

Also, this is a buy-and-hold portfolio. This isn’t a crazy options tactic or a set of short-term swing trades. It’s just a set of under-the-radar, contrarian income plays that can quickly build your wealth without piling on the extra risk of gambling on newspapers and dying retailers.

Too good to be true? Look at this strategy’s past 10 years of returns, and you’ll see why I call it the “Perfect Income Portfolio”:

What really makes this group of stocks stand out is that it’s so much more than high headline yield. This portfolio checks off a bundle of vital retirement boxes:

- It gives you a safe, secure, and steady income of $10s of thousand per year in cash—not just ‘paper gains.’

- It pays out more than enough to live on from dividends without drawing down your savings or assets.

- You avoid overly complex, high-risk investments that can wipe out decades of hard-earned money in a matter of weeks or months!

- You’re not involved in any risky options, spread-bets, or day-trading.

- It’s simple to set up and simple to manage. That way you’re not glued to your screen all day. Go out. Enjoy life. Your check’ll be in the mail.

Don’t lie awake anymore worrying about your yo-yo-ing net worth. Instead, let me teach you more about this incredible strategy, including its dominant track record. In fact, I’ll even let you hear it from the mouths of other investors that have reaped market-smashing gains from my research service.

Don’t wait another minute. Learn how to get 2x-4x your current income with this simple, straightforward system. Click here to get a FREE copy of my Perfect Income Portfolio report, including tickers, buy-in prices, dividend yields, full analyses of each pick … and a few other bonuses!

Source: Contrarian Outlook